Rise in investment increases capital needs for utilities

- 12 January 2021

- Energy

A recovery in power demand of 3% on average for the European Union, coupled with a recovery in power prices, should bring European utilities back to growth in 2021

Across Europe, power demand fell 4.3% in 2020, according to ENTSO-E’s statistics. Depending on the severity of the Covid-19 pandemic and lockdown measures implemented by governments, some countries were more severely impacted than others. The consumption of natural gas also drastically slumped and its price on the markets reached all-time lows. A recovery in power demand of 3% on average for the European Union (according to Eurostat’s expectations) coupled with a recovery in power prices should bring European utilities back to growth.

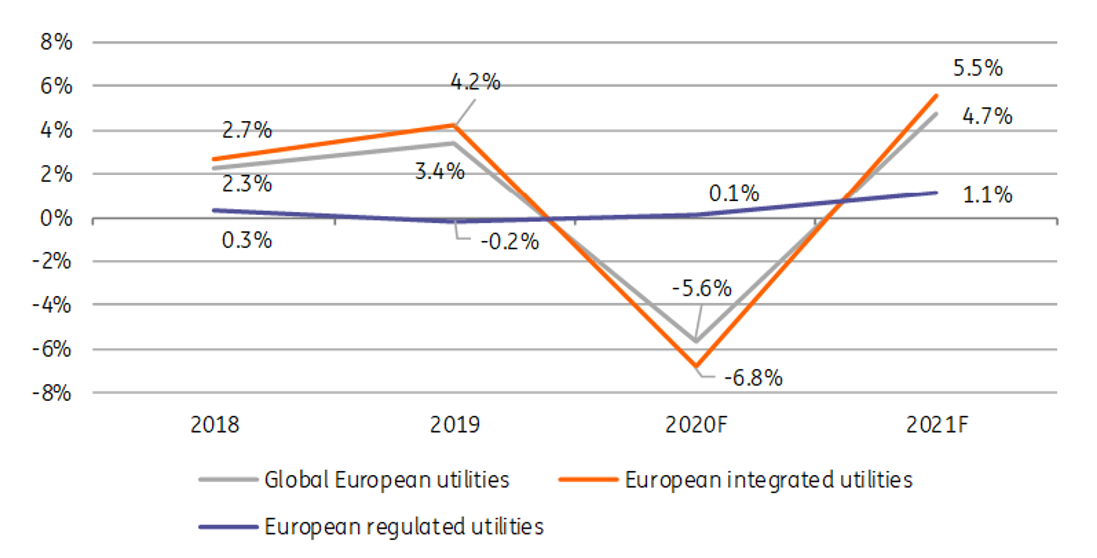

On aggregate, based on a panel of 38 utilities*, we estimate that European utilities’ EBITDA will be 5.6% lower in 2020 vs. 2019. While regulated utilities’ EBITDA should come in flat (+0.1% in 2020 vs. 2019), integrated utilities bear most of the impact from the Covid-19 pandemic with an aggregate EBITDA down 6.8%, according to our estimates.

| 4.7% |

European utility sector’s EBITDA to grow by this amount on average in 2021 vs. 2020 |

European integrated and regulated utilities – sector EBITDA 2018-2021F

Earnings growth in 2021

While a number of grid utilities will see their remuneration reduced by (new) regulatory packages, their strong capital expenditure plans will preserve cash flow generation growth thanks to inflated regulated assets bases. In 2021, we expect European regulated utilities’ EBITDA to grow 1.1% vs. 2020. With power and gas prices as well as consumption up in 2021, integrated utilities should be able to catch-up with a sector EBITDA growth estimated at 5.5%, based on updated strategic plans and our assumptions. All in all, we estimate that the overall sector (integrated utilities and regulated) will grow earnings before interest, depreciation and amortisation by 4.7%. Although it will not erase completely the 5.6% reduction in 2020, we consider this number to be very supportive for the sector.

