‘Ready-to-drink’ market growth puts pressure on aluminium cans

- 25 March 2021

- Commodities, Food & Agri Manufacturing, Construction and Retail

The 'ready-to drink' market has seen significant growth over the last few years driven by consumer demand for more convenience and healthier alternatives. But, the increased consumption of canned beverages has led to aluminium can shortages, as recognition grows that the metal is infinitely more recyclable and sustainable in comparison to PET plastic

It’s comforting to see there are some winners during these unprecedented times.

The ready-to-drink segment is the only category in the alcoholic beverage market that saw growth in 2020. In our view, this is partially due to Covid-19 but not entirely. Between 2014-2019, the global Total Beverage Alcohol (TBA) grew at a compound average growth rate of 5%, while the ready-to-drink segment grew at a rate of 8% over the same period.

Even before the pandemic, we think there were three main drivers. Convenience, on-the-go consumption and health & well-being. The single-serve nature of ready-to-drink beverages also raises the question about their impact on the environment.

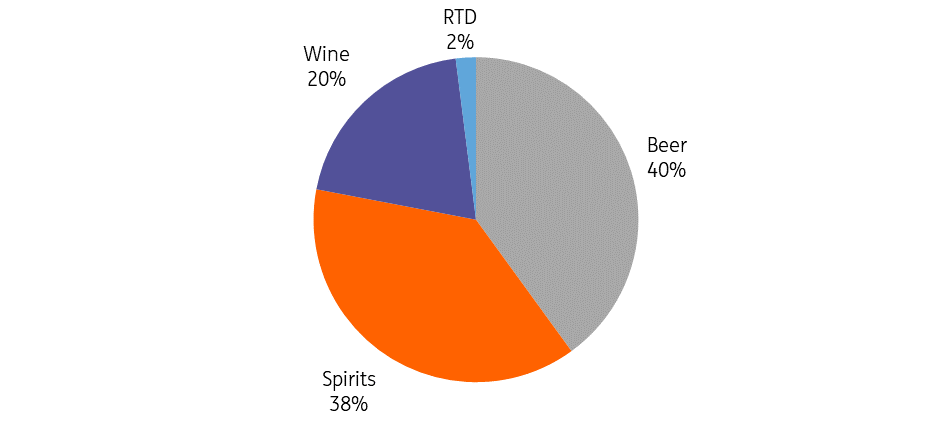

The figure below shows the market is still very small with only 2% of the total value.

Global Total Beverage Alcohol (2019)

Consumers want convenience

The single-serve packaging that is ready for consumption on purchase answers this question due to the versatile nature of ready-to-drink beverages.

Consumers love the convenience of having what they want, when they want it, