Singapore manufacturing stages a surprisingly strong surge in May

- 25 June 2021

- Singapore

We believe the authorities will continue to see through the latest outsized economic activity and focus on supporting the recovery via the persistent accommodative macro policy stance amid lingering Covid-19 threat

| 30% |

May industrial production growthYear-on-year |

| Higher than expected | |

It’s just a statistical boost

Singapore released the industrial production figures for May showing a surprisingly strong 30% year-on-year and 7.2% month-on-month (seasonally adjusted) surge. This was ahead of our 19% YoY and -6.0% MoM forecasts for the month and April’s 2.1% YoY and 1.0% MoM growth.

Among the key manufacturing clusters, electronics output posted over 23% YoY growth but was down -9% MoM, led down by semiconductor production. Pharmaceutical output jumped by +38% YoY and but was down slightly by -0.9% on the month. Petrochemicals, engineering, and general manufacturing fared well with modest month-on-month gains leading to strong year-on-year growth.

Export recovery is paused

However, the best manufacturing performance in months was at odds with almost paused export recovery in the last month, while the roaring Covid-19 second wave restrained the overall economic activity since mid-May.

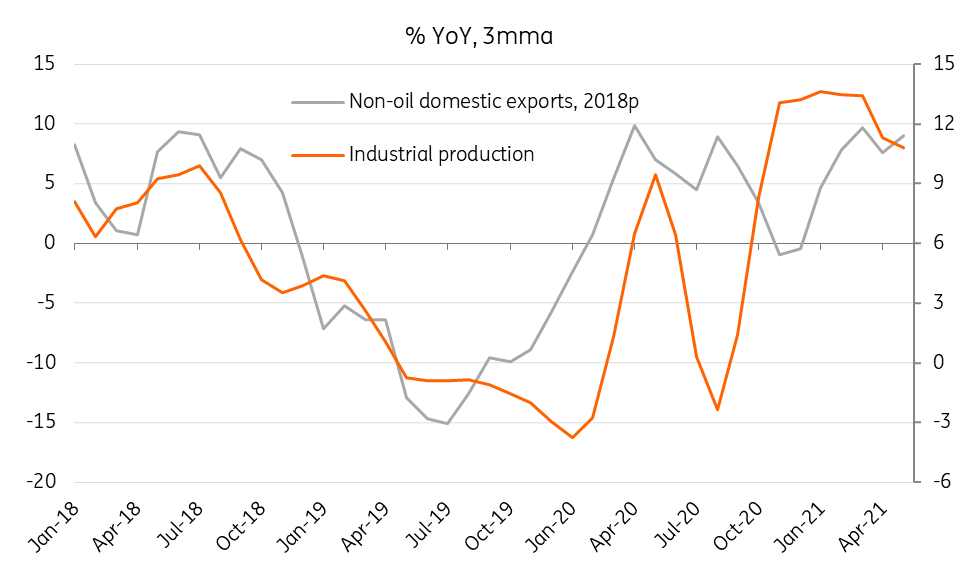

Non-oil domestic exports, the key indicator of the economy’s health, were almost flat on month in May, even as the low base effect pushed the year-on-year growth modestly higher to 8.8% from 6.0% in April. As for NODX, the base effect explains most of the surge in the yearly IP growth. And, a wonky seasonal adjustment factor flattered the month-on-month IP growth; unadjusted -3.9% MoM fall was the second consecutive negative reading.

Exports drive manufacturing

Strong 2Q GDP view stands

The IP growth closely tracks manufacturing GDP growth, which in turn drives the overall GDP growth. With the base effect continuing to support IP growth in June, we expect a pick-up in the quarterly manufacturing GDP growth to over 13% YoY in 2Q from 10.7% in 1Q. We should also see other GDP components of construction and services turning the corner to positive year-on-year growth in this quarter. With this our 12.2% YoY growth forecast for 2Q GDP remains on track.

However, strong 2Q GDP will still be one-off as waning base effects and the lingering impact of the latest Covid-19 outbreak on domestic spending will work together to dampen GDP growth over the rest of the year. Our full-year 2021 GDP growth forecast remains at 4.9%, which is within the official 4% to 6% forecast range but more bearish than the market consensus of over 6% growth.

We believe the authorities will continue to see through the latest outsized economic activity growth and focus on supporting the recovery via persistent accommodative macro policy stance amid lingering Covid-19 threat ahead.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more