Russian CPI underperforms in August, supporting rate cut

- 5 September 2019

- Russia

Russian inflation slowed to 4.3% YoY in August, below expectations, making us more comfortable with our 4.0% year-end forecast and reinforcing the case for the key rate cut on 6 September. Yet food and non-food CPI remain a watch factor for the mid-term along with the end of the harvest season and acceleration of budget spending growth

| 4.3% |

Russian CPI growth, August (YoY)Down from 4.3% YoY in July |

| Better than expected | |

Russian CPI slows in August thanks to monthly deflation in fruits and vegetables

Deceleration in the Russian CPI growth from 4.6% year-on-year in July to 4.3% in August is a positive surprise, as it underperformed the consensus forecast of 4.4% and our cautious 4.5% expectations.

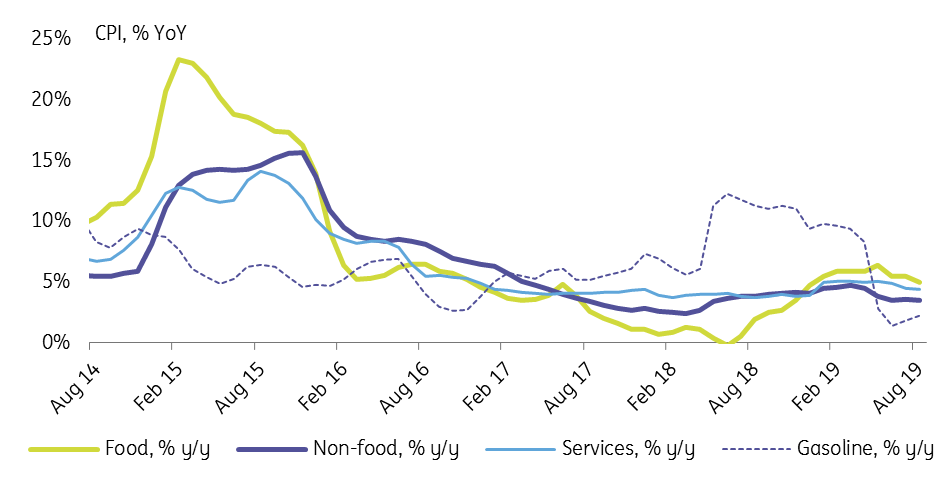

This time the food segment (c.38% of the CPI basket) was the key driver of the slowdown, with price growth there decelerating from 5.5% YoY in July to 5.0% YoY in August, mainly thanks to the strong 10.1% month-on-month deflation in the fruit and vegetable segment (the annual growth rate remained positive but decelerated from 5.4% to 1.3%. Noteworthy, prices for almost all other food items showed an acceleration in the annual growth rate.

Prices for non-food products and services decelerated by 0.1 percentage point to 3.5% YoY and 4.4% YoY, respectively, being a minor drag on overall CPI. We note that the gasoline prices, which is included into the non-food product segment, are posting continued acceleration - from 1.4% YoY in June to 1.8% YoY in July and 2.2% YoY in August, reflecting expiration of the agreement between the government and the oil majors, as well as the end of the high base effect.

Russian CPI growth by components (% YoY)

