Singapore 2020 Budget – Dealing with the viral crisis

- 16 February 2020

- Singapore

Singapore's government is preparing for a more detrimental fallout from the coronavirus than it did for SARS in 2003 and is expected to roll out a significant stimulus in the FY20 budget to be unveiled on Tuesday, 18 February. We also think the central bank won’t risk lagging behind the curve on monetary easing

Bracing for the worse

As if the global trade war and technology slump weren’t enough adverse shocks to the economy over the last couple of years, now we have a pandemic depressing growth prospects further this year. The Covid-19 (the coronavirus) has been evolving as an unprecedented disease in recent history, worse than the SARS in 2003. And, given a small, open economy Singapore remains among the most vulnerable to such external headwinds. Indeed, the economic fallout from the latest virus could be more detrimental than SARS and this calls for significant policy support to the economy.

Therefore, all eyes are on the Budget for the financial year 2020 (starting in April) that Singapore’s Deputy Prime Minister and Finance Minister Heng Swee Keat is due to announce tomorrow, Tuesday, 18 February. We expect it to include a big-bang fiscal stimulus to avert the crisis.

Unprecedented crisis…

As during SARS, Singapore has been one of the front-line countries affected by the coronavirus with the second-highest infection outside of China. However, the spread of the current disease is far more rapid than SARS. And the current economic backdrop is already far weaker than it was during SARS. Hence, the SARS provides no reliable starting point to gauge the potential economic impact of Covid-19.

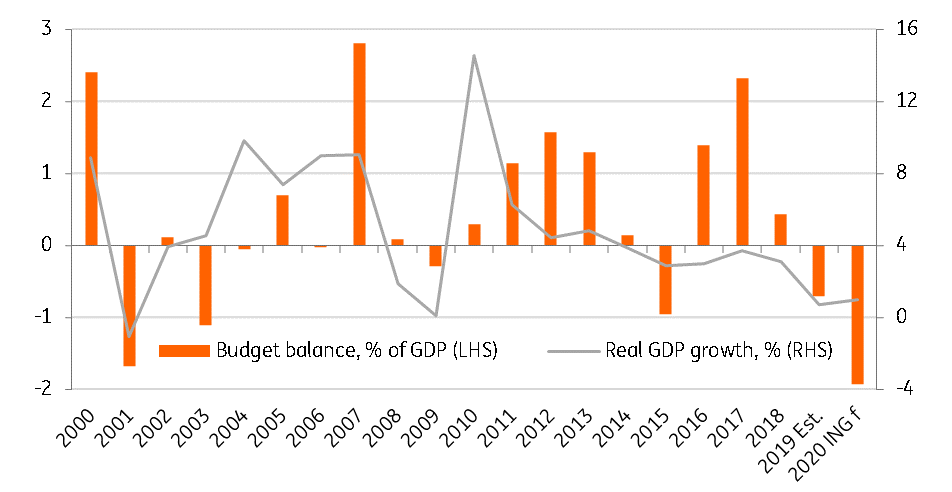

The SARS impact was limited to only one quarter of a stalled economy with a 0.3% year-on-year GDP contraction in the third quarter of 2003. However, the backdrop of global growth at that time, especially of China, which was opening up following its WTO entry, was very strong and it helped give a quick bounce-back to Singapore’s economy. In contrast, the trade war and tech slump have already depressed the economy in recent years. Singapore eked out 0.7% growth in 2019, a sharp slowdown from 3.1% in the year before, making it the worst growth year since the global financial crisis in 2009 (with a 0.8% fall).

The impact mainly flows through tourism and trade as China is a big partner of Singapore in both these areas. Chinese tourists account for little under one-fifth of annual visitor arrivals to Singapore. And, China is a destination for about one-quarter of the island’s non-oil domestic exports (including exports to Hong Kong, SAR). The authorities are expecting a 25-30% plunge in visitors this year, which together with a sharp slowdown in exports to China will undoubtedly mean a big economic slump ahead. Moreover, the global spread of the disease implies visitors from and trade with the rest of the world takes a hit too and this results in far greater economic damage.

… requires an unprecedented response

Even before the outbreak of Covid-19, the government was preparing a growth-friendly budget to jumpstart the economy, which was already reeling under the global trade war and tech downturn. The talks of more support measures to the affected sectors have intensified with the rise in the number of infections.

