Riksbank: Don’t rule out a hike this week amid hawkish pivot

- 26 April 2022

- Sweden

In stark contrast to its February forecasts, Sweden's Riksbank could hike rates as soon as this week. More likely though, policymakers will lay the groundwork for a June hike and several more thereafter. The Riksbank should continue to be a broadly supportive factor for SEK in the coming months

Riksbank set to lay the groundwork for a June rate hike

Sweden’s Riksbank has long sat at the dovish end of the central bank spectrum, and only in February was it formally projecting no change in the repo rate before 2024.

Fast forward a few weeks and the story couldn’t be more different. Admittedly those rate projections were never likely to survive for long, and indeed in our last forecast update at the start of the month we brought forward our forecast for the first rate hike to September.

But since then, several board members have floated the possibility of much earlier rate rises. That includes Governor Stefan Ingves who, when asked, offered very little pushback against the 10 rate hikes that are roughly priced into financial markets over the next couple of years. A rate hike this week certainly shouldn’t be ruled out, though we suspect policymakers will be more inclined to lay the groundwork for an increase in June.

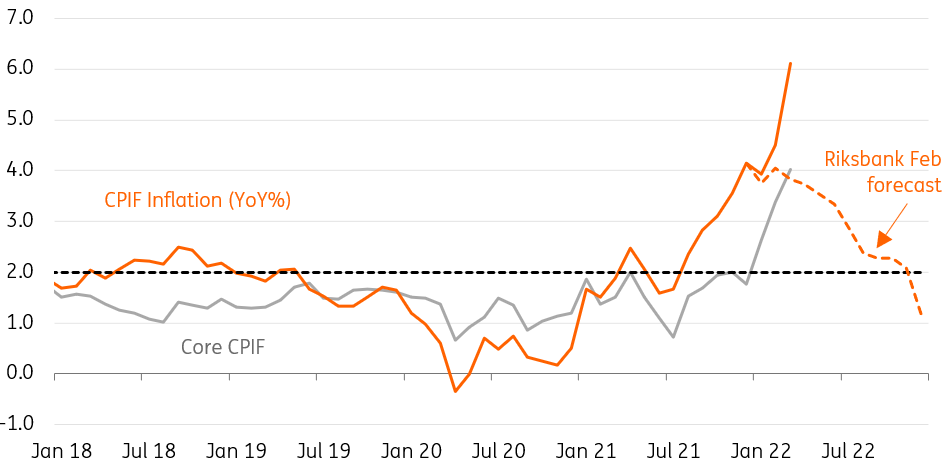

Swedish inflation has come in much higher than the Riksbank's forecasts

It’s not hard to find the source of the recent hawkish turn. Headline CPIF inflation came in above 6% in March, well ahead of the 3.8% Riksbank forecast from February. Big updates to the projections are inevitable.

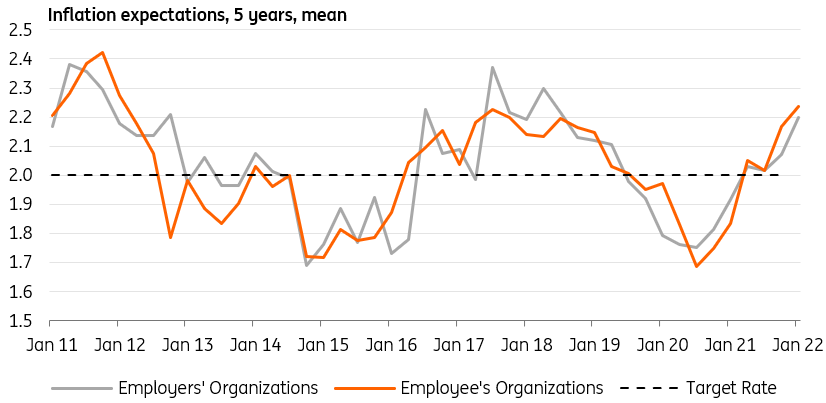

This is important in the context of wage negotiations, which occur on a three-year cycle, and are due to conclude next spring. Higher headline inflation rates mean there's a growing chance that these talks will result in a higher outcome than during the 2020 round. The jobs market is tight, and labour shortages are as acute as they were in 2018 when the unemployment rate last troughed. Inflation expectations among employer and employee organisations are increasing too.

In short, we expect the Riksbank to endorse a rate hike each quarter this year, starting in June. We doubt the new interest rate projection will go as far as markets, which are pricing a terminal rate in the region of 2.5%. But we wouldn’t be surprised to see the Riksbank pencilling in at least another 2-3 hikes in 2023 and 2024. All of this is likely to be coupled with a reduction in the size of the balance sheet, most likely starting in the third quarter (2Q purchases have already been announced).

Inflation expectations among wage negotiators have been rising

FX: More support to the krona, but watch for external risks

The radical shift in the Riksbank’s rhetoric and the market’s increasingly hawkish repricing of rate expectations in Sweden have combined to offer some meaningful support to the krona, with EUR/SEK now trading around pre-Ukraine-war levels. That surely implied some reduction in the geopolitical risk premium embedded into European assets.

This week’s policy decision can continue to offer support to the krona. Naturally, a rate hike this Thursday would likely see SEK rally, but we also think that a hawkish shift in the rate projections and some endorsement of the market’s tightening expectations (which have been always significantly ahead of the curve) can be enough to put some mild pressure on EUR/SEK. We think only a clear pushback against market pricing would have a material negative impact on SEK.

In our view, the Riksbank should continue to be a broadly supportive factor for SEK in the coming months. However, the external environment should continue to prove quite challenging for the krona, which may suffer from its high beta to both a) global risk sentiment – at a time where global tightening cycles (as well a prolonged Ukraine conflict) can hit risk appetite and b) eurozone’s economic outlook – which should start to show the negative impact of high energy prices and the war in Ukraine.

These factors mean, in our view, that EUR/SEK risks are by and large balanced for Q2, and we expect it to hover around the 10.40 mark into the summer months. Later in the year, some stabilisation in sentiment and the Riksbank’s advantage over the ECB in the tightening cycle can push EUR/SEK to the 10.20-10.00 area.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more