The road haulage sector’s recovery is set to stay in the slow lane

- 15 January

- Transport & Logistics

The road transport sector presents a mixed picture in 2026. Companies in industrial goods still face lagging demand, and there’s more traction in consumer products and building materials. Carriers have also reduced their capacity. Volatility is here to stay, but that’s part of a new normal. Meanwhile, the momentum for replacements is growing

European road transport continues to move forward unevenly in 2026

Transport demand continued to recover in 2025 after a setback in 2023, yet ton/km volumes remain on average about 1.5% lower than before. For 2026, we expect a stable demand growth of around 1%, with larger-than-usual variances between countries, freight segments, and fleets.

Protectionist trade policies, geopolitical instability, and their ripple effects on supply chains and consumer confidence will linger into 2026. However, 2025 demonstrated that goods trade is resilient and adaptable, and the economy performed better than expected. Road transport’s flexibility also proved beneficial during supply chain disruptions and unexpected conditions.

European road transport still sluggish, but on a recovering path

Evolvement of European road transport volume in million ton/km

Industrial goods transportation not out of the woods yet

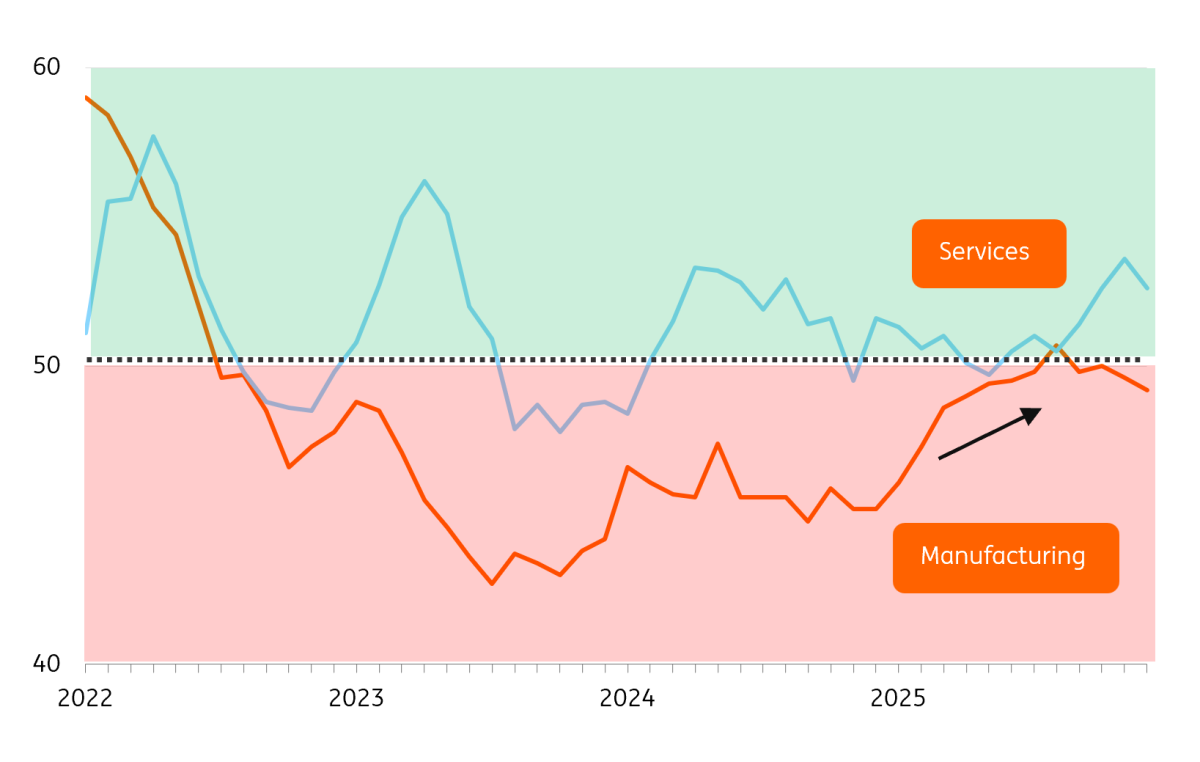

Industrial goods represent a large share of road transport. Manufacturing shippers may have hit bottom; the Purchasing Managers Index (PMI) climbed out of a deep trough by mid-2025 but is not signalling growth just yet. The foundation for recovery remains fragile, with heavy industries under persistent competitive pressure, although food industries show better prospects.

