Russian data supports the central bank’s hawkish bias

- 9 February 2022

- Russia

Although January's CPI is below consensus, its structure and continued acceleration in February highlight near-term pro-inflationary risks. Simultaneously, numbers on employment, salaries, consumption, and lending are relatively strong. That, in our view, supports the hawkish stance that the Bank of Russia is likely to reiterate on 11 February

Headline CPI below expectations, but the devil is in the details

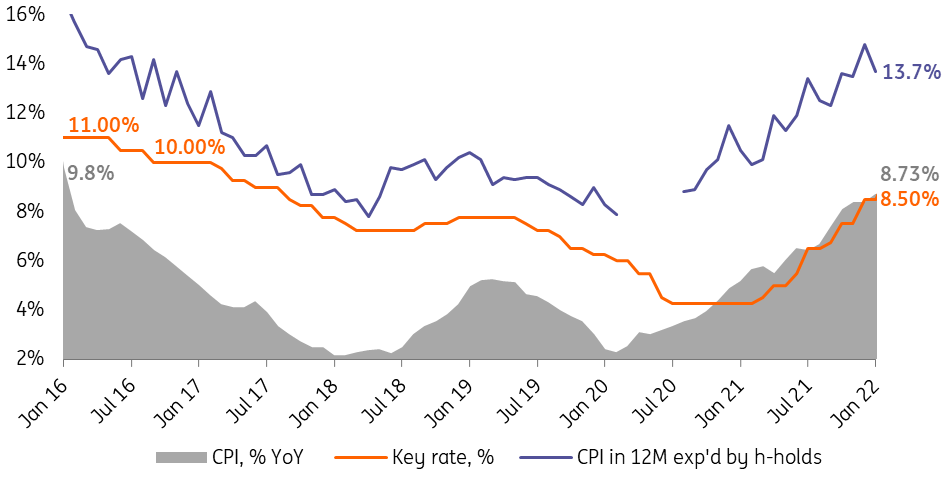

Russian headline CPI accelerated from 8.39% year-on-year in December 2021 to 8.73% YoY in January 2022 (Figure 1), which is 0.2 percentage points below the consensus forecast and our expectations. That's the only good news so far. Going beyond the headlines:

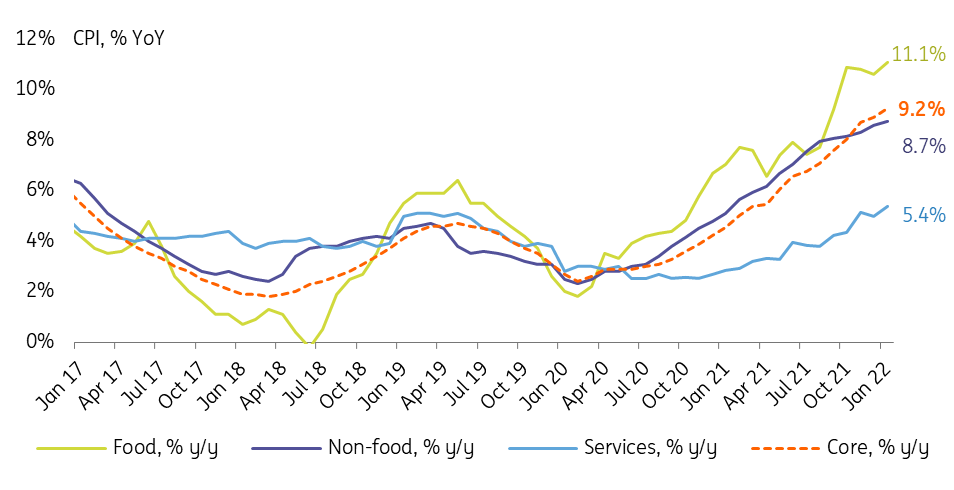

- Core CPI at 9.24% YoY exceeded the headline number, for the third month in a row (Figure 2).

