Rising rice and energy prices in the Philippines fuel inflation concerns

The 'crucial 3': will the return of rice and energy price spikes delay Bangko Sentral ng Pilipinas’ easing plans?

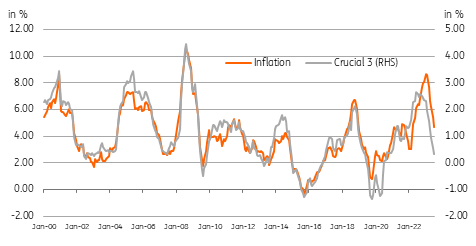

Philippine inflation on the downtrend... for now

Philippine inflation hit a peak of 8.7% year-on-year in January 2023, driven by a mix of resurgent domestic demand and elevated global commodity prices. Inflation has since moderated to 4.7%YoY as of July.

A string of aggressive monetary tightening (rate hikes totalling 425bp) on top of moderating global energy prices helped nudge the inflation path towards the Bangko Sentral ng Pilipinas’ (BSP's) inflation target of 2-4%. The BSP projects inflation will settle back within target by the fourth quarter.

However, recent developments could derail the current slowdown, particularly with price pressures for key commodities flaring up again.

Rice, transport and power = the crucial three

Past episodes of high inflation in the Philippines have been driven in large part by supply-side issues. Local rice production is inadequate to meet domestic demand and so the country relies on imports of the grain from neighbouring economies. The Philippines also depends on imported energy for power generation and transport, highlighting how vulnerable the economy is to sharp fluctuations in global energy prices.

We have identified three key items in the CPI basket, namely rice, electricity and transport, which combined account for 23.41% of the total. For the most recent inflation episode, the crucial three accounted for 41% of inflation for 2022, highlighting the importance of stabilising price movements for these key commodities.

Given their weight in the CPI basket and the country’s dependence on imports of rice and energy, any sharp upticks for the so-called “crucial 3” could spell a renewed flareup for Philippine inflation.

The 'crucial 3' for Philippine inflation: rice, transport and electricity

It’s not a meal without rice

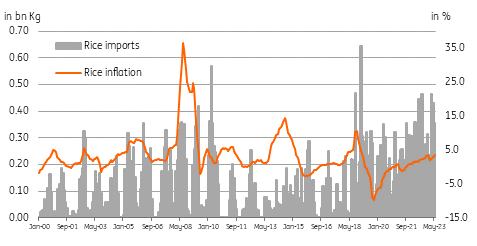

Rice is the main staple in the Philippines and meals are not considered a “full meal” without it. This fact is reflected in the 9.6% weight of rice in the CPI basket. Crop damage from storms or inclement weather has forced the Philippines to import more of the staple to shore up supply in the past. Developments in 2023 cloud the domestic production outlook with the onset of the El Niño weather phenomenon on top of the recent export ban from India.

Legislation passed in 2019 (RA 11203) removed quotas on rice importation, which in theory could help augment domestic supplies, however the Philippines could face elevated import costs given the impact of El Niño on rice exporters and the India rice export ban. Rice inflation recently moved past the target (4.2%YoY) and could increasingly become a concern should supply conditions tighten further in the coming months.

Philippines reliant on rice imports

Energy dependent

On top of being dependent on rice imports, the Philippines is also dependent on energy imports for power generation and transportation. Transport and electricity have substantial weights in the CPI basket, at 9.02 points and 4.8 points respectively. The spike in global energy prices in 2022 was one of the key drivers for inflation with transport and electricity registering inflation of 12.9%YoY and 18.5%YoY.

The recent resurgence in global energy prices due to developments in Ukraine and production cuts has resulted in higher Philippine domestic pump prices. This development should eventually filter through to higher electricity costs with 13.5% of power generation driven by oil-based power plants.

Furthermore, high inflation for transportation and electricity often results in second-round effects. Expensive transport and electricity costs could fuel an increase in prices for items that require transport and electricity in production, resulting in even more price pressures.

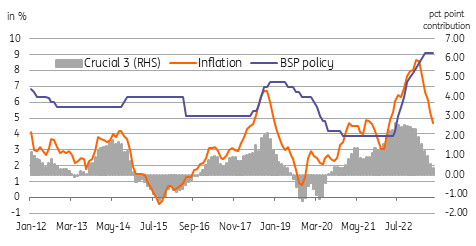

'Crucial 3' inflation spike to complicate BSP’s plan to ease?

BSP recently hinted at a potential policy reversal by the first quarter of 2024, pointing to forecasts where inflation would be well within target by that time.

The BSP is an inflation-targeting central bank with the goal of keeping inflation within the band of 2-4%. Recent tightening episodes were in 2014, 2018 and 2022 with BSP hiking rates to deal with price spikes induced by rising costs for rice and energy.

The recent uptick in rice prices coupled with the resurgence in global energy costs could spark renewed price pressures and prevent headline inflation from settling well within the BSP’s inflation target band. We had originally pencilled in a BSP rate cut by the first quarter of next year given the disappointing second-quarter GDP report. However, if we continue to see rice and energy prices tick higher in the coming months, we could see BSP delaying its planned easing to mid-2024.

BSP could delay rate cuts should inflation flare up again

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article