Riksbank preview: On hold as May cut speculation intensifies

Sweden’s central bank is looking at a more encouraging inflation outlook but may be relatively cautious in revising its rate projections lower. In our view, a cut in June is likely – but risks of a krona drop, resilient services inflation and an improved economic outlook mean May cut bets may be overdone. Still, prompting a hawkish repricing won’t be easy

Data encouraging dovish bets

A surprise move by the Swiss National Bank has fired the starting gun on the rate cutting cycle among the G10 major central banks – and there is a chance that the Riksbank might be next. While Sweden’s central bank is set to keep rates at 4% when it meets on 27 March and releases its latest projections, the recent dataflow has raised the prospect of a cut at the May meeting.

Perhaps the most important development is that Swedish inflation has improved faster than both the consensus and the Riksbank had expected. Headline CPIF came in at 2.5% in February and core (excluding energy) at 3.5%. The Riksbank had been expecting 2.9% and 3.7% respectively, though it’s worth noting that this downside surprise is driven by goods rather than services. Services inflation is actually running around half a percentage point above the Riksbank’s forecast, and it’s this that most of the major central banks are focusing more heavily on right now.

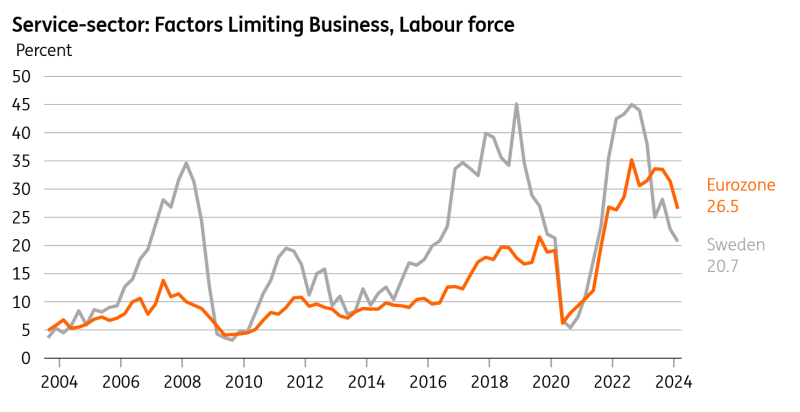

Still, there should be better news here in the pipeline. The jobs market is cooling more rapidly than elsewhere. The unemployment rate is up, and surveys show that fewer firms are experiencing worker shortages in Sweden than in the eurozone, which is historically unusual. There are also more unemployed workers than job vacancies for the first time since late 2021. Together with lower survey measures of inflation expectations, this points to reduced wage pressures further ahead.

Labour constraints are easing in Sweden

All of these elements – coupled with consistent Swedish underperformance on economic activity and less significant currency pressure – enabled the Riksbank to pivot towards a more dovish narrative back in February. The statement saw policymakers acknowledge that “the possibility of the policy rate being cut during the first half of the year cannot be ruled out”. That, together with the surprise inflation figures, has allowed markets to speculate more freely on earlier rate cuts.

Markets are calculating that these downside surprises on inflation are set to continue and the implied probability of a May cut has jumped to 50-60%, with a June cut almost fully priced in.

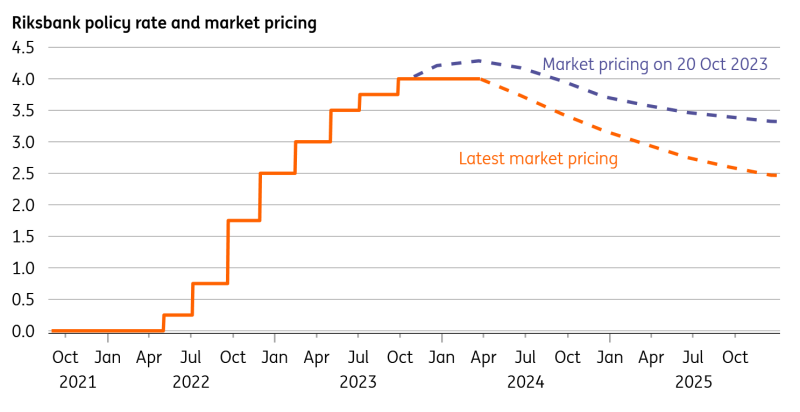

Market rate expectations have moved lower

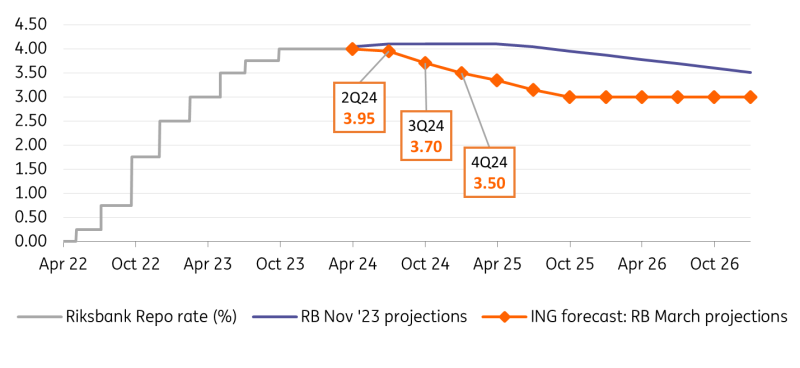

Rate projections to be revised lower – but not too aggressively

The latest projections (from November 2023) show that rates would be kept at 4.0% throughout 2024 and a large part of 2025. Those are now clearly outdated; the reference to cuts in the first half of the year in recent communication, paired with lower-than-expected inflation, means that the rate path will likely be revised lower.

Despite growing speculation of a May rate cut, we think the Riksbank will be careful to not sound too dovish. This means not signalling more than one cut in the first half of 2024, therefore implying that the first move will be in June and not May. In our view, the projections may be even more conservative than that, showing only a fraction of a cut by mid-year, and slightly over 50bp in total for the year.

Our expectations for new rate projections

Krona remains a primary concern

The Riksbank remains one of the most currency-focused developed central banks. In a recent comment, Deputy Governor Martin Floden reiterated how a weak krona – along with geopolitics – remains the biggest upside risk for inflation. This echoes previous remarks by Governor Erik Thedeen and others. The Bank should continue to exercise caution to avert material SEK depreciation.

Along with evidence that the domestic economic backdrop is generally stronger than at the November meeting, krona concerns are, in our view, the main reason why the Riksbank will avoid signalling aggressive easing in the rate projections, and instead hint that a cut in the first half of the year is not a done deal.

The Riksbank measure of the trade weighted krona is not much changed since the November and February meeting, but SEK is the worst performing currency in G10 since the start of March. While external factors (mostly US related) remain undoubtedly the primary driver of SEK, recent underperformance against close peers like NOK is a reflection of rising bets on a Riksbank May cut. That is a strong enough incentive for policymakers to avoid encouraging dovish bets.

Our call on the Riksbank and the krona

We don't think it will be easy for the Riksbank to prompt a hawkish repricing of May cut expectations. The Bank’s rate projections have been very cautious when it comes to easing before, and markets have not really taken them as a reference as they increasingly priced in more cuts. Unless Governor Thedeen pushes back explicitly against a move in May, we think markets will continue to price a moderate probability of a May cut while waiting for new data inputs.

With a lot of easing already in the price, the downside risks aren’t too big for the krona at this meeting. Still, the market reaction will also be influenced by the new inflation forecasts. There is a risk that downward revisions in CPIF will encourage dovish bets despite a relatively conservative rate projection.

Our call on the Riksbank remains unchanged. It appears too risky to move in May given concerns on the krona impact and resilient services inflation. We expect the Riksbank to wait for the European Central Bank to move first in early June (this is our economists’ call) and deliver the first 25bp cut on 27 June. We see 75bp worth of cuts in both Sweden and the eurozone by year-end.

The Riksbank policy should not matter as much as Fed easing for the krona. Our view is that the Fed will cut 125bp this year starting in June, and that a decline in USD rates and the dollar will boost high-beta currencies like SEK. In the near term, SEK might face a bit more pressure, but our expectation is that, in the next couple of months, we will see enough US data weakness to kickstart the USD downtrend and SEK rally. We currently target 10.70 by year-end in EUR/SEK.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article