Riksbank set for at least one more hike despite fragile economic backdrop

- 7 September 2023

- Sweden

Further declines in economic output are likely, but for now, the Riksbank is focused on high services inflation and renewed krona weakness

Riksbank set for at least one more hike

There are two weeks to go until the Riksbank’s September meeting and another 25bp rate hike looks pretty likely. Services inflation is uncomfortably high and the trade-weighted value of the krona is back to its lows. A follow-up rate hike in November can’t be ruled out.

Yet the economy is clearly reacting to higher interest rates. A 0.8% decline in second quarter GDP, while not as bad as initially reported, shows the economy is under strain. On a year-on-year basis, Sweden is in the bottom five performers in the EU when it comes to growth.

Still, the story isn’t universally bad and there are some bright spots. The jobs market is still very tight by historical standards, the housing market has stabilised, confidence is rebounding and consumer spending is showing signs of levelling out.

Here, we look at how the economy is performing in several key areas.

Housing market

Housing is a well-known vulnerability for Sweden, and the 16% peak-to-trough fall in prices during 2022 was not hugely surprising. Compared to other European economies, Sweden has a much greater percentage of variable rate mortgages, and that proportion has only increased since interest rates started to rise. According to the Riksbank, 90% of loans have a remaining fixation period of below two years, and in the majority of cases, these are not fixed at all. The result is that the average rate on outstanding mortgages has increased by 200bp since the Covid low, compared to 64bp for the eurozone as a whole, and much less still in France/Germany.

How average mortgage rates have changed since 2021

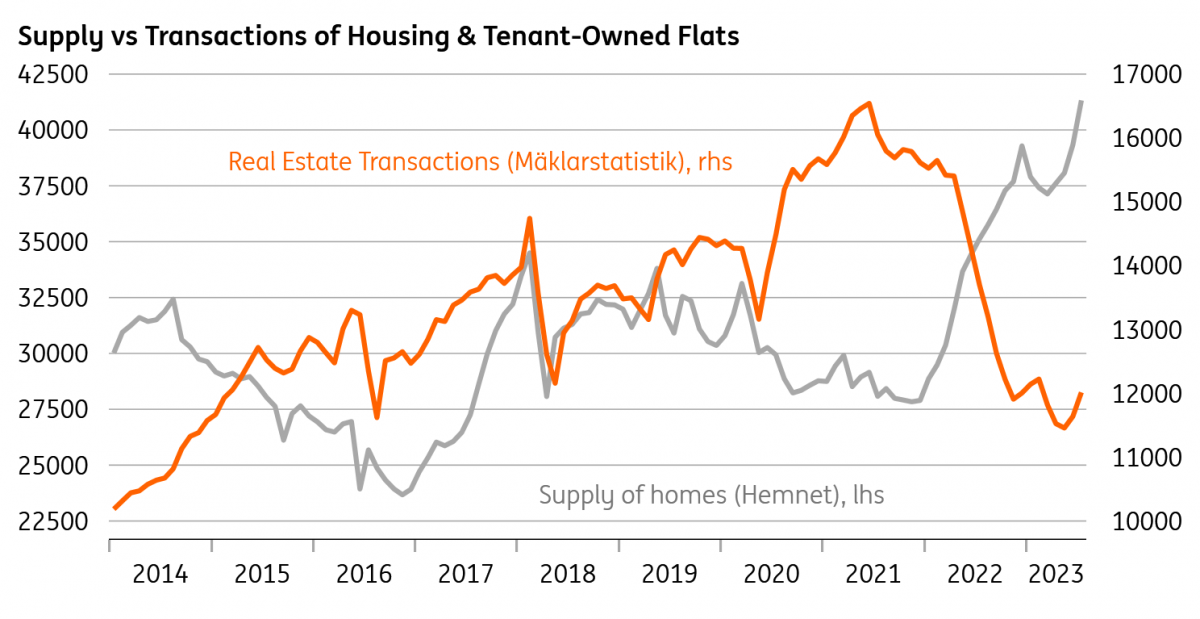

That said, housing prices have stabilised this year and household sentiment towards housing has improved noticeably. But the fundamentals of the market still look challenging, and data from Hemnet – a property search site – shows housing supply at multi-year highs, while separate figures show transactions are at a low. We tend to agree with the Riksbank’s forecast that further price falls are likely.