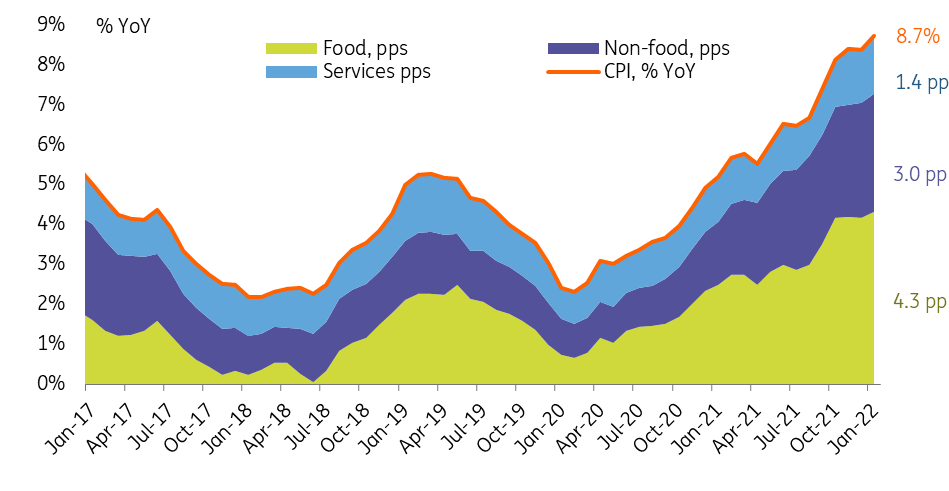

- The structure of headline CPI growth (Figure 3) shows that the acceleration in January was broad-based, with a 0.3 percentage point increase in the annual rate evenly split between food, non-food products, and services.

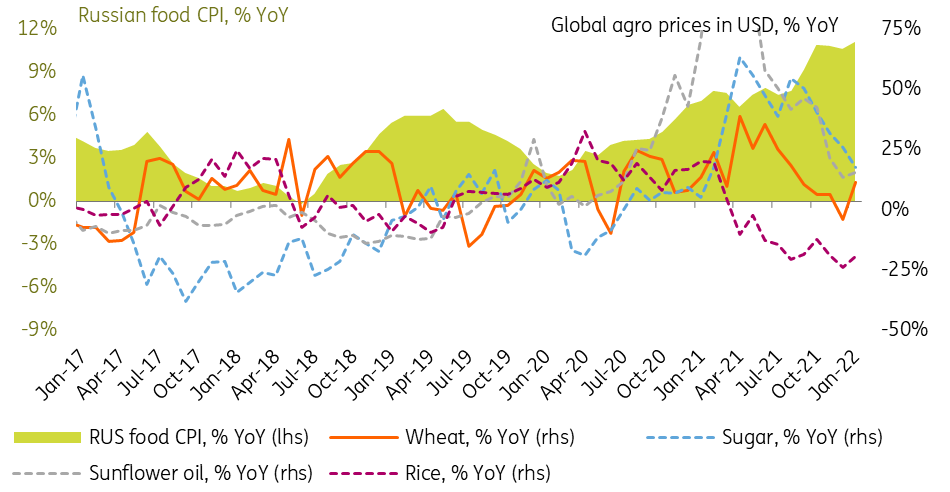

- The slight uptick in local food prices was supported by global agro commodity prices which resumed growth in January.

- Weekly CPI data points at a further acceleration, to 8.8% YoY as of 4 February. Granted, the seasonal spike in tourist services costs was the key contributor to this acceleration, but the food and non-food product segments also showed an uptick.

Overall, the January CPI numbers somewhat lower the risk of CPI reaching or breaking out of the 9.0-9.5% YoY range, but the underlying structure suggests near-term CPI risks remain elevated in Russia.

Figure 1: Headline CPI accelerates to 8.7% YoY in January, amid moderating household expectations

Figure 2: Core CPI exceeds headline rate for the third month in a row

Figure 3: CPI acceleration in January is broad-based

Figure 4: Uptick in local food prices was supported by global trends

Local demand fundamentals stronger than expected

Russian retail trade picked up from 3.1% YoY in November to 5.4% YoY in December, exceeding the 3.5% YoY consensus on the faster consumption of non-food products. As a result, full-year retail trade increased 7.3% YoY in 2021, exceeding the pre-Covid levels by 3.9%. The consumer demand fundamentals behind this appear to be strong, at least for the near term:

