Riksbank’s hedging figures fuel FX intervention suspicions

- 20 October 2023

- FX

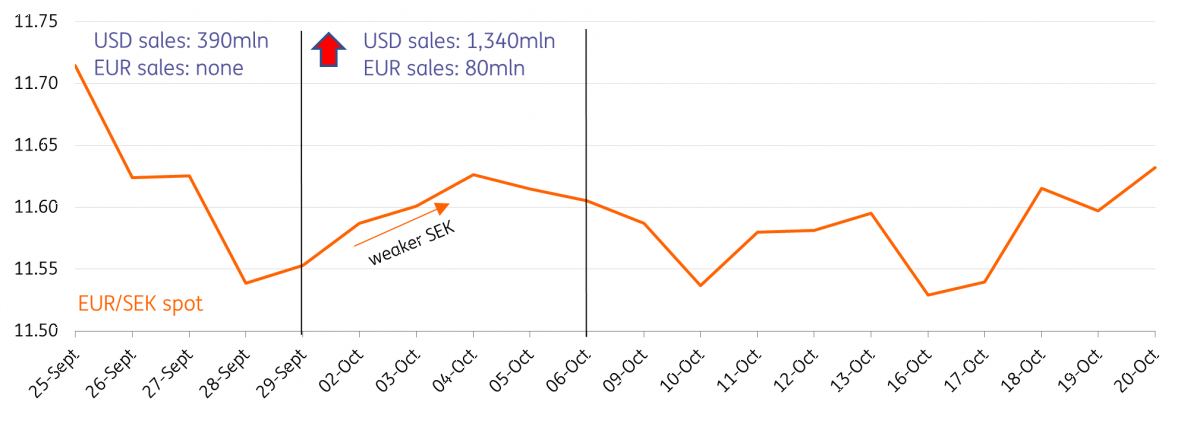

The Riksbank announced it sold a bulky USD 1.34bn in the second week of hedging operations (2-6 October). We suspect the high number was due to market pressure on the krona that week, which suggests the Riksbank is actively building a SEK floor. But with almost a fourth of the USD firepower already used, these covert interventions don’t look very sustainable

USD sales jumped in second week of hedging

The Riksbank released information for the second week (2-6 October) of FX reserve hedging operations this morning. Here are the main highlights of the report:

USD sales soared in the second week, from 390mn to 1.34bn

EUR sales were initiated, although at a rather moderate weekly pace: 80mn

Remember that the Riksbank announced it would hedge USD8bn and EUR2bn of its reserves over 4-6 months starting 25 September 2023. We discussed potential patterns and FX implications of the Riksbank’s hedging programme in our article “Sweden: Estimating the FX impact of the Riksbank’s hedging operations”. For reference, this table summarises our estimations for equally-weighted FX sales in three scenarios (four, five and six months), calculated before the Riksbank started publishing hedging data.

Our original estimates for Riksbank's FX sales

Looking more and more like FX intervention…

As shown above, we had estimated that the fastest (4 months) the Riksbank could sell its USD reserves on a weekly basis was USD520mn if it were not adjusting sales based on SEK levels (i.e. buying more SEK when SEK is cheaper). Today’s figures show that the Riksbank sold more than twice that USD amount (1.34bn) in a week, confirming our expectations that selling at a predictable pace was not in the plans. It’s true that sales were lower than expected in the first week, but the first two weeks saw sales totalled USD1.73bn, which is almost a fourth of the total stock of USD reserves (8bn) they plan to hedge.

We had thought the Riksbank would have concealed the “FX intervention” aspect of its hedging operations with a risk management rationale: buying more SEK when SEK its cheaper intuitevely maximises the return. However, that reasoning would have implied larger FX sales in the first week, when SEK was much cheaper. Instead, it definitely feels like that the second week’s huge sales were aimed at countering a drop in the krona that occurred between 2 and 4 October, as shown in the chart below. These manoeuvres look like covert FX intervention.

EUR/SEK and Riksbank FX sales

... but this isn’t necessarily good for SEK

Intraday price data show that EUR/SEK was rejected twice around the 11.65 resistance area since FX hedging started. Once on 4 October and on 19 October. Given how much Riksbank’s FX sales jumped around that 4 October EUR/SEK rally, we are inclined to believe 11.65 is one of the “pain levels” for the Riksbank if indeed it is carrying out covert FX intervention operations.

One question may arise: why are we looking at EUR/SEK when almost all FX sales were done on USD/SEK? That’s because the Riksbank would likely be targeting a trade-weighted index for SEK. In the Riksbank’s SEK effective exchange rate index, the EUR has a 46% weight, the USD only 8%. Sweden’s reserves were however 61% in dollars and 21% in euros as of April, hence the disproportionate amount of USD hedging.

The speculation that the Riksbank is actively seeking a floor for SEK may be read as a positive factor for SEK at face value. However, with almost a fourth of USD reserves ammunition (under the hedging programme) depleted by the second week, there is a tangible risk that speculators will start to doubt the ability of the Riksbank to effectively counter further selling pressure on SEK. While it’s true that EUR sales were minimal in the first two weeks, we must remember that some of the EUR sales will be conducted via the exchange of EU payments, and may have a smaller FX impact compared to the direct swap operations carried out in the USD/SEK.

Once again, don’t count on Riksbank’s hedging for a SEK turnaround

Today’s FX sales figures endorse our longstanding view that the Riksbank FX operations are unlikely to be a sustainable driver for a krona recovery. While the aggressive SEK buying during a week of SEK underperformance signals a potential intention by the Riksbank to cap EUR/SEK upside via covert FX intervention, our doubts about the limited firepower when it comes to FX hedging operations have grown even bigger.

One possibility is that the Riksbank increases the scope of its FX hedging operations (perhaps doubling it) if it senses that SEK requires more support and it’s running out of sellable reserves under the original hedging programme. That would be a rather aggressive move and de-facto admission of FX intervention.

For now, we continue to think that SEK requires an improvement in risk sentiment and a decisive turn lower in the dollar (thanks to weaker US data) to enter an appreciating path and start to sustainably converge towards its much higher medium-term fair value. Until that happens, the Riksbank can keep EUR/SEK capped at 11.65-11.70 via hedging operations, although it may have to accept higher levels, especially if geopolitical tensions put additional pressures on high-beta currencies.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more