Russian CPI soars, challenging central bank forecasts

- 3 November 2021

- Russia

Russian CPI jumped 0.7 percentage points to 8.1% year-on-year in October, exceeding market expectations. The good news is the volatile food segment accounted for 83% of the acceleration. The bad news is that weekly CPI needs to slow down from the current 0.21% to 0.09-0.15% to fit into Bank of Russia's fresh year-end forecast. This looks too optimistic

| 8.1 |

October CPI, % year-on-yearup from 6.7% in September |

| As expected | |

Good news first

Russian CPI picked up from 7.4% YoY in September to 8.1% YoY in October, exceeding the market consensus but meeting our expectations. Looking into the numbers, we see both good and bad news. Good news first:

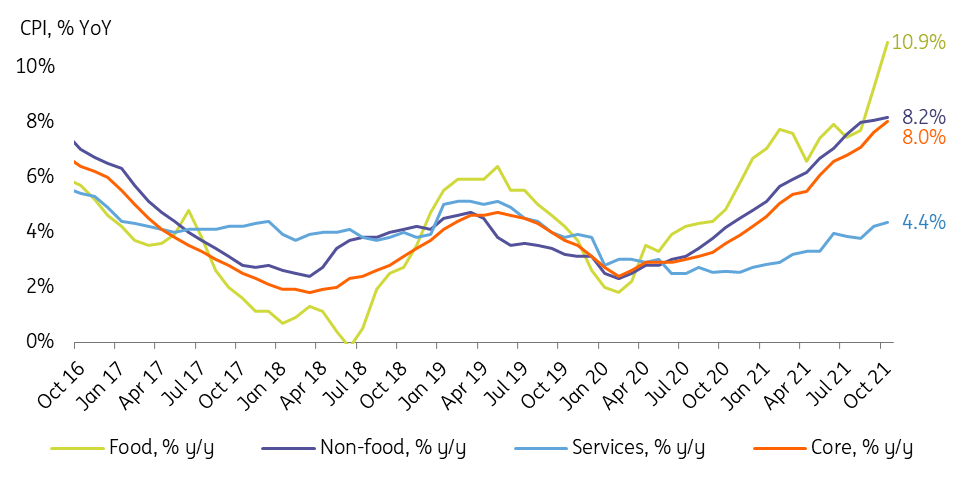

- Unlike the September picture, this time core CPI (Figure 1) is reported below the headline figure, suggesting a higher contribution of volatile components to the current acceleration of inflation.

- In October, 83% of the CPI acceleration is attributable to the food segment (Figure 1), higher than the 75% seen in September. The food segment is, by nature, more volatile than others and is heavily affected by seasonal and climate factors, including harvest. The trends in CPI in non-food products and services are much calmer.

