Swiss National Bank preview: Little reason to move

- 17 June

- FX Switzerland

The Swiss National Bank meets tomorrow and is expected to keep its policy rate unchanged at 0% amid subdued inflation

Inflation remains under control

Rising energy prices have pushed inflation higher across much of the world, but Switzerland has been largely shielded from this trend. Headline inflation stood at 0.6% year-on-year in May, unchanged from April.

Energy prices have, of course, increased in Switzerland (+17.7% year-on-year for petroleum products) as they have elsewhere. Still, the strength of the Swiss franc continues to exert a significant disinflationary effect. Imported goods, which account for 22% of the consumer price index, rose by only 0.7% year-on-year in May. This marks a clear shift after three years of declining import prices, but it remains well within the SNB’s comfort zone.

Domestic inflationary pressures are also contained, with prices rising by 0.6% year-on-year in May.

All in all, inflation in Switzerland has picked up from the 0.1% observed at the start of the year, but remains comfortably within the SNB’s 0-2% target range. Early-year deflation fears have receded for now, while the risk of a sharp inflation increase in the coming months appears negligible. There is therefore little reason for the SNB to adjust interest rates at its June meeting.

Inflation outlook and FX interventions in focus

That said, two aspects will be closely watched tomorrow.

First, the SNB’s medium-term inflation projections. In March, these stood at 0.5% on average for both 2026 and 2027, and 0.6% for 2028. A modest upward revision would carry limited implications for monetary policy. With inflation still firmly within the 0-2% target range, a rate hike remains unlikely in the foreseeable future.

Conversely, a downward revision could signal renewed concern about deflationary pressures once the impact of recent energy price increases fades. Even so, such adjustments would not justify a policy move this month. We expect rates to remain at 0% over the next two years.

Second, close attention will be paid to any comments on foreign exchange interventions. The Swiss franc has appreciated in effective terms over the past 12 months, although upward pressures have eased since early March, when the SNB explicitly indicated a greater willingness to intervene.

Importantly, in real effective terms, the franc has not become more expensive, thanks to lower inflation in Switzerland compared with its peers. This is the metric the SNB monitors most closely. With Swiss inflation set to remain persistently lower than elsewhere, concerns about excessive currency strength should remain contained.

Overall, the Swiss backdrop appears more favourable for the SNB in June than it did in March, and certainly more comfortable than for most other central banks. This should allow policymakers to remain firmly on hold. Any meaningful shift in tone would come as a surprise.

Charlotte de Montpellier

EUR/CHF: SNB would prefer higher levels

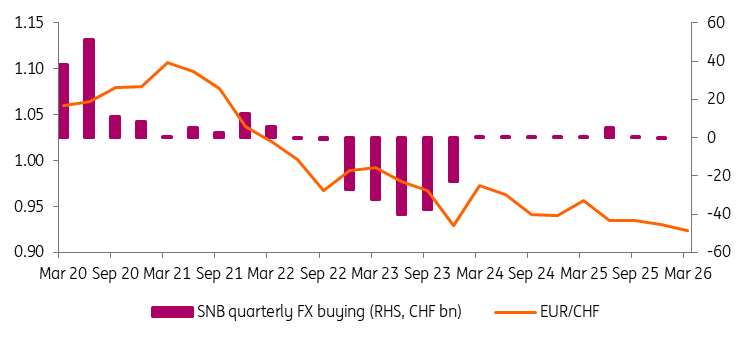

The exchange rate is an important monetary policy tool for a small, open economy such as Switzerland. And let’s not forget that during Switzerland’s last major inflation shock in 2022 and 2023, the SNB actively used a stronger Swiss franc to tighten policy. In fact, in the five quarters from the fourth quarter of 2022 to the end of 2023, the SNB sold CHF160bn of FX to drive franc strength and fight inflation.

While other central banks have hiked or are considering hiking this year, Switzerland’s starting point of low inflation means that the SNB is in no hurry to tighten or to start selling EUR/CHF again. Indeed, its current position is to show a greater willingness to intervene to curb further franc gains. 30 June will see the central bank release figures of FX intervention for the first quarter, where FX buying could exceed the CHF5bn undertaken in the second quarter of 2025.

Yet the SNB has also been sounding relaxed around the exchange rate, citing lower Swiss inflation relative to trading partners keeping the real Swiss franc level contained. While the nominal trade-weighted franc has risen 30% since 2020, the inflation-adjusted franc has only risen 6%.

Adding in the franc’s status as a safe haven on geopolitics and a play on the dollar de-basement trade builds quite a mixed picture of the currency. Our baseline sees EUR/CHF continuing to trade around these 0.92 levels for a while with some upside risks over the summer if the European Central Bank does indeed hike in July or September. In terms of its short-term reaction to the SNB meeting, we doubt the SNB needs to sound hawkish and could see EUR/CHF edge a little higher if it pushes the message of a prolonged pause.

Chris Turner

SNB's FX intervention activity since 2020

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more