SNB: It’s all about the adverb

- 13 September 2017

- FX Switzerland

Will the Swiss National Bank remove the adverb 'significantly' from its CHF description?

Swiss semantics

Ever since it chaotically removed the 1.20 EUR/CHF floor in January 2015, the Swiss National Bank has included the sentence 'the Swiss Franc is significantly overvalued' in every quarterly monetary policy assessment. This Thursday, markets will focus if that adverb, 'significantly', is withdrawn.

Such a move would suggest the SNB is a lot more relaxed and:

a) would be less inclined to continue intervening in FX markets and

b) could be slightly closer to raising its 3m CHF Libor policy target of -0.75%.

The reason for the focus on 'significantly' is because:

a) EUR/CHF has rallied 6% since the SNB last met and

b) Earlier this month, SNB President Jordan admitted in a speech that the summer moves had reduced the franc's significant over-valuation.

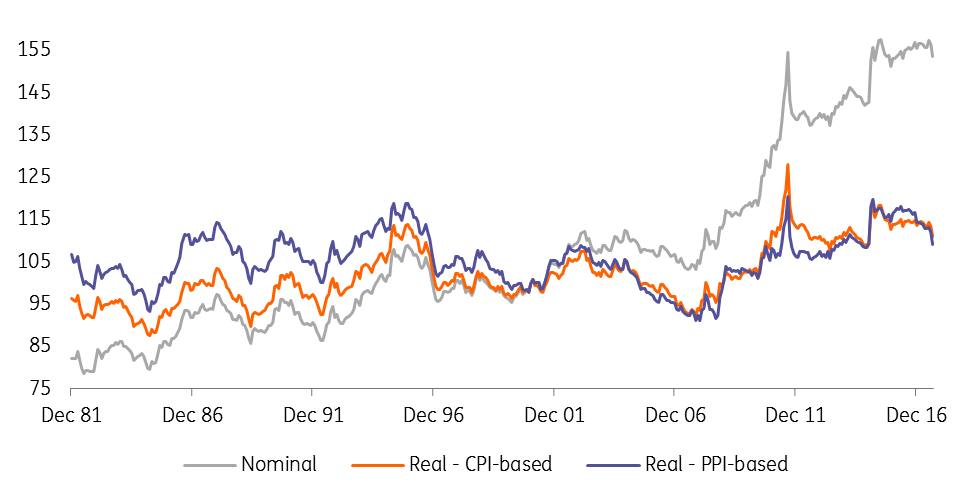

And looking at the SNB's effective exchange rates, we can see that as of the end of August, the SNB's inflation-adjusted exchange rate indices have declined more than the nominal index - largely as Swiss CPI runs consistently below that of major trading partners. Also note that the decline in the nominal CHF index, just 2.5% off its highs seen in summer 15 is much less than the CHF fall against the EUR.

In theory, then, a decent decline in the inflation-adjusted CHF exchange rate index give the grounds for the SNB to remove 'significantly'. But will it?

SNB measures of CHF trade weighted exchange rates

SNB likely to remain cautious

When it comes to the domestic story, the SNB will be less cheerful. The recently released 2Q17 GDP came in lower than expected at 0.3% quarter on quarter and the 1Q17 figure was revised down to 0.1% QoQ from 0.3%. The slow start to the year could see the SNB revise down its full year 2017 growth forecast to 1.5%.

On inflation, the SNB may have grounds for some small upward revision to its forecasts, given that energy prices have risen a little and the CHF has fallen. Yet any revisions will be applied from an exceptionally low starting point. In June, the SNB saw headline CPI edging lower to +0.1% YoY in 1Q18 and not nearing the SNB's forecast (of close to, but under 2%) at any point on the SNB's horizon - to 1Q20.

In short, we doubt any adjustment to the inflation forecast will have a meaningful impact on the pricing of the first SNB hike - currently expected by the market in summer 2019.

The SNB's waiting game

Instead, we expect the SNB to continue to deliver a dovish message on Thursday - emphasising the need to keep rates negative and the threat of FX intervention - sticking to the plan that the ECB needs to move first. After all the ECB broke the SNB's floor in January 2015 when it introduced QE, so it can fix an over-valued CHF by tapering.

We think the SNB will remove the ‘significantly’ from its statement but it’ll be a way to emphasise policy will not be changing for a while

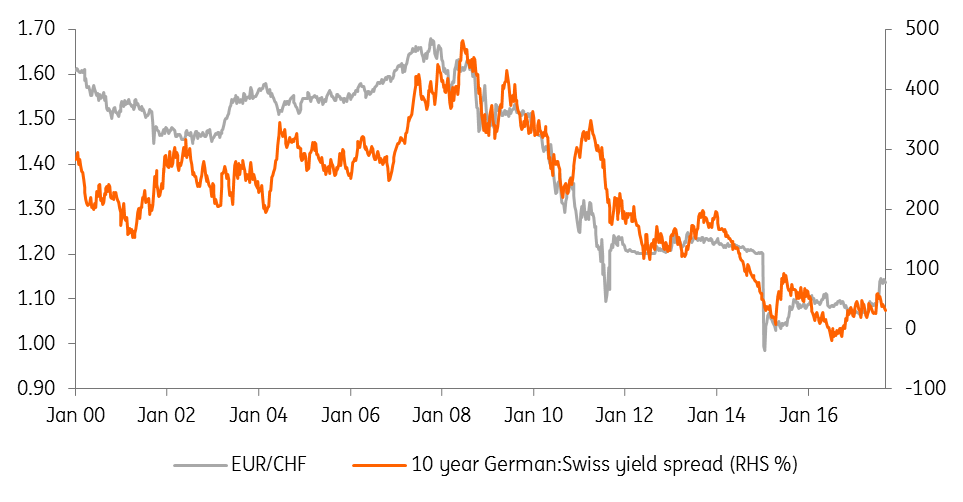

As such we expect the SNB to be at least twelve months behind the ECB in normalising policy - suggesting that if the ECB were to raise the deposit rate in late 2018, the SNB would not raise its 3m CHF Libor target of -0.75% until late 2019. All this would help widen spreads against the CHF - the 2018 story will be one of rate divergence at the long end of the curve - and drive EUR/CHF higher.

And regarding the bigger picture, we reiterate the points made in August, that chances of EUR/CHF hitting 1.30 in 2018 are underpriced.

Spreads should help lift EUR/CHF into 2018

Final word

Coming back to that issue of whether the SNB removes 'significantly' from its statement - we think it will. But we also think it will find a way to emphasise policy will remain unchanged for a substantial period. This should mean that any dip in EUR/CHF - say to the 1.1350/1400 area - is temporary.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more