Supply of housing has increased as transaction volumes fall

Jobs market

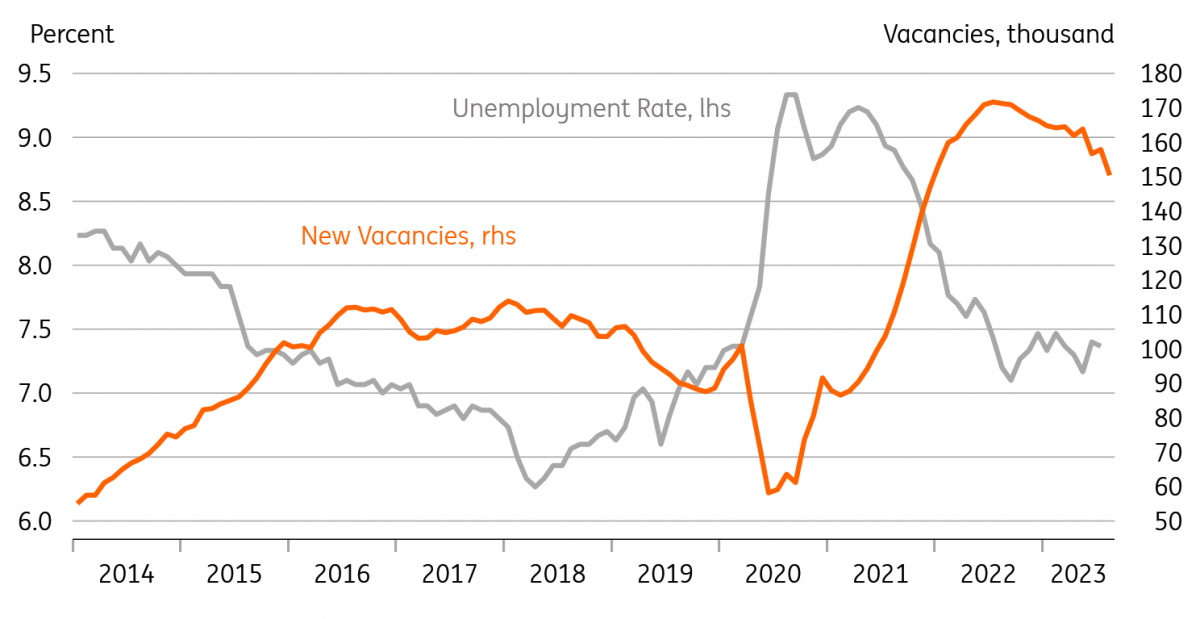

Sweden’s unemployment rate is at a post-pandemic low, and that resilience has been helped by a pronounced reduction in joblessness among foreign-born workers. One of the key issues for a number of years has been a skills mismatch and poor integration of migrant workers into the Swedish jobs market – and the gulf between native unemployment (below 5%) and foreign-born workers (near 14%) is still large, but has narrowed.

There are signs that the jobs market is cooling, however. The number of layoffs has started to rise, though from a low base. Vacancy numbers have been falling too, though so far the decline in the ratio of job openings to unemployment has been less sharp than in other economies, notably the US and UK. The proportion of service-sector businesses that see labour as a constraint on production has fallen from 45% to 30% in just over a year.

Still, there are signs that firms are “hoarding” staff – i.e. they are afraid of letting people go given rehiring concerns. This is helped by the fact that nominal wage growth is relatively contained given the level of inflation, with the benchmark negotiated pay deal set at 3-4% for the next couple of years. That's noticeably below the rate we've been seeing in some other advanced economies.

As a result, while we’re assuming that unemployment will increase over the coming months, the rise is likely to be gradual.