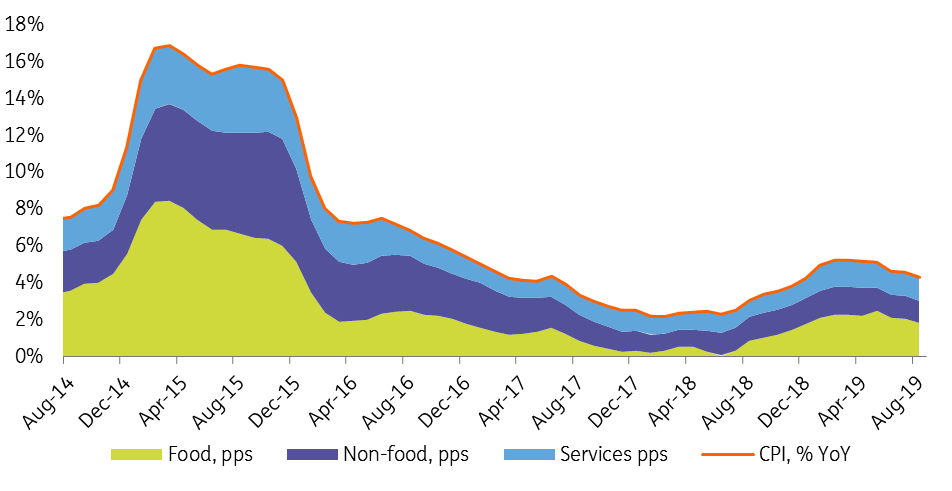

Russian CPI growth by components (contribution to total, in pps)

Year-end 4.0% YoY outlook confirmed, not improved

The August CPI result makes us more comfortable with our year-end forecast of 4.0% and a temporary drop to 3.0% in 1Q20 on the high base effect. Our main hopes for a further slowdown from here are mainly related to the favourable situation on the global grain market, to which Russian food inflation has been historically sensitive.

Yet unlike some other market participants, we are reluctant to further improve the mid-term outlook due to several considerations:

- The food price growth outside fruit and vegetables fails to show noticeable deceleration despite the favourable base effect, while the shifted seasonality of the harvest this year may suggest that the fruit and vegetable deflation may end very abruptly this year;

- Acceleration in the gasoline price growth remains a watch factor;

- The 4.7% RUB depreciation to USD seen in August may still have a minor inflationary effect in the mid-term;

- The upcoming acceleration in the budget spending growth from 2% YoY in 1H19 to 8-13% drafted for the full-year could remove some of the demand-driven constraints to CPI.

Global wheat price growth and Russian food CPI, % YoY

Case for a 25 bp key rate cut reinforced, but do not expect extra dovishness

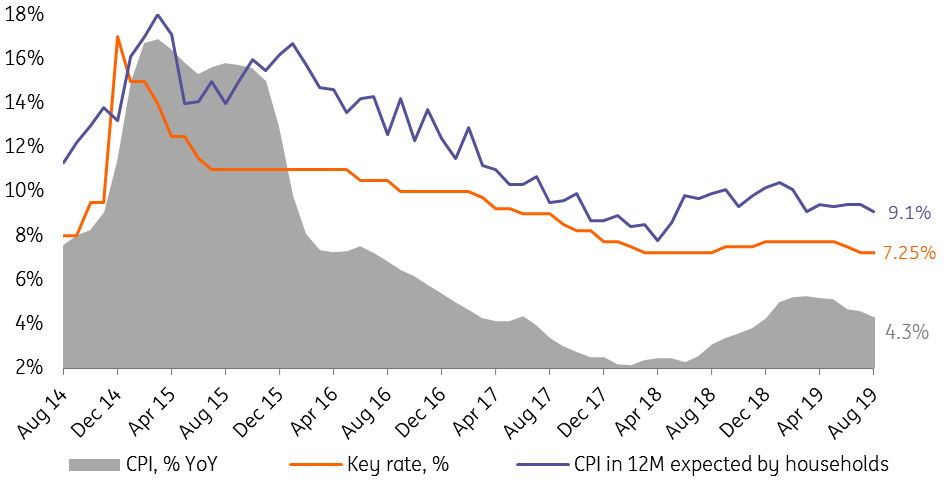

In any case, the 0.3 ppt slowdown in the CPI growth in August strengthens the case for a 25 bp rate cut at the upcoming 6 September meeting, which was already priced in by us and the market based on the weekly CPI performance, improvement of the inflationary expectations by households and corporates, stabilization of the RUB exchange rate, and the poor activity reading for July. We wrote about it in some detail on 2 September https://think.ing.com/snaps/russia-central-bank-to-cut-and-hold/

At the same time, above-mentioned concerns regarding the mid-term CPI trend make us doubt that the Central Bank of Russia will be more aggressive in terms of rate action. Also, the increased global market volatility and ongoing discussion about investing part of the state savings locally may even contribute to a more cautious tone of the CBR commentary.

Russian CPI, inflationary expectations, and key rate

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more