Six things we think about Hungary

- 30 June 2022

- Hungary

As we have reached the end of the first six months of 2022, we have decided to make a short overview in six points about the Hungarian economy’s performance and its near-term future. This first half was a mixed bag, but it could have been worse. However, with mounting risks, we see a gloomier future ahead

Economic activity holds up well

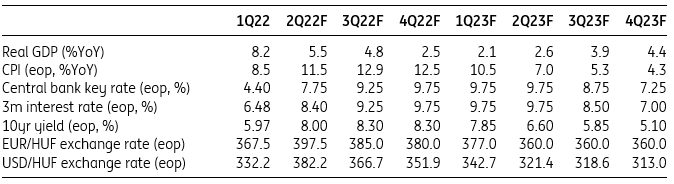

Despite all the negative external developments (war, sanctions, supply chain disruptions, etc), GDP growth has held up quite well. The first quarter brought a 2.1% quarter-on-quarter performance, though it was mainly spurred by the extraordinary government transfers to households. Incoming data shows a marked slowdown in the second quarter and in our base case we see a minor contraction on a quarterly basis. We look for a mild rebound during the second half of the year; thus, we see GDP growth at 5.3% in 2022. We downgrade our 2023 outlook to 3.2% as we expect a more marked slowdown in consumption and investment activity due to stronger inflation, higher interest rates and more moderated growth of real disposable income.

Peak in inflation is still ahead of us

The past six months were all about upside surprises in prices. Inflation moved from 7.4% year-on-year in December 2021 to above 11% YoY by June (according to our expectations). The monthly repricing has been three-four times stronger than we used to see as corporates are using their pricing power to pass on rising costs to consumers. There is a strong correlation between producer prices and consumer prices, suggesting further price pressure is in the pipeline. We see the year-on-year headline inflation peaking in September or October at a tad below 13%, before it starts a slow and gradual decline. We upgrade our 2022 average inflation forecast to 11%, while moving up our 2023 outlook to 7.4% with both surrounded by further upside risks.

Labour shortage is a growing pain

Under normal circumstances, here we would cheer about the strength of the Hungarian labour market. The unemployment rate dropped to 3.5% in May, yearly wage growth is around 15% and job vacancies are close to record-high levels. The only caveat here is that labour shortages are adding to the price pressures. We expect the tight labour market to remain with us for the remainder of the year, pushing companies to raise wages further. This year, this will support growth of consumption, but next year we see a marked slowdown in the economy’s real wage bill, as growth in employment will hit the wall and companies pricing power will be reduced, so they will be less open to meet with workers' rising salary demands.

Fiscal policy faces a turnaround

The first quarter of the year was all about spending. The government injected roughly HUF2,000bn into the economy. It is difficult not to draw parallels between the April general elections and the loosening of the budget. By the end of May, the budget accumulated a shortfall of 87% of the full-year target. Thus, it hardly comes as a surprise that the government announced an austerity package. The full package contains roughly HUF1,200bn spending cuts and approximately HUF900bn in revenue enhancing measures. This will significantly improve the budgetary situation in the second half of the year, and we see the government being able to meet this year’s 4.9% of GDP deficit target.

Monetary policy keeps on fighting

Since the start of 2022, the National Bank of Hungary has raised the base rate by a total of 535bp and it now sits at 7.75% at the end of June. Despite carrying out the largest tightening cycle in the region, Hungarian assets have remained under pressure due to several political and geopolitical risks. The only realistic point of the monetary policy impact remains the currency, in our view. To keep EUR/HUF stable, the central bank needs to continue its decisive tightening at least until inflation peaks. Our base case is a 50bp increase per month with a terminal rate of 9.25-9.75% in September-October, where we see the highest probability for inflation to peak. We forecast a positive real interest rate environment from spring 2023.

Forint remains in the grip of external factors

The forint was a clear underperformer in the region in the first half of 2022 and EUR/HUF reached a new high at 403. The NBH stepped up and in the short term we expect the latest rate decision to add some support to the forint. However, we believe that under current conditions there is room for appreciation only towards the 390-395 range versus the EUR. In the long run, not much has changed in our view. The forint continues to be our least favourite currency in the CEE region, but we continue to watch headlines signalling a turnaround in the Rule of Law and EU funds disputes that should unlock the hidden potential of the forint in the second half of the year (perhaps in September).

Quarterly forecasts of ING - Hungary

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more