Vacancy numbers are falling, albeit slowly

Consumer spending

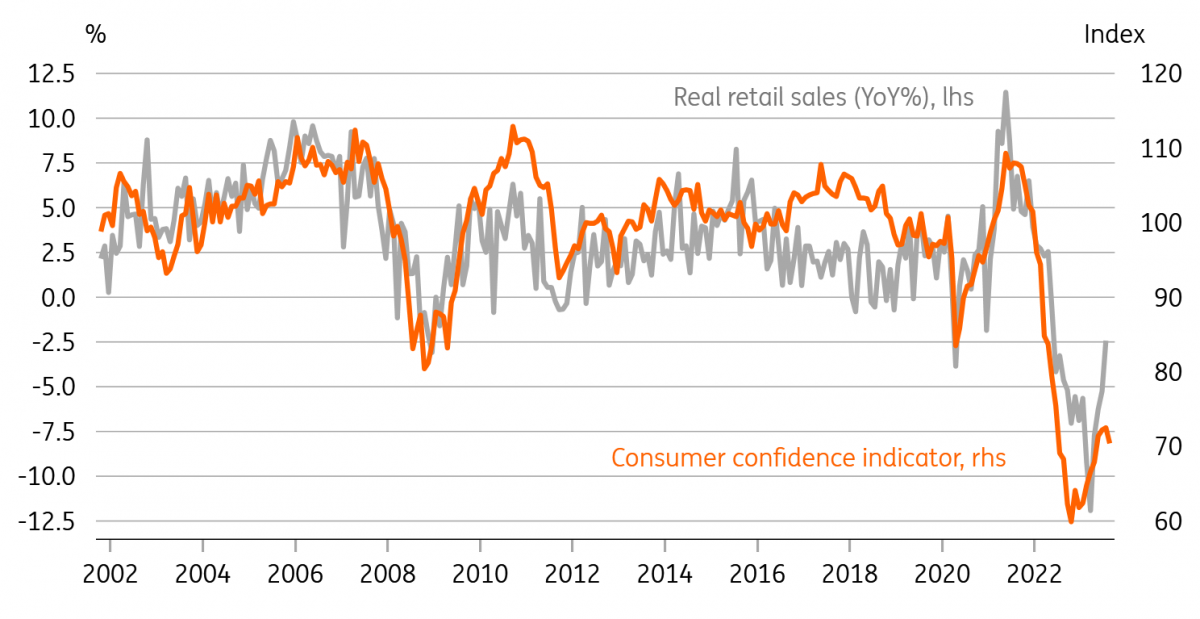

Consumption has been falling consistently for a year now, though this masks big differences across spending categories. Furniture sales are down 15% on pre-pandemic levels while spending on recreation/culture is up by a similar percentage. Even in the weaker areas though, the story is stabilising. Consumer confidence has risen noticeably, and real wage growth is slowly becoming less negative. Still, with interest payments set to consume an ever-increasing share of household budgets, we don’t expect consumer spending to return to meaningful growth any time soon.

Higher consumer confidence points to stabilisation in retail sales

Production

Like consumer spending, and like pretty much everywhere, Sweden’s manufacturing sector is also in contraction, at least according to the PMIs. Admittedly, this weakness hasn’t entirely been borne out in the official production data, and Swedish manufacturing has been operating 5-10% above pre-pandemic levels for much of the last year – in sharp contrast to the likes of France/Germany where production remains below early-2020 levels.

This growth has been heavily concentrated though, primarily in chemicals/pharmaceutical products, and more recently in a sharp recovery in vehicle production. The latter is up almost a third since the start of 2022 on improved supply chains, but we suspect this is more of a catch-up story and can only last for so long. We expect the weaker manufacturing numbers to show up more clearly in the official data over the coming months.

Bottom line

Assuming there's a renewed fall in house prices, some gradual weakness in the jobs market and ongoing pressure on consumer spending and production, we're likely to see further declines in economic output through the remainder of this year. While the Riksbank clearly isn't quite done with rate hikes, the fragile economic backdrop suggests we're near the peak.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Swedish economic and FX update: Pessimism reality check

- This bundle contains 2 Articles