Russian ruble enters 4Q21 on a strong note

- 11 October 2021

- Russia

Russia's exceptionally strong current account surplus helped the ruble outperform its peer currencies in 3Q21 and is likely to keep doing so in 4Q21. As a result, we see USDRUB appreciating to 70.0-71.0 in the coming month. For the medium term, fast local capital outflow and global USD strengthening should be a factor limiting ruble appreciation

| 40.8 |

3Q21 current account surplus, US$bnUS$82.2bn for 9M21 |

| Higher than expected | |

Current account fundamentals strengthened in 3Q21

Russia's current account recorded the largest ever quarterly surplus of US$40.8bn in 3Q21, exceeding our US$32bn expectations and hitting the top of the consensus range. We take the headline print positively and have the following observations:

- Non-fuel export growth accelerated to 55% YoY in 3Q21, despite a somewhat adverse base effect, as Russian exporters of metals, select fertilizers, and agriculture products enjoyed higher demand and stronger pricing environment.

- Meanwhile, import growth was restrained on both the goods and services segments (Figure 1), reflecting still limited outward tourism and the moderation of merchandise imports after a very strong spike in 2Q21.

- Still, despite the moderation, merchandise import growth at 30% year-on-year in 3Q21 appears elevated relative to the exchange rate performance: even though the ruble continued strengthening to EUR (EU accounts for 1/3 of Russia's imports) and USD, by 3Q21 EURRUB and USDRUB have only returned to levels seen in 3Q20 (Figure 2). One explanation to this dynamic is the substitution of foreign travel with consumption of imports, in addition to some recovery in local investment activity.

- Finally, fuel (crude oil, natual gas, LNG, oil downstream), accounting for 48% of Russia's export proceeds in 9M21, benefitted in 3Q21 from both a better pricing environment and volumes (Figure 3). The likely seasonal increase in gas export volumes in 4Q21 combined with continued easing in OPEC+ restrictions allow for expecting further growth of Russian exports per US$1/bbl in 4Q21.

- Thanks to an increase in volumes and prices, natural gas exports increased from US$16.7bn in 9M20 to US$33.1bn in 9M21, reaching 20% of Russia's fuel exports. Assuming a further increase in volumes and moderation in prices, Russia's gas exports may reach US$15.0-15.5bn in 4Q21.

Taking into account the trends in the non-fuel sector, expected US$75/bbl Urals price for 4Q21 and assuming increase in export volumes, we see the 4Q21 current account surplus in the US$40-45bn range, suggesting a full-year figure of c.US$125bn, or c.7.5-8.0% of GDP.

Figure 1: 3Q21 current account exceeds expectations on strong exports and restrained imports

Figure 2: Merchandise import growth moderated but remained elevated relative to FX rate dynamic

Figure 3: Fuel exports up thanks to prices and volumes

| 33.9 |

3Q21 net private capital outflowUS$58.9bn for 9M21 |

Local private capital outflow remains the main drag

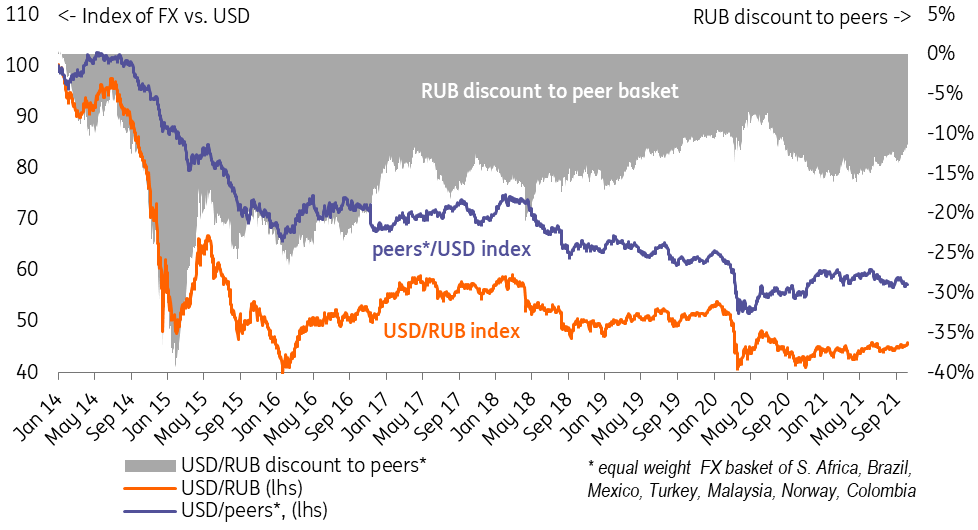

- Looking at the broader balance of payments picture, it appears that the current account surplus was the key driving force behind the ruble's positive performance in 3Q21 vs. USD (Figure 4) and peers (Figure 7).

