Riksbank preview: Resisting the ECB’s dovish lure

- 1 July 2019

- Sweden

This year’s bout of krona weakness and potential for further depreciation suggests the Riksbank won’t be too fazed by the prospect of ECB easing. Policymakers are likely to signal that a further rate hike is possible in the next 12 months, although we think this is unlikely to materialise

The next Riksbank meeting will take place on 3 July at 9:30am CET

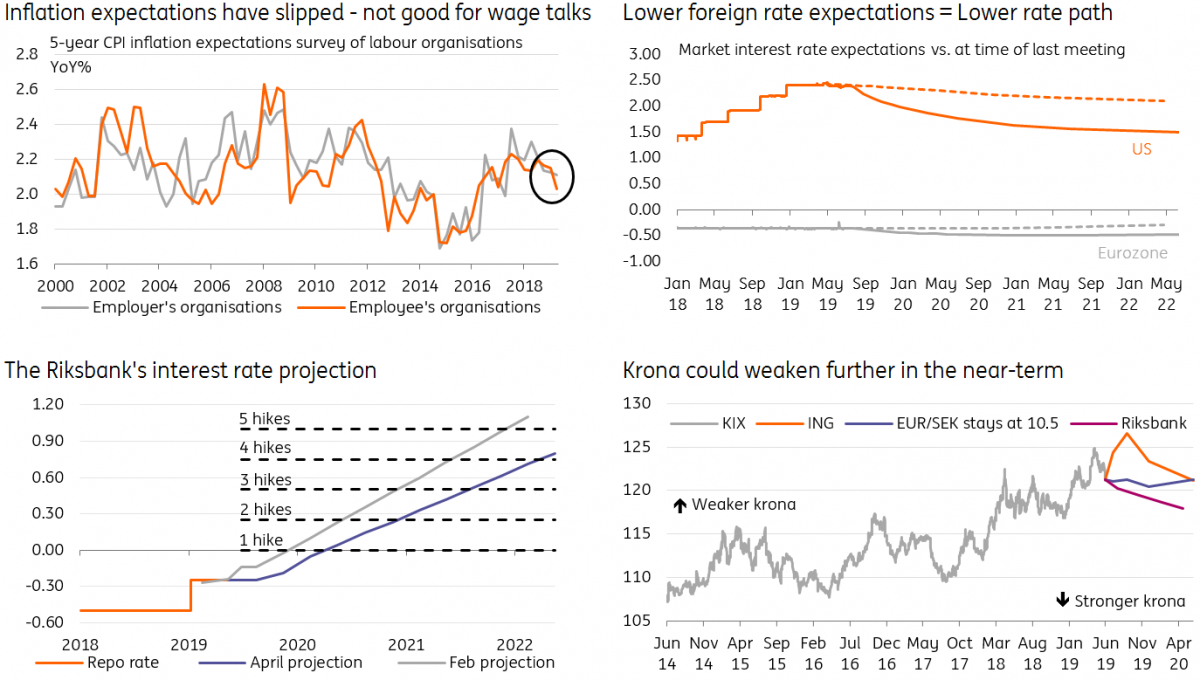

Riksbank likely to be fairly relaxed about ECB easing prospects

In times gone by, Swedish policymakers have closely mirrored ECB moves, including the shift to negative interest rates. But this time, things look slightly different. The krona has weakened further since the start of the year, and with EUR/SEK above 10.50, policymakers appear to be taking a more relaxed stance when it comes to potential currency strength.

A few meetings back, the Riksbank ditched a previously long-standing reference to keeping SEK at a level “compatible” with its inflation target. Recent inflation reports have also factored in some krona appreciation over coming years, on the belief that the currency is undervalued.

All of this suggests that the Riksbank will opt against ‘meeting fire with fire’ if faced with some currency strength on the back of a more dovish ECB. In fact, our FX team think the krona is actually more likely to depreciate further against the euro, as increasing concerns surrounding global growth outweigh the impact of ECB easing (which is largely priced).

We could see a slightly lower interest rate projection

That’s not to say the impact of ECB/Fed dovishness won’t have any effect. The fact that market expectations for the Fed and ECB have slipped should translate into a lower Riksbank interest rate projection – assuming policymakers keep their SEK forecasts broadly unchanged.

That could see a subtle shift in the timing of the next hike – currently projected to come either later this year or early next. However, we’d still expect the Riksbank to hint at another move by next summer, given that away from interest rate expectations, there are unlikely to be wholesale changes to the forecasts previously set out in April. The last two inflation readings, for instance, came in more-or-less exactly as the Riksbank projected at its last meeting.

A 2020 rate hike may not materialise

In reality though, we think this future tightening is unlikely to materialise – or at least not as soon as the central bank is currently projecting. Domestic demand is likely to remain fairly lacklustre, despite a slightly more solid spring housing market performance. The lagged impact of earlier property price declines is still translating into slower residential construction, while the fragility of the market is also weighing on consumer sentiment.

There are also some tentative signs that inflation expectations are slipping among labour organisations (that represent both employers and employees). Admittedly the change is relatively minor so far, but it comes as another reason why the next round of wage negotiations in the spring may not yield the kind of agreement the Riksbank is currently forecasting. The central bank is expecting wage growth to go from 2.6% in 2018 to 3% in 2020.

The potential for a further deterioration in global trade relations could also spell bad news for Sweden’s relatively open economy. In the context of possible US auto tariffs later this year, it’s worth highlighting that car exports make up 7.5% of the total, and the US is the biggest customer.

Wrapping all of that together, we expect the Riksbank to keep the repo rate where it is for the foreseeable future.

FX impact: The krona’s ongoing unattractiveness

We see the recent SEK strength as temporary and driven by positioning (late May) and the turnaround in risk appetite (late June). In our view, the bearish case for SEK remains fully in place.

The domestic economy remains weak (as house price declines weigh on consumption and investment) and with inflation excluding energy below the 2% target, there is a very limited case for Riksbank hikes – we don’t expect any more hikes during this cycle. As we said above, the bar for the Riksbank to surprise on the hawkish side and provide some support to SEK this week is set rather high.

This means that the unattractiveness of a low-yielding, high beta SEK remains in place. The currency suffers in the bad times (as do other higher beta FX), while in the good times it does not overly benefit given that it doesn’t offer yield (instead it tends to be seen as a funding currency). The krona has also lost the support from the trade balance surplus. We think there's a high risk of EUR/SEK hitting 11.00 this summer, as the likely escalation of trade wars is a negative for the currency of an open economy like Sweden.

The Riksbank's July dashboard

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more