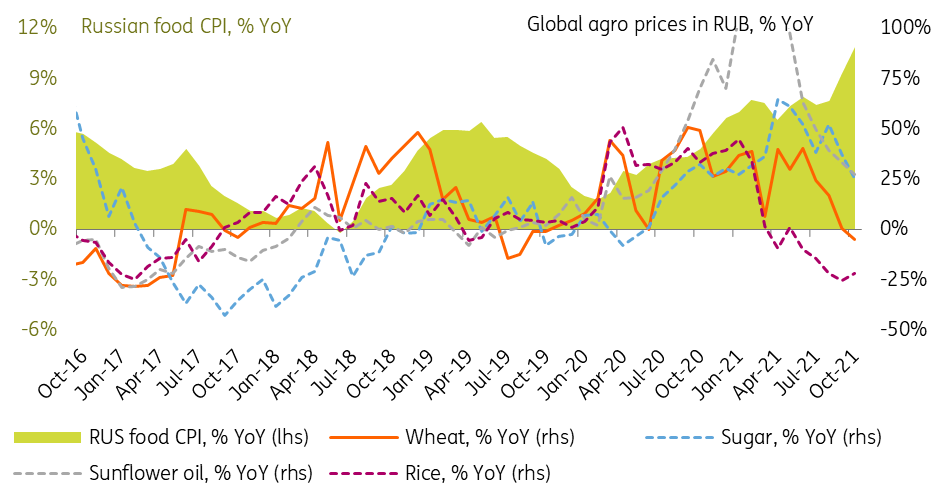

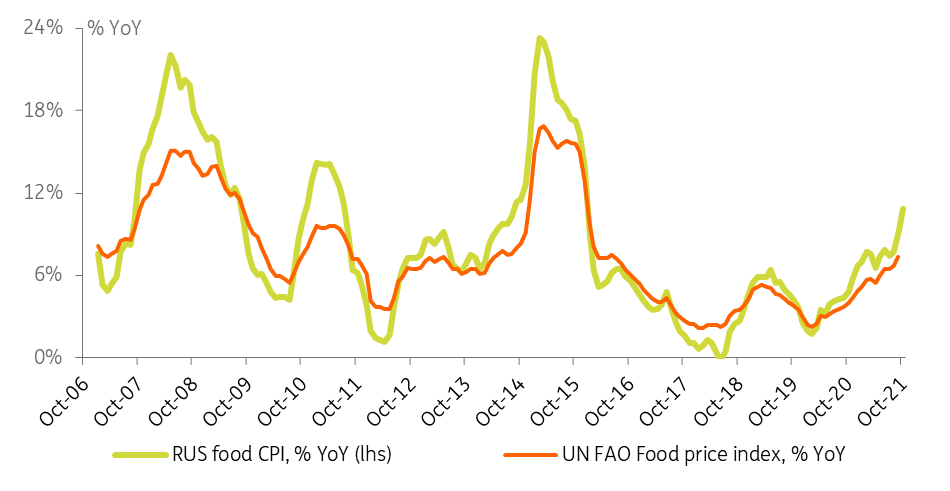

- The sharp acceleration in local food prices (to 10.9% YoY in October) goes against the easing in the core global agricultural commodity markets (Figure 2). History shows (Figure 3) that any decoupling of local Russian prices from global trends tend to be temporary.

Figure 1: Food prices were the key driver of faster CPI in October, core CPI is slightly lower than the headline 8.1%

Figure 2: Pick-up in local food prices goes against easing in the global pressures

Figure 3: Decoupling from global food prices is unlikely to be sustainable in the longer run

Now, to the bad news

At the same time, our take on the October data is also mindful of the negatives:

- The data confirms the low predictability of food price growth in Russia. We do not exclude that the current price spike, which has become particularly noticeable since the middle of September, at least partially reflects a release of inflationary pressures accumulated before the parliamentary elections.

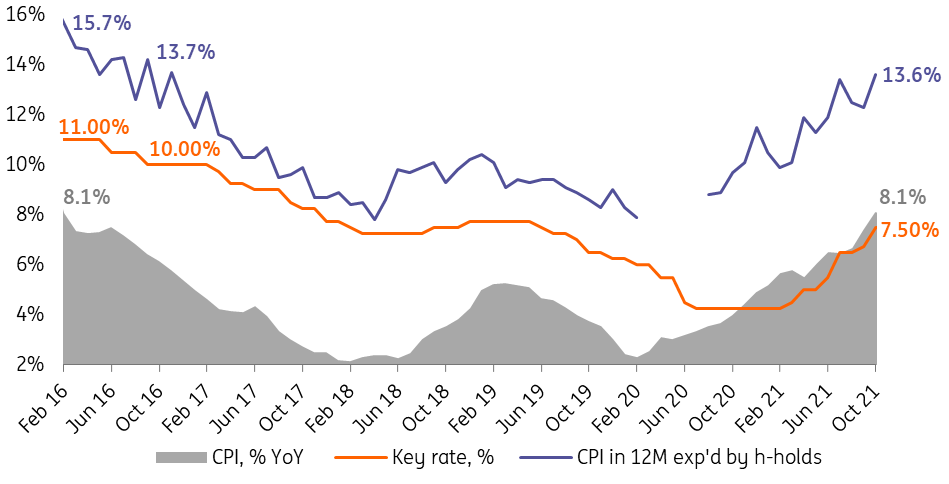

- The acceleration in the CPI, regardless of the drivers, tends to negatively affect households' expectations (Figure 4), which in itself could add to actual inflationary pressure in the medium term.

