Markets are still complacent amid the Fed shake-up

- 8 November 2017

- United States

Markets may have shrugged off the upcoming change at the top of the Fed, but they remain complacent about the risks of faster rate rises next year

Markets are too complacent on rate hikes

After weeks of twists and turns, markets breathed a sigh of relief as President Trump opted for continuity in his nomination of Jerome Powell for Fed Chair. The fact that Trump opted for a "gradualist" on interest rates, rather than the potentially more hawkish Taylor or Warsh, has contributed to the Treasury curve flattening to its lowest in 10 years.

However, we feel the market is being too complacent. The combination of upside risks to growth and mounting inflationary pressures, as well as a hawkish rotation in the make-up of Fed voters, suggests that markets are too cautious in only pricing in one hike next year. We expect two, with risks of more rather than fewer.

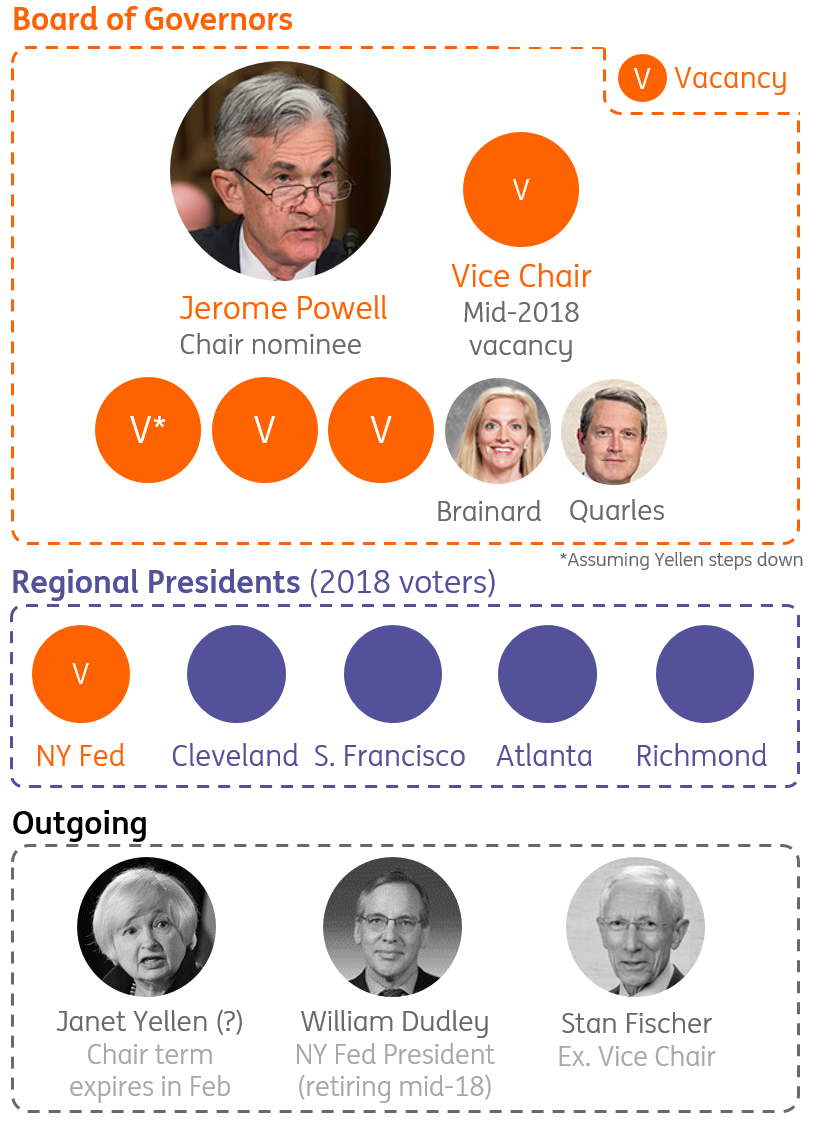

Some scepticism is understandable

Assuming Yellen decides to stand down completely when her Fed Chair term ends in February, four out of the seven positions on the Federal Reserve Board will be vacant. There is also now a vacancy at the New York Fed, given that its President, William Dudley, is retiring early. Remember the NY Fed is particularly involved in the financial market aspects of monetary policy, as well as its President having a permanent vote on interest rates.

As with the Fed Chair, Trump has the choice over who fills the four board member vacancies. Given he is facing mid-term elections in a year's time, it is unlikely he'll want to see clear hawks appointed that could threaten his three percent growth target.

But until Trump has made his decisions and the full 2018 voter mix becomes clear, it is perhaps not surprising that markets continue to treat the Fed's latest "dot diagram" cautiously. Some scepticism is also understandable given the Fed has signalled higher rates before in its dots, without ultimately following through. And on the face of it at least, below-target core inflation and October's weak wage growth number suggests there's no pressing need for a more aggressive shift towards policy tightening in the near term.

| Four |

Current vacancies on the Fed Board of Governors |

Strong growth, rising inflation and financial stability risks point to higher rates

There are also many reasons to think markets are being too cautious on the Fed. Strong business surveys, robust employment and post-hurricane rebuilding means we could see another 3%+ growth figure in the fourth quarter. Commodity prices and import costs are rising, and with that we see inflation recovering over the next few months. The tightness in the labour market suggests there are upside risks to wage growth too.

There are many reasons to think markets are being too cautious on the Fed

We have also seen the Fed broaden out the reasoning for why higher rates might be justified. The "adverse implications for financial stability" of "persistently easy policy" is one such factor, and relatively loose financial conditions (weaker dollar and flatter yield curve) is another. Some Fed officials have also cited "rich" asset valuations, and with rates at such low levels, the Fed doesn't have much ammunition to help stimulate the economy if a bubble were to burst. That implies a need to step in earlier to prevent them forming in the first place.

The Fed is set to take a hawkish turn

Then there's the annual rotation of voters at the Fed. This will see arch-dove Neel Kashkari leave, along with Charles Evans (who isn't far behind on the dovish scale). They'll be replaced by the more hawkish John Williams and Loretta Mester. Williams is in favour of three hikes next year, and Mester has even hinted she'd like the Fed to go 'a little stronger' than that.

Until Trump gets new governors onto the Fed board, this means the group of voters will be both smaller and more hawkish, faced with an economy that is performing well and that may have more fuel thrown on the fire with tax cuts.

We're expecting a December rate hike, and these various factors mean there is upside risk to our call for two further rate rises next year. What's more, the long-end of the curve will also have to deal with additional supply from the Fed's balance sheet reduction programme.

The Fed is shrinking its balance sheet by reducing the amount of maturing bond proceeds it reinvests

Meet the 2018 Fed

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more