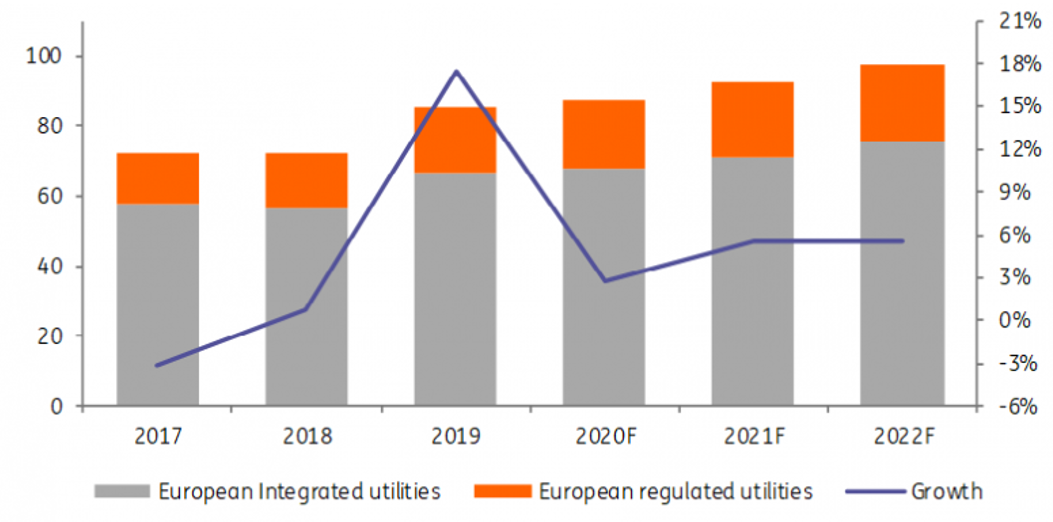

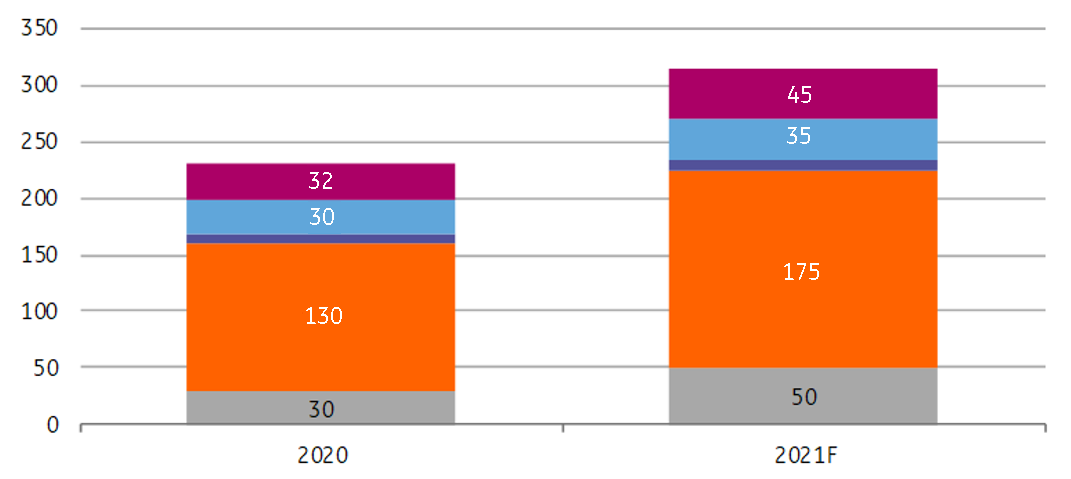

Contrary to oil & gas majors, European utilities are maintaining their ambitious capital expenditure plans. A number of utilities have even posted new strategic plans including bigger investments in 2021 and beyond, in comparison with their initial intentions last year and two years ago. Total investment in 2021 is expected to surpass 2020 by 5.5% with a strong focus once again on renewable capacity development and upgrade, as well as the expansion of power networks. We expect a similar expansion of investment in 2022, with growth of 5.6%, according to companies’ information and our estimates.

| 5.5% |

increase in investments in 2021 |

Total investment (€bn) and growth for the European sector (selection of 38 utilities)

Financing capex plans

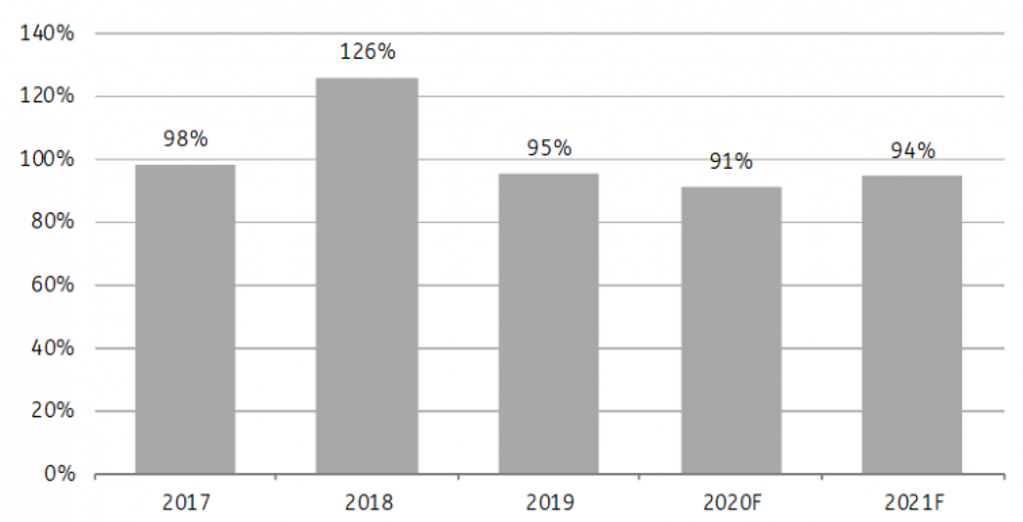

The expansion of capital expenditure, which started in 2019 and will go on in 2021 and beyond, suggests that cash flow generation (represented by cash flow from operations) will not be enough to fully finance investments. This is particularly true for regulated utilities, whose capital expenditure is expanding even more strongly than for integrated utilities. Taking our panel of 38 utilities altogether, we expect cash flow from operations to cover 94% of investment expenditures in 2021. Taking expected dividend payments into consideration, this ratio falls to 80%, according to our estimates.