- According to the recently published quarterly monetary policy review, the Bank of Russia believes that the reasons for the deviation of the current CPI trend from the long-term target of 4% are at least in part sustainable. Record low unemployment of 4.3% and relatively robust credit growth suggests that demand-side factors are also at play, in addition to global supply chain disruptions.

- In order to justify the fresh CBR forecast of year-end CPI of 7.4-7.9% YoY, the weekly CPI prints have to drop from the current 0.22-0.30% week-on-week to 0.09-0.15% until the year-end, which looks optimistic given the deterioration of the global inflationary picture outside the food segment.

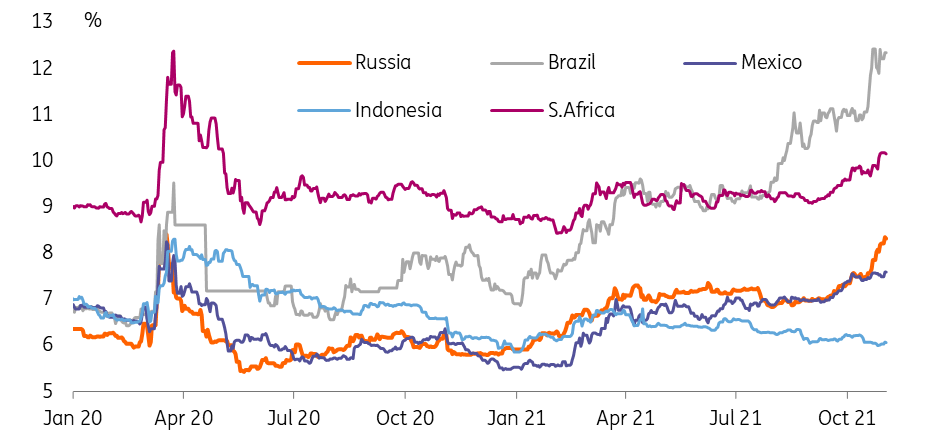

- We believe the actual CPI growth may reach 8.0-8.5% this year. The near-term trend should not be pivotal for the Bank of Russia's monetary policy decisions per se, but a series of misses on the CPI forecasts could be a challenge to the market trust in inflation targeting. Russian 10-year yields are up 63 basis points since before the last CBR monetary policy meeting, while the growth in peers Brazil, Mexico and South Africa is limited to 2-34 basis points for the same period. The sharp repricing at the longer end may point to some revision of the long-term inflationary expectations of the market participants, which probably needs to be addressed.

Figure 4: Regardless of drivers, faster CPI propels higher household expectations, which are relevant to the CBR

Figure 5: Russian 10-year yields may suggest the market is pricing in a deterioration in the long-term CPI trend

Bank of Russia will remain under pressure to act

Food is the primary driver of the current CPI growth in Russia. On the positive side, this may be temporary. On the negative side, it still puts upward pressure on households' inflationary expectations. A slowdown of inflation to 7.4-7.9% YoY expected by the CBR is not impossible, but looks a bit optimistic at this point. Even though the near-term CPI developments are not guaranteed to trigger the Bank of Russia, they still may if the market starts challenging the long-term inflation target.

While initially we saw a 25 basis point hike at the upcoming 17 December meeting as a base case, a sharper, non-standard move of 50 basis points now looks equally possible. In any case, there are still plenty of data points ahead that might affect those expectations. As a reminder, the recent CBR forecast suggests that any option between 7.5-8.5% key rate is on the table for year-end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more