Asia week ahead: Relatively light data calendar with scattered trade and production data

- 3 March 2022

- Asia week ahead

Next week's data calendar features China's policy guidance and Korea's presidential elections

China releases policy guidance

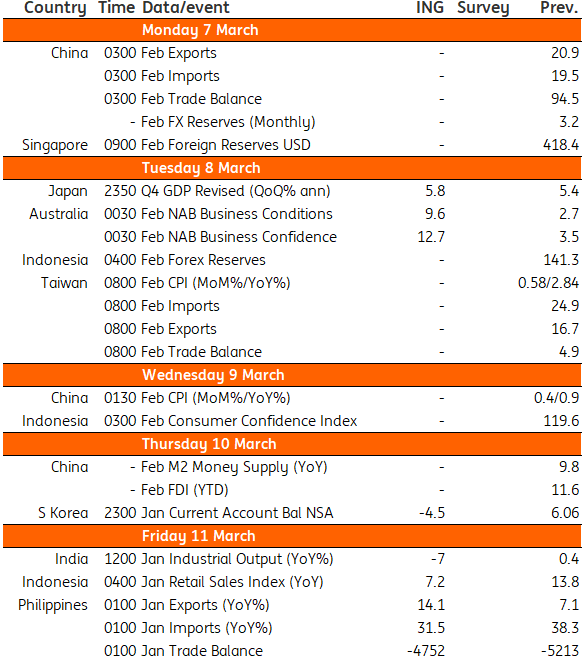

China’s annual Two Sessions (National People's Congress and Chinese People's Political Consultative Conference meetings) will take centre stage next week. The government work report is being released this Saturday (5 March), which will announce policies for the economy for 2022 ahead of the 20th Party Congress in the fourth quarter of this year. These policies will likely be geared towards the main theme of stability, which implies more pro-growth policies to offset the damage from the continued deleveraging reform on the real estate sector.

There are also many Chinese data points scheduled for release next week. We expect export and import data to reflect resilient growth on a year-on-year basis. Meanwhile, retail sales, fixed asset investments and industrial production should show a divergence in Chinese growth, with retail sales being the laggard within the economy. Loans should continue to increase robustly, although likely to a smaller extent than January – which is the usual pattern.

Trade data out in the Philippines

We expect recent trends for Philippine trade to hold with imports sustaining strong double-digit gains as the economy continues to gradually reopen. Elevated crude oil prices should also bloat the energy import bill, keeping the trade gap wider than US$4bn. Exports on the other hand will post a decent gain on robust electronic component exports but will not likely keep up with the pace of expansion for inbound shipments. In the coming months, the trade gap should remain wide suggesting a sustained depreciation bias for the peso.

Impending Indian production data

India’s January industrial production numbers will be out next week, which should reflect more of what the PMI data gave us an early glimpse of. The Omicron wave sent Covid case counts surging in January, peaking at levels (about 350,000 daily cases) only slightly lower than the second wave. With this came the unsurprising reimplementation of some movement restrictions, which were only wound back recently in India’s capital. Daily Covid cases are now averaging just slightly over 10,000, boding well for the resumption of more normal activity with vaccination rates now above 70%.

Australia’s business sentiment indicators should paint a positive outlook

After GDP growth figures released on Wednesday showed a sharp rebound for 4Q21 (actual: 3.4%, ING: 1.9%), February business confidence and conditions data will be released in Australia early next week. These should reflect continued improvement in business sentiment, as movement restrictions have been further reduced and states reopen their borders.

Korea may see a new president

The Korean presidential elections will take place next Wednesday (9 March). The respective candidates from the ruling party (Mr. Lee Jae-myung) and the major opposition party (Mr. Yoon Seok-yeol) have been running neck-and-neck in the polls, with around 40% support each. The latest polls have suggested Yoon is in the lead, but all remain within the statistical margin of error.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles