Refined products: Middle distillate tightness to persist

- 7 September 2023

- Commodities, Food & Agri Energy

Refinery margins have been volatile in recent months due to tight inventories and a number of outages over the summer. We expect margins to remain volatile and relatively elevated given the tightness in middle distillates, along with the lack of new refining capacity

Volatile and elevated refinery margins likely to remain

Refined product markets witnessed significant strength over the northern hemisphere summer, which helped to drive refinery margins to their highest levels since last year. Strength was seen across the board, although it has predominantly been middle distillates which have pushed margins higher.

More recently, however, margins have started to give back a lot of these gains. Weakness has been largely driven by gasoline as we come to the end of the summer driving season. Middle distillates have also come under some renewed pressure more recently. The latest release of Chinese export quotas would likely have put some pressure on cracks.

Longer-term, refined product markets remain vulnerable. Inventories are mostly tight and global refining capacity has remained largely unchanged since 2019, with new capacity offset by longer-term closures. This is happening at a time when demand continues to grow, leaving markets tight. While there is spare capacity in China, the ability for significantly more refined products to make it onto the world market is restricted by export quotas. This suggests that refinery margins are likely to remain relatively elevated and volatile for the foreseeable future.

China releases further export quotas

A delay in the release of the third batch of refined product export quota from the Chinese government initially provided some support to refined product markets. Uncertainty over when we would finally see this released and the volume of the third tranche were supportive. Recently, the government finally issued the third batch, which amounted to 12 million tonnes, more than the 10 million tonnes the market was expecting. This also means that export quotas released to date total 39.99 million tonnes, above the 37.25 million issued over the whole of 2022. The increase in refinery run rates this year has allowed for a higher quota allocation.

However, what is not clear is whether the government will release a fourth batch of export quotas. Much will likely depend on how domestic demand evolves over the remainder of the year. Even if we see further releases, it does not guarantee that further quotas will have to be used before the end of the year. As we saw last year, the government may allow some of these to be rolled over into early next year.

Higher export quotas have obviously translated into higher export volumes of refined products. Over the first seven months of the year, refined product exports totalled 36.62 million tonnes, up 46% year-on-year. Diesel exports have seen the largest increase with 8.4 million tonnes exported, compared to just 2.4 million over the same period last year.

China refined product export quota releases exceed 2022 levels (m tonnes)

Middle distillates to remain well supported

Like last year, the middle distillate market has led the strength amongst refined products. The ICE gasoil crack has traded as high as $45/bbl recently, with the NYMEX heating oil crack hitting highs of more than $50/bbl while Singapore gasoil cracks briefly traded a little over $35/bbl in August.

Declining middle distillate inventories have helped to push the market higher, with stocks well below the five-year average in most regions including the US, ARA in Europe and Singapore. The concern is that inventories have been falling and are already low as we head into the northern hemisphere winter, a period where you would expect to see stronger demand. This suggests that middle distillate cracks are likely to be fairly well supported.

In Europe, a key issue has been the ability of buyers to replace Russian products. Prior to the EU ban on Russian refined products, Russian gasoil flows to the EU were about 450Mbbls/d. In the lead-up to the ban, there was some front-loading, evident in the buildup of inventory over the latter part of 2022 and into early 2023. Since the ban, the EU has turned to other origins, however, it would appear that this is not enough to fully make up for the loss of Russian supply. As a result, we have seen ARA gasoil inventories steadily declining since late February.

Recovering air travel has also played an important role in the renewed strength seen in middle distillates. This is evident in the widening of jet fuel’s premium to gasoil in north-west Europe, whilst the Asian regrade discount continues to narrow. This shouldn’t be too surprising given that air traffic continues to move towards more normal levels. The latest data from the International Air Transport Association show that air passenger traffic (revenue passenger kilometres) in July was 4.4% below the same period in 2019. In fact, in North America and Latin America, passenger traffic is back above 2019 levels. However, Asia is still lagging with passenger traffic 8.8% below 2019 levels. While we could see a seasonal slowdown in jet demand with the end of the northern hemisphere summer holidays, we should continue to see a recovery year-on-year, driven predominantly by Asia.

In addition, ongoing OPEC+ supply cuts have led to distortions in the crude oil market, which has fed through to the product markets. These cuts have led to a tightening in the medium sour crude market, which will have an impact on refinery yields, with refiners yielding lighter products as a result.

A tightening in gasoil has also attracted speculators to the market or at least has seen a drastic shift in their positioning. This is evident when looking at speculative positioning in ICE gasoil. The managed money position has increased from a net short of almost 33k lots in early May to a net long of almost 94k lots by mid-August – 127k lots of buying, which is close to 95m barrels of buying.

Our view is that middle distillate cracks should remain relatively well supported for the remainder of the year at around US$30/bbl, whilst through 2024 we expect the crack to average a little over US$20/bbl.

Gasoline cracks to ease

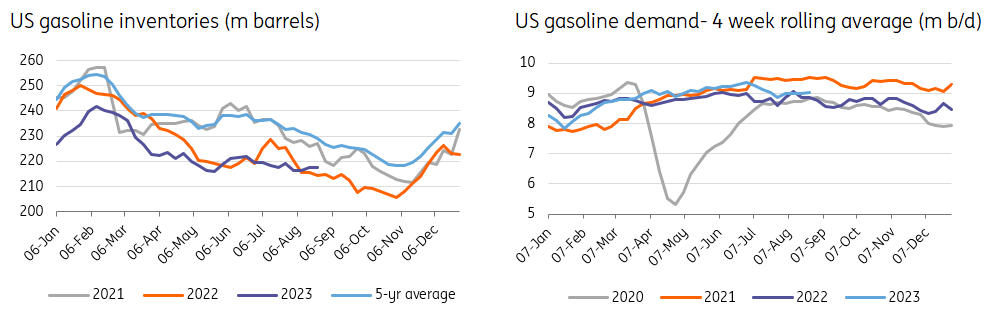

The gasoline market has been strong for much of the summer, trading to levels seen last summer – a time when there was plenty of uncertainty over Russian crude and product flows. The strength in the market had been partly due to low US inventories, which have been well below the five-year average. In addition, there were a number of refinery outages over the summer, whilst hot weather in parts of Europe meant that refiners had to reduce run rates, which hit gasoline output.

US gasoline demand also held up well through much of the second quarter, with the four-week rolling average at levels last seen back in 2019. However, since early July, whilst demand has remained above year-ago levels, it has fallen below levels seen in 2021. Gasoline cracks have come under significant pressure more recently, coinciding with the end of the driving season.

Obviously, with the US driving season now behind us, demand is likely to continue to trend lower, which should mean we start to see US gasoline inventories moving higher, particularly once seasonal refinery maintenance is complete. However, much will depend on how the rest of the US hurricane season develops. Seasonally weaker demand, combined with refiners processing lighter grades of crude (due to tightness in the medium sour market), suggests that there is limited upside in gasoline cracks in the coming months.

Meanwhile, gasoline inventories in the ARA region are comfortable, remaining near five-year highs, suggesting that there will be little upward pressure on cracks driven by European dynamics.

US gasoline inventories to rise as demand edges lower

Hi-5 fuel oil spread likely to widen

The high-sulphur fuel oil (HSFO) market has seen significant strength this year. In fact, the HSFO crack traded at an unusual premium in north-west Europe briefly over the summer. A key driver in the strength of the HSFO market has been the tightness in the medium sour crude market, which as mentioned has come about due to ongoing OPEC+ supply cuts. The tightness in the sour market is reflected in the unusual discount of the Brent/Dubai spread.

In addition, the European market would have been supported by reduced Russian flows since the EU ban was implemented earlier in the year.

Over the summer months we would have also seen the usual stronger demand in the Middle East for cooling purposes. This demand should ease in the months ahead, which should support the view of weaker HSFO cracks. Already, we have started to see these cracks weakening from their recent highs. However, this weakness is likely to be somewhat limited given the tightness in the medium-sour crude market.