Sluggish transport demand is reflected in the 2025 figures from leading players such as DSV and Kühne & Nagel. Energy-intensive sectors (steel, chemicals) continue to struggle to compete, with production cuts and site closures across Europe – especially in Germany, which accounts for over 25% of European road transport. Some relief has come from lower energy prices and government support. With ramped-up investments in defence and infrastructure, improvements are expected in 2026. The automotive industry, another key segment for road transport, is also likely to see a gradual recovery.

*Relatively high savings-rate still illustrates low confidence and people’s hesitance amid uncertainties in the global (geopolitical) environment.

Eurozone manufacturing PMI out of deep negative territory now

Eurozone purchasing managers index for services and goods (<50 = contraction)

Consumer products and building materials support growth in 2026

Transportation of consumer goods shows a brighter outlook, supported by rising purchasing power and persistently low unemployment. Consumers remain cautious and are saving more than they used to, but European consumer spending on goods is on the rise, growing 2% in the first three quarters of 2025.

Demand for consumer product transport is set to continue outperforming industrial goods in 2026. A more stable international policy environment could unlock additional spending. Construction activity is also expected to grow, triggering higher volumes of building materials on European roads.

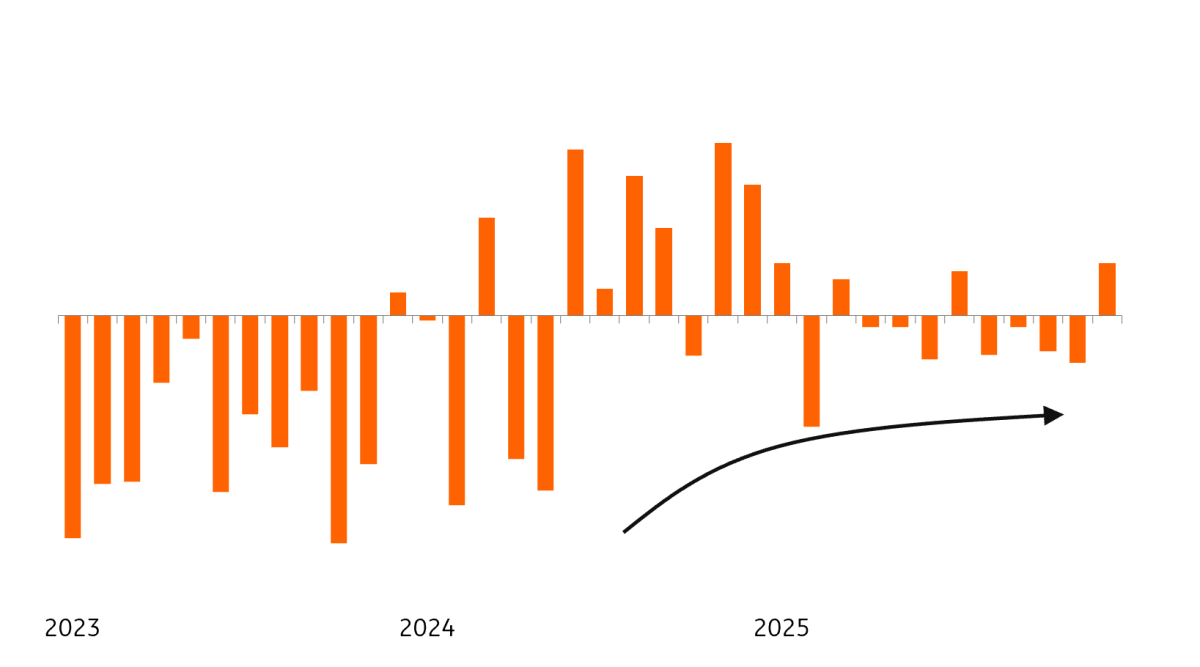

Transport volume across Germany struggles to continue the recovery

Total truck mileages on German motorways (MAUT) YoY (adj. for working days)

European picture benefits from relatively strong performers like Spain

Current MAUT figures still indicate stagnant volumes across Germany. The broader European road transport story is more positive, though. Countries like Spain and Poland show stronger growth, in line with robust GDP performances. Over the course of 2026, the impact of extensive investment packages in infrastructure and defence should materialise, reducing Germany’s drag on European transport demand.

Geopolitics set to be a key player in this year's transport market outlook

Geopolitical uncertainty will continue to affect supply chains and transportation in 2026. With protectionism on the rise, global trade growth will remain fractional, with higher trade barriers incentivising regional sourcing where possible. Europe recognises the need to invest in competitiveness and domestic production capabilities, which would bolster intra-EU transport over time.

A key factor to watch in 2026 is the evolution of the war in Ukraine. An end to the conflict and the start of reconstruction would significantly boost transport demand, especially in Central and Eastern Europe.

Reduced trucking capacity supports the market

Transport companies reduced their capacity after the demand contraction of 2023. The European haulage capacity index was down almost 1% in September 2025 compared to a year earlier (Trimble/Transporeon). Efficiency gains (higher occupancy rates) also reduced capacity needs somewhat. Eurostat has confirmed that companies have trimmed their fleets and taken older, rigid trucks out of service. Bankruptcies and remarketing of used trucks outside Europe contributed to this trend.

Momentum for replacements picks up

The market setback, as well as uncertain market conditions and delayed deliveries of previously ordered equipment, is keeping hauliers and fleet owners cautious – but the scope for postponement is reaching its limits. On balance, we believe that the momentum to catch up on investments has grown. Investing means staying up-to-date and ready for the future, and uncertainty seems to be the new normal.

Negative investment considerations:

- Growth prospects for road transport in 2026 are limited, with volumes still hovering below 2022 levels.

- There’s still (older) equipment on the sidelines.

- Uncertainty about the future CO2 reduction trajectory for truck manufacturers and lingering constraints on investment in e-trucks (charging infrastructure missing fiscal support) could lead to delaying investments.

- Predictive analytics, real-time track and trace and optimisation of planning result in efficiency gains within existing fleets.

Positive investment considerations:

- Deferred replacement demand across Europe still offers a catch-up effect.

- Equipment prices have normalised after the 2020-2023 production constraints and prolonged lead times. The return of a buyer’s market improves investors’ bargaining positions.

- CO2-linked truck toll systems in several countries, including Germany, increase the operational costs of older trucks and support replacement.

- Policy pressure on manufacturers (CO2 targets) and larger clients (CSRD) still supports demand for new equipment.

- Efficiency improvement is an incentive for carriers to invest. New generation trucks like the new DAF XF/XG are typically 10-15% more fuel efficient than the previous generation.

- Lower interest rates make financing cheaper. Between late 2023 and mid 2025, the Euribor monthly rate halved from around 4% to 2%.

Margins under pressure and require continued attention

European road transport is dominated by fixed contracts with shippers, but spot rates (roughly 20% of the market) provide short-term guidance. Spot rates converged with contract rates after the 2023 setback, revealing market weakness. International road transport prices rose 2-3% year-on-year in autumn 2025 (IRU/Upply, Transporeon/Trimble), but this did not fully offset cost increases.

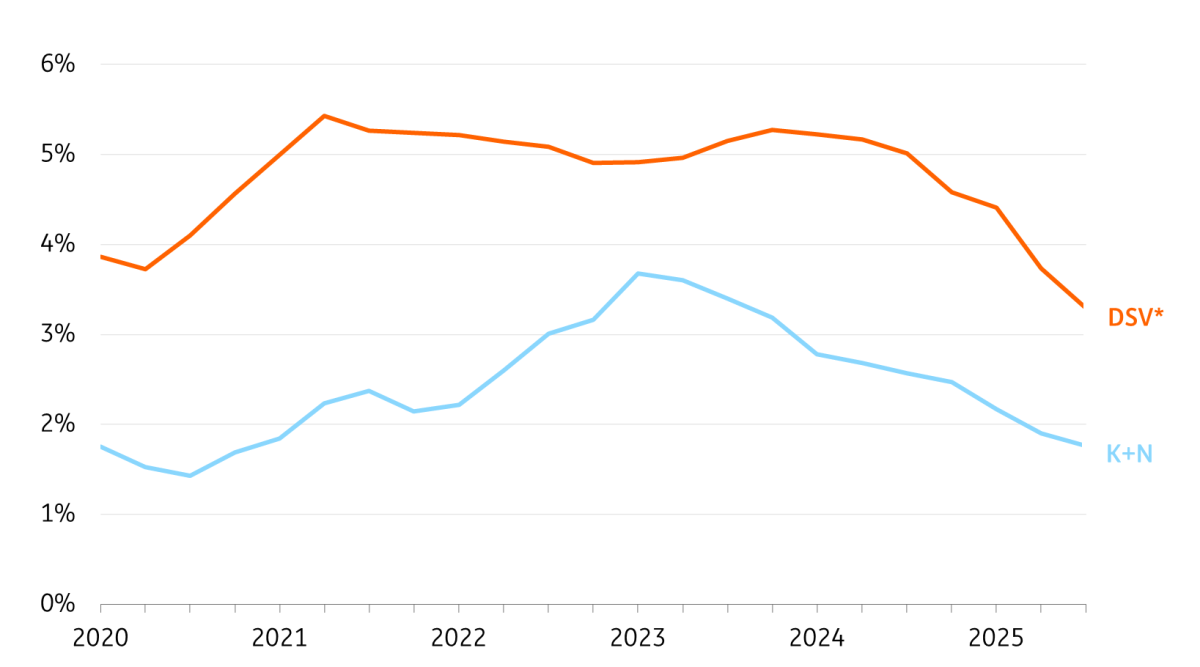

EBIT margins of major players like DSV and Kühne & Nagel have returned to pre-pandemic levels after elevated margins in 2021-2023. Passing on wage and toll increases will be challenging in 2026, especially in countries like the Netherlands and Belgium, where toll costs rise. Lower diesel prices (20-25% of total costs) may offer some relief.

Road transport margins large logistics services providers under pressure and back around pre-pandemic levels

EBIT road transport divisions DSV + Kühne & Nagel (primarily European focussed), rolling four-quarter average

Companies challenged to pass on wage and toll increases push costs in 2026

Freight rates remain fragile in the current market, despite less offered capacity. Strong client relations continue to be important for passing on expected cost increases in 2026. This especially holds true in countries like the Netherlands and Belgium, which will see (higher) toll costs.

As we expect continued excess supply in the oil market to keep diesel prices down (20-25% of total costs), this will likely offer some counterweight. Many larger road transport companies have already diversified into adjacent activities. Logistics services, such as supply chain management, contract logistics and warehousing, are more profitable.

Truck driver hiring shortages could catch up quickly again

Future trucking capacity growth in Europe is limited by the availability of drivers. This is an important future success factor. Carriers generally found it easier to recruit drivers in 2025 than they have recently. However, the labour market remains tighter than before and recruiting sufficient drivers to make up for outflow could still be a challenge across segments and countries. Recruitment (and marketing) therefore requires ongoing attention.

The setback in transport demand has brought some relief recently, but unlike in the past, pressure remains. The World Transport Association (IRU) still counts 426,000 unfilled driver positions across Europe. This is why forward-looking (larger) companies are permanently hiring drivers throughout the economic cycle.

Reasons why shortages are here to stay (and likely to grow):

- Most truck drivers no longer appreciate long working hours and weeks on the road in international trucking, as they prefer more time with their families and can earn similar wages in other jobs. This is certainly the case in Western Europe, but the trend has now spread to Europe’s market leader, Poland, which is among the countries with the largest shortages.

- The availability of potential workers in EU countries (working-age population) is limited for demographic reasons.

- The labour force ages, which pushes up outflow (EU truck drivers are currently aged 47 on average, with one third older than 55), whereas the workforce below 25 years is only around 4-5%.

Carriers are broadening their recruitment efforts outside of the EU and even in Asia. Forward-looking, larger companies continue to hire and educate a continuous flow of truck drivers throughout the cycle. An ongoing problem remains the relatively low representation of women in the sector – this is slowly creeping up, but there still exists a far lower number of potential applicants.

More consolidation expected to stay competitive and to meet requirements

The European road haulage sector remains fragmented, with large international trucking companies such as Girteka, Warberer’s, Primafrio and Raben and a large majority of small and medium-sized companies. Larger trucking companies are generally getting bigger because of the combination of autonomous growth and acquisitions, while more drivers are also starting their own independent companies.

We have seen more bankruptcies in the last two years, but companies still lean on the strengthened position seen in the years 2020-2023. Still, the finances of many smaller companies are eroding, and going forward, small businesses face an investment challenge to keep up with progress in ICT and sustainability. The ageing of company owners also poses succession issues. In turn, we expect an ongoing strong trend of consolidation in the sector.

Regulatory focus points for road haulage on its way to 2030; softened, but still relevant

On the road to 2030, a range of new EU regulations will be enforced and tightened. Several EU reporting and sustainability policies have been scaled back significantly, limiting CSRD obligations to companies with more than 1,000 employees and either turnover above €50 million or a balance sheet above €25 million. Enforcement of ETS2 has also been delayed. The EU’s CO2 regulation for truck manufacturers has been softened and will be reviewed earlier than planned.