The city-state’s abundance of riches evident from several years of fiscal surplus recently will be put to use to minimise the damage to the economy.

The city-state’s abundance of riches evident from several years of fiscal surplus recently (barring FY19 when the budget was programmed for a deficit of about 0.7% of GDP) will be put to use to minimise the impact of the virus on the economy.

We anticipate close to 2% of GDP fiscal deficit, up from 0.7% planned for FY19 and the most in two decades (after a 1.7% deficit during the burst of the tech bubble in FY01).

Taking a cue from the SARS stimulus package, the Covid-19 package is likely to contain some income tax relief for both individuals and corporates, target relief measures for the tourism and retail sectors, incentives for small and medium-sized enterprises to stay afloat without having to downscale operations, and probably some boost to real estate via a rollback of some earlier tightening, besides the usual long-term initiatives supporting innovations and digital transformation.

The bigger the crisis, the bigger is the fiscal thrust

Damage control - MAS is likely to pitch in too

We think a wave of growth forecast downgrades is becoming the order of the day in both Asia and globally and we won’t rule out further cutting our forecast for Singapore’s 2020 growth, even after our recent revision to 1% from 1.6%. Although 1% is consistent with the official view of growth improving modestly this year over the 2019 rate, it still sounds optimistic considering the gravity of the crisis at hand. However, underlying optimism is the expectation of a greater macro policy thrust.

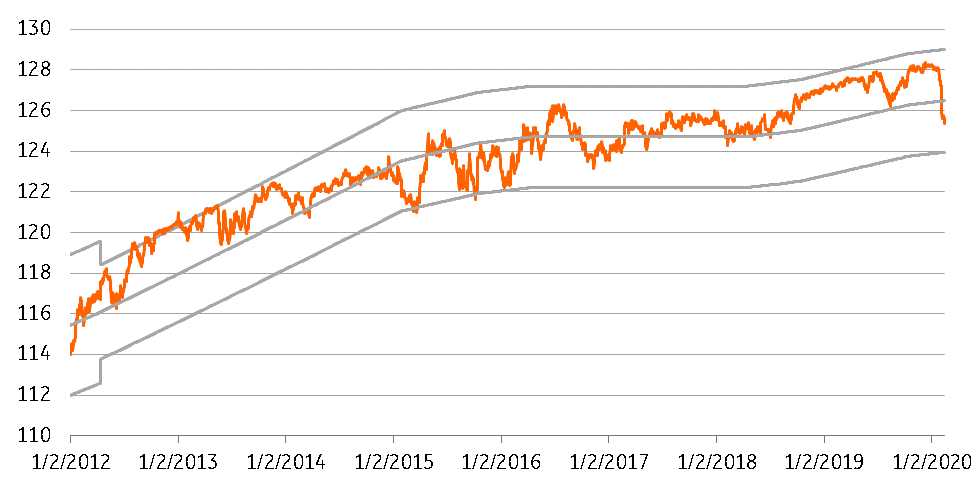

Not just the fiscal policy, but monetary policy will eventually need to share some of the burden. The Monetary Authority of Singapore (MAS – the central bank) has dampened hope of any easing ahead on the grounds that there was room for accommodation within the current policy band for the Singapore Dollar Nominal Effective Exchange Rate (S$-NEER). Even so, and despite a slight reduction in the slope or the rate of appreciation of the S$-NEER band at the last review in October 2019, the policy still dictates a tightening bias which may not come across as appropriate for the ongoing economic risks.

Recognising the growth risks, the central bank easing cycle in Asia has gained momentum lately – banks in China, Malaysia, Philippines, and Thailand (Indonesia’s is likely to join the camp this week) have cut their policy interest rates in recent meetings. We don’t think the MAS would risk lagging behind in its response, while the little available space for accommodation within the current band could well be exhausted in a matter of days, if not weeks or months as can be judged from a sharp swing from 1% strong S$-NEER from the mid-point of the policy band (estimated per the Goldman Sachs Index on Bloomberg) to about 1% weaker currently.

The MAS’s response to the SARS crisis was an easing via a downward shift of the policy band with zero appreciation in July 2003. We consider this as a reliable guide to the response this time around and expect it at the forthcoming review in April. After all, it is damage control from the crisis, not outperforming it.

S$-NEER Policy Band

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 17 February 2020

- This bundle contains 3 Articles