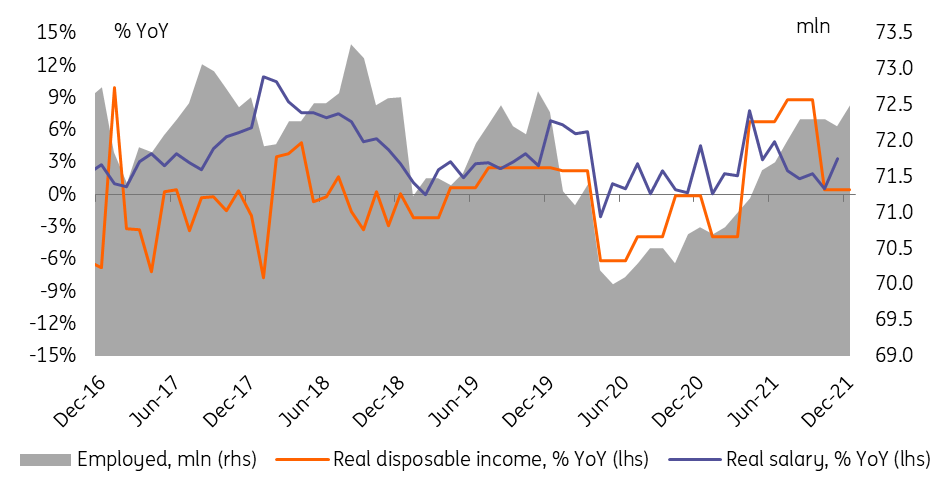

- Despite a material acceleration in CPI over 2021, real disposable income increased by 3.1% YoY last year, exceeding the pre-Covid levels by 1%. Salary growth totalling 2.8% YoY in the year to November (driven by manufacturing, construction, and trade sectors) was only one of the contributors, while real pensions were up 4.1% YoY.

- While the unemployment level remained at 4.3% in December, the number of employed continued to increase, reaching 72.5 mln, the highest level since November 2019. (Figure 5)

- In addition to income, consumption seems to be supported by an increasing reliance on leverage, as retail lending growth continued to accelerate, reaching 25% YoY in 2021, up from 14% YoY in 2020. Meanwhile, retail deposit growth (adjusted for FX revaluation) picked up from 4% to 6% only. That suggests that the savings rate most likely declined last year.

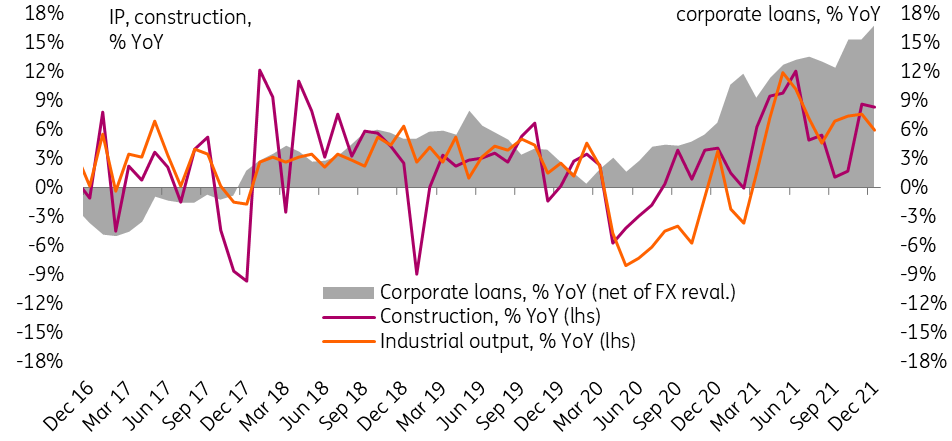

Corporate activity also exceeded expectations, with December industrial output up 6.1% YoY (+5.3% for 2021) thanks to strong local manufacturing output, while construction growth posted an 8.4% YoY increase in December (+6.0% YoY for 2021) even though housing construction posted a decline. The expansion in local producer activity took place amid a gradual pick up in local corporate lending (Figure 7), suggesting this was broad-based. We also do not exclude that the year-end activity received a boost from the state sector, as federal budget spending jumped 24% YoY in December after 5% YoY growth in the year to November, as the government postponed 19.5% of the annual spending plan until the last month of the year.

The December activity data suggests that the near-term trends are supportive. Nevertheless, we maintain our expectations of GDP growth decelerating from the just reported 4.6% in 2021 to 2.0-2.5% YoY in 2022 on the reduced scope for a post-Covid recovery amid a likely deceleration in lending growth.

Figure 5: Household income trend supported by recovery in employment, social payments

Figure 6: Reliance on borrowing is also increasing

Figure 7: Corporate activity supported by external and local demand in 2H21

The recent set of data supports the CBR's hawkish bias

December activity and January CPI are the last set of important data to be released ahead of the 11 February key rate decision. We believe that the further acceleration of CPI in January-February and stronger-than-expected local demand at the end of 2021 support the Bank of Russia's narrative of elevated inflationary risk for the medium term. We reiterate our call that the Bank of Russia is likely to make a 100 basis point hike, reaffirm its hawkish guidance, and raise its official CPI and key rate guidance for 2022.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more