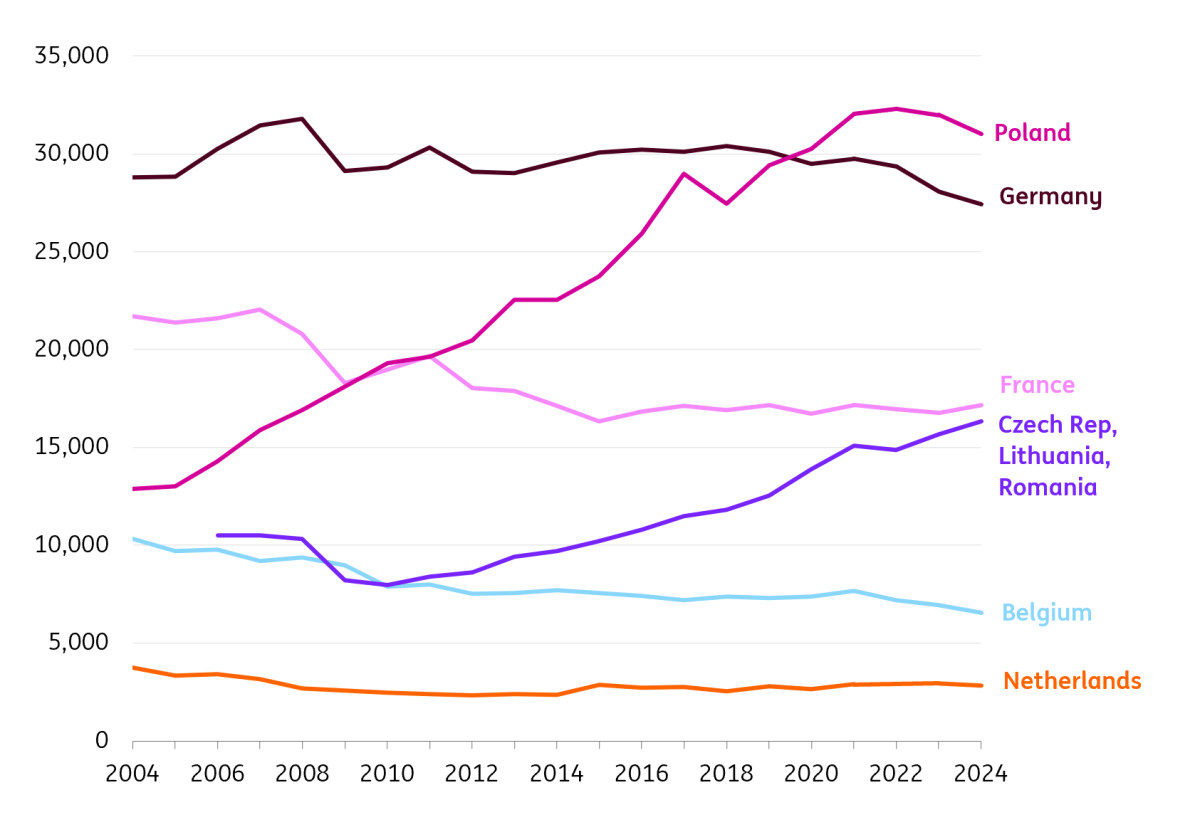

EU extension success story for Poland reached its peak

Vehicle km's in millions per country, per year

The centre of gravity in international transport has shifted east in the last two decades

Since the EU’s major enlargement in 2004, international road transport has increasingly shifted towards Poland due to lower labour costs. This has reduced transport activity from the Netherlands, Belgium, Germany, and France, while Poland has become the market leader. The Dutch fleet’s share of international kilometres fell from 60% to just over one-third, and the declining mileage of Dutch‑registered tractors shows the trend persists.

Many Western firms have responded by setting up subsidiaries in Eastern Europe. While trucks often carry Eastern European plates, much of their activity still occurs in Western Europe. Market enlargement increased competition and lowered international transport costs for shippers and consumers, and the EU’s Mobility Package aims to improve transport and labour conditions. The vehicle “return home” rule has been scrapped, but drivers must still return home every four weeks, unless they opt out. Poland now faces labour shortages and rising wages, making Romania and other countries more attractive. This shift is likely to continue as long as wage gaps remain.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more