Cash flow from operations/investment ratio

Bond issuance

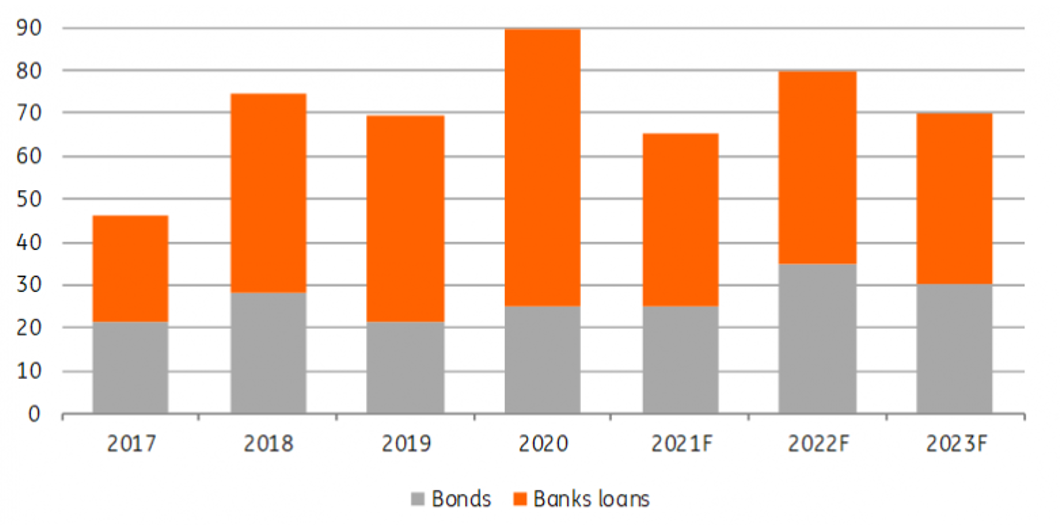

With cash flow generation too short to cover the capital expenditure in full, additional debt via bond or bank loan issuance, will translate into higher debt and pressure on credit ratios.

As far as the current debt burden is concerned, the utility sector has a relatively low bond and bank loan redemption schedule in 2021. While bond and bank loan redemptions reached almost €90bn in 2020, this number falls to €65bn in 2021. Total redemptions will step up again in 2022, reaching €80bn.

€ bonds and bank loans redemption schedule 2017-2023 (in €bn)

With ambitious capital expenditure plans and dividends payouts not fully covered by cash flow generation, we expect utilities to be printing c.€40bn of bonds this year. The Utility sector will continue to support global green bond issuance. Among all the corporate sectors (excluding Financials), utilities have been the most active in green bonds in the last few years due to the sector’s major role in energy transition plans.

In 2020, the markets, all currencies included, issued an equivalent of c.€380bn of sustainable bonds including green, social, sustainability and SDG-linked bonds. As far as euro-denominated bonds are concerned, some €230bn of bonds equal to or above €250m were printed in 2020. We forecast total euro-denominated sustainability bonds to reach €315bn in 2021.

2020 and 2021F € denominated bond sustainable issuance (in €bn)

| 20bn |

€ denominated green bonds in 2021 for the utility sector |

While we believe sovereigns and agencies will continue to dominate green, social and sustainable bond issuance in 2021, we expect the corporate sectors (excluding financials) to issue €45bn, with utilities accounting for €20bn of green bonds. Among the €45bn, we also expect more SDG-linked bonds (€12bn in 2021 against €3.1bn in 2020) as the format becomes more popular. A number of European oil & gas majors and utilities announced they were contemplating the issuance of SDG-linked (Sustainable Development Goals) bonds in 2021 that would allow the companies to target specific sustainability goals.

*38 utilities: A2A, Acea, Alliander, Centrica, CEZ, EDF, EDP, Elia Belgium, Enagas, EnBW, Enel, Enexis, Engie, E.ON/Innogy, Eurogrid, Fluvius, Fortum, Hera, Iberdrola, Italgas, National Grid, Naturgy, Nederlandse Gasunie, Orsted, Red Electrica, REN, RTE, RWE, Snam, SSE, Stedin, Suez, TenneT, Terna, Vattenfall, Veolia, Viergas.

This article is part of our Energy Outlook 2021. You can read the full report here.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

More power, flower

- This bundle contains 10 Articles