- FX interventions were not an issue, as they only sterilized 31% of the current account surplus in 3Q21 thanks to the non-fuel support factors to the latter. We believe, in 4Q21 FX purchases are also unlikely to exceed 30-35% of the current account surplus, leaving around US$30bn of unsterilized surplus until the year-end.

- 3Q21 was also a successful quarter in terms of portfolio infows into the local currency public debt market (OFZ), which were close to US$6bn after negative US$4bn in 1H21. This recovery was supported by the toning down of Russia's foreign policy tensions, hawkish central bank, and a generally calm mood on the global debt markets, which however proved fragile after the tightening in the Federal Reserve rethoric caused a spike in UST yields and led to more bullish USD expectations.

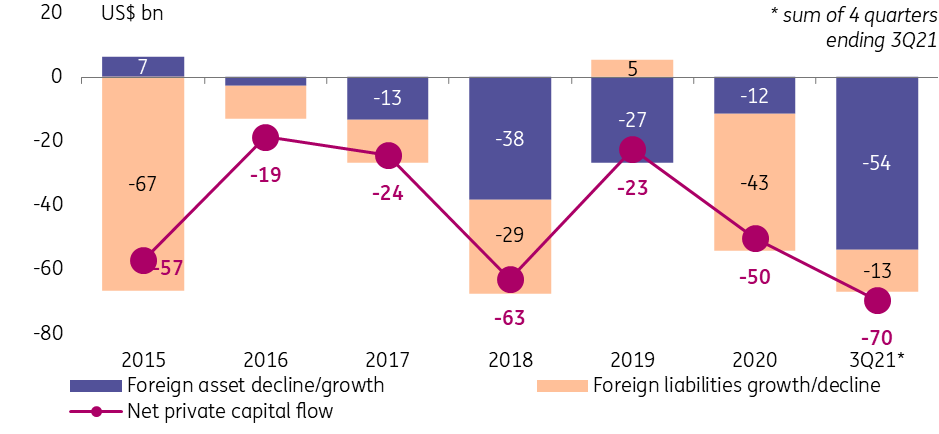

- Our biggest concern and a major drag on the ruble is the local private capital outflow, which picked up to US$33.9bn in 3Q21 to US$58.9bn for 9M21 (US$69.5bn over 4 quarters). The foreign debt data, that allows a detailed analysis of the capital flow structure, will be released on 13 October, but the preliminary numbers show (Figure 5) that after a brief improvement in 2020, the capital outflow structure is back to its usual focus on accumulation of foreign assets.

- Looking deeper into the foreign asset flows (FIgure 6), one can see a return to standard outward FDI of around US$30bn per year accompanied by a comparible accumulation of more liquid foreign assets. The latter may suggest a potential for reversal in case of more favourable conditions for the capital flows, but the catalysts for such a move remain incertain.

The overall balance of payments picture supports our take that the private capital outflow remains a factor limiting ruble's appreciation in the medium term. The structure and dynamics of the capital account point at a low appetite for capital locally, which combined with external limitiations (foreign policy, global risk mode) keeps the ruble undervalued, making it continuously favourable for trade balance. A mirrored shrinking of the current account surplus and net capital outflow under more or less stable exchange rate would be a sign of a reversal in the trend.

Figure 4: Private capital outflow remains an issue

Figure 5: Private capital outflow is driven by accumulation of foreign assets

Figure 6: Outward FDI is back to US$30 bn a year, accumulation of other foreign assets is also noticeable

Figure 7: Ruble was stronger than its peers in 3Q21

Near-term ruble outlook improved, but ruble's stabilisation at the lower bound of the USDRUB70-75 range is an optimistic case

An exceptionally strong 3Q21 current account prompts us to improve our full-year outlook by around US$30bn to US$125bn in 2021. Thanks to that, we now see a possibility of ruble appreciating to 70-71 in the coming 4 weeks and see potential room for improvement of our year-end target of 73.0. Taking into account partial sterilization of the current account via FX purchases, ruble fair value should be improved by USDRUB 2.0, all else being equal. Nevertheles, ruble's stabilisation at the lower bound of the USDRUB 70-75 range in the medium-term remains an optimistic scenario, requiring moderation in the private capital outflow and stabilisation of USD to major currencies, none of which is part of our base case at the moment.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more