Robust US growth, but it lacks breadth

- 30 January

- United States

The US economy looks set to post a sixth consecutive year of 2%+ real growth, led by strength in spending by high-income households and tech investment. But traditional capex and construction activity are treading water, and the economy is struggling to create jobs

Growth immune to the government shutdown

We have revised our US 2026 GDP growth forecast higher to 2.7% from 2.3%, in part reflecting a stronger fourth quarter of 2025. The government shutdown was thought to mean growth would slow notably in the fourth quarter, but the private sector has performed well and the October trade report was remarkable in that the deficit of $29bn was the smallest outcome since 2009 when the economy was depressed after the Global Financial Crisis.

This sharp narrowing of the trade deficit likely reflects delayed shipments related to hopes that the initial 'Liberation Day' tariffs would be cut. Given that it can take many months for products to be delivered by sea, these decisions take time to show up in US data. The trade situation will eventually normalise, but we think a 4Q GDP expansion of close to 2.5% looks plausible even with a rundown in inventories, rather than a little over 1% as previously predicted.

High income households and tech continue to drive growth

In terms of 2026, the K-shaped narrative surrounding the economy dominates in both the corporate and household sectors, and this should keep growth above trend in 1H 2026. The top 20% of households by income continue to spend strongly, boosted by high incomes and soaring wealth, while the bottom 60% are struggling as concerns about job security and the potential for tariff-induced price hikes sap sentiment. Some tax changes may help lower-income households at the margin, with higher tax refunds also expected this year, but the jury is still out on the potential timing and scale of the $2,000 “tariff dividend” payment mooted by the president.

Regarding corporate spending, we’ve seen four consecutive quarters where business capex outside of tech has contracted, yet investment in computing and software is up 20% year-on-year. This bifurcation looks set to remain a theme through much of 2026, although there is a sense that we may see some moderation in the pace of tech capex growth as business leaders and shareholders seek returns on the money spent. Similar patterns are expected for the construction sector.

At the same time, the jobs market continues to lose steam with Federal government worker lay-offs resulting in non-farm payrolls falling 173,000 in September. There were gains in November and December of 56k and 50k, respectively, but Federal Reserve Chair Jerome Powell’s assertion that the Bureau of Labor Statistics is likely overstating jobs growth by around 60k per month means that employment has stalled – a low-hire, low-fire economy.

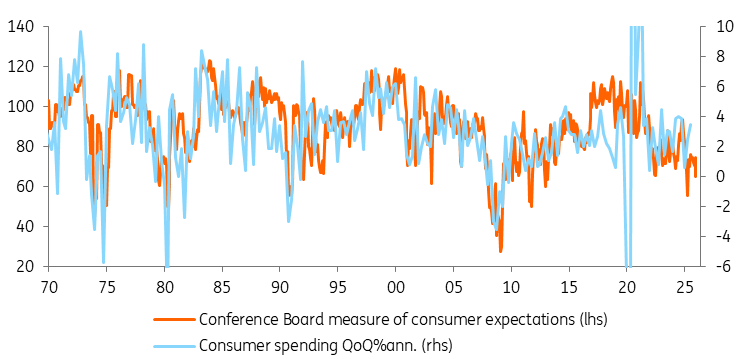

Consumers continue to spend despite weak sentiment

Inflation and job worries mean two more Fed cuts

The shutdown-delayed inflation data confirmed that tariffs are not having the immediate impact on prices that most feared. We can’t rule out that it will lead to higher prices eventually, as there is a belief that some companies are delaying passing on the higher costs to consumers until the Supreme Court rules on IEEPA tariffs. But even if the Supreme Court rules against those specifically, President Trump’s team will be looking to swiftly reinstate tariffs via an alternative route.

Nonetheless, the fact that tariffs are coming through so slowly gives more opportunity for lower energy costs, slowing housing rents and weaker wage growth to mitigate and allow inflation to continue trending down towards 2%. Given this backdrop and the caution surrounding the jobs market, we expect the Fed to cut interest rates twice more in 2026. However, the first cut is now more likely in the second quarter rather than in March as we previously forecast.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s Arnold moment – why strategy over spectacle matters

- This bundle contains 15 Articles