China: We’re cutting our GDP forecast as deleveraging bites

- 14 June 2018

China's credit tightening is hitting economic activity and we are cutting our 2Q GDP forecast as a result. But don't panic. We don't think this weakness will last very long and we're not expecting a credit crunch

Revising GDP growth downward to 6.7% YoY from 6.8% in 2Q18

We are revising our China GDP growth forecast to 6.7% YoY from 6.8% YoY in 2Q18 but maintain our forecasts for 3Q18 and 4Q18 at 6.7% YoY. The revised GDP forecast for 2018 is 6.70% from 6.75%.

Weaker economic activity could be a result of credit tightening

Economic activity was slower than expected in May.

- Industrial production fell to 6.8% year on year in May from 7.0% YoY in April

- Retail sales grew 8.5% YoY from 9.4% in April

- Fixed asset investments have fallen to 6.1% YoY year to date from 7.0%

We have found that credit tightening has had a big impact on economic growth.

Slower retail sales growth as consumers wait for tariff cut to be reflected in prices

Slower growth in retail sales has been broad-based, with the exception of telecommunication items and petroleum and related products. Even automobile sales posted a negative 1% YoY growth rate. The slower growth has been caused by:

- A high base, as retail sales growth has been strong for many years.

- Tariff cuts, which have encouraged consumers to wait for prices of imported goods to come down. This applies to automobile sales and daily consumer products. Sellers of goods imported before the tariff cuts may need to lower their prices to attract consumers, so we may see a revival of retail sales in June.

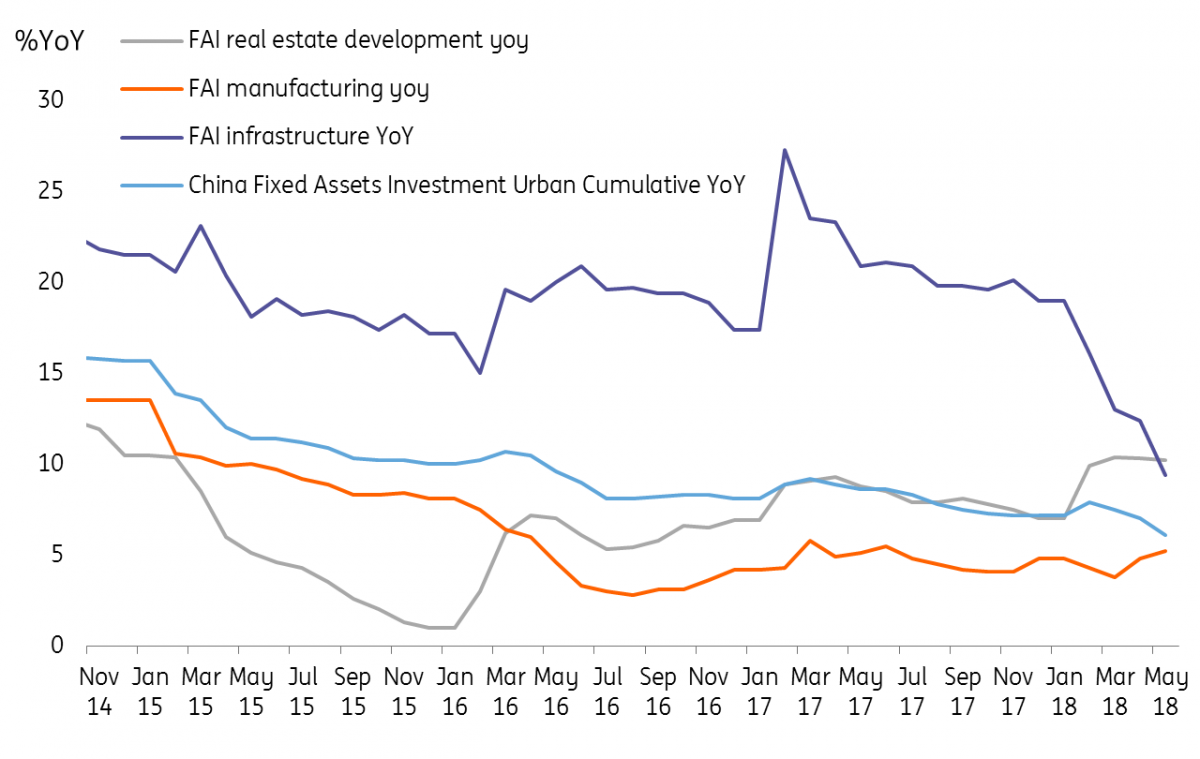

Fixed asset investment shows only in manufacturing

A slowdown in fixed-asset investment growth has also been broad-based but in varying degrees for different industries.

Investment in transportation fell 2.3% YoY YTD, of which investment in rail transport was down 11.4%. This is a direct result of financial deleveraging reform that has tightened issuance of wealth management products, of which the underlying assets are usually local government-supported infrastructure projects.

High-tech investments and manufacturing should be able to pick up. Fiscal and monetary support for high-tech and SMEs will offset the loss of economic growth from credit tightening.

Still, investment in computer telecommunications manufacturing still held up well at 14.6% YoY YTD. This allows us to retain our bullish stance for 2H18, as we expect more fiscal support in this area.

In addition, real estate development didn't slow as quickly as the headline number. Real estate development grew 10.2% YoY YTD, down just slightly from 10.3% YoY YTD. The central government's gradual approach to deflating the property bubble has indirectly cushioned overall investments.

Trade tensions have had some impact on investment, reflected by a fall in spending by Hong Kong-owned and foreign-owned enterprises. These enterprises focus more on export markets and could delay investment decisions as trade tensions escalate around the world.

Industrial production still has high-tech support

Unlike retail sales, slower growth in industrial production was not broad-based.

Most of the high-tech items continued to grow at a solid rate. For example, industrial robots grew at 35.1% YoY in May up from 33.7% in April, and integrated circuits grew 17.2% YoY compared to previous month's 14.6%.

It seems to us that industrial production in areas related to Made in China 2025 is still holding up well. This implies the current credit tightening from financial deleveraging reform has not hit the high-tech sector.

Financial deleveraging reform will continue to pressure the economy

Credit tightening has led to a rising number of defaults in China and has resulted in weaker economic activity. But growth momentum is not going to return simply by the central bank halting a five basis point rate hike. We think there will be more fiscal support to boost investment in high-tech sectors, as well as monetary support for SMEs ( more on PBoC's monetary policy here) and we don't expect the weakness in May to last long.

With financial deleveraging reform continuing throughout 2018, we don't expect there will be a sudden return of high growth in fixed asset investments in sectors related to transport infrastructure, and that is the reason behind our revised 2Q18 GDP forecast.

But we don't see China facing a credit crunch

We are not expecting a credit or liquidity crisis as a result of tighter credit because:

- Credit measures and liquidity are controlled by the central bank. The central government and the central bank can be flexible in crafting policies to avoid the economy weakening continuously.

- The impact of financial deleveraging on wealth management products (and therefore the underlying assets) should be reflected in around three months' time. The new measures were announced at the end of April, so most of the impact should be seen from May to July.

As financial deleveraging reduces the unnecessary financing of projects, it should also reduce the number of projects by local governments. This would keep investment growth in transport infrastructure at a low level.

In the meantime, high-tech investment and manufacturing pick up.

As a result, we are still optimistic on growth in the second half of this year and expect fiscal and monetary support to offset the loss of economic growth from credit tightening.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In Case You Missed It: Confidence and cracks

- This bundle contains 7 Articles