As for very-low sulphur fuel oil (VLSFO), we expect this market to be relatively well supported given the strength that we are seeing in middle distillates and the expectation that the middle distillate market should hold up relatively well through the coming months.

Therefore, given expectations of some weakness in HSFO and support for VLSFO we believe the Hi-5 (VLSFO-HSFO) spread will widen from current levels. It is also worth pointing out that we are not far off from levels where this spread has historically found some good support.

Naphtha cracks to stay deeply negative

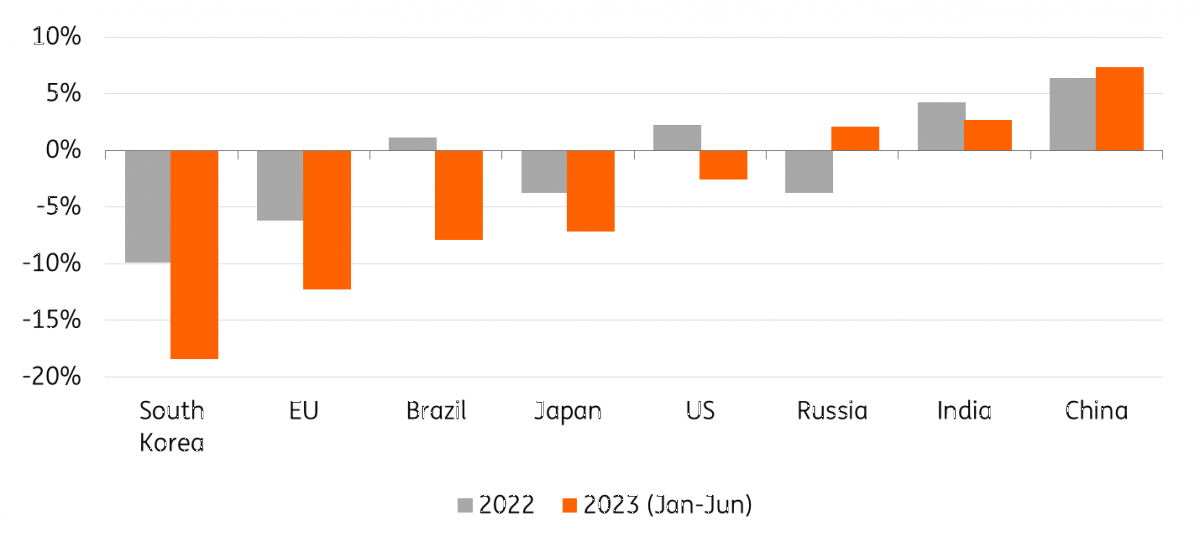

While the naphtha market has strengthened over the summer, prompt cracks still remain deeply in negative territory and well below historic norms. There are several reasons driving the broader weakness in the naphtha market. Firstly, a weak propane market has ensured that propane is the favoured feedstock for the petrochemical industry, with propane trading at more than a US$100/t discount to naphtha in northwest Europe. Secondly, downstream demand has been weaker, with cracker margins in both Asia and Europe not great.

In Europe, the chemical sector has suffered significantly because of higher costs and weaker demand. As a result, chemical production over the first half of 2023 was down 12.3% year-on-year according to the European Chemical Industry Council (Cefic). Cefic numbers show that this weaker output from the sector is not isolated to Europe. South Korea and Japan also saw large declines over the first half of 2023, with output falling by 18.4% and 7.2% YoY respectively.

Despite this, we expect naphtha cracks will see seasonal strength as we move into the northern hemisphere winter with increased usage amongst the petrochemical industry as propane’s discount to naphtha narrows, making propane a less attractive feedstock for the industry. However, whilst we see strength in cracks, we expect that they will remain firmly in negative territory and below historic norms through the northern hemisphere winter, given weak downstream demand.

Chemicals production still under pressure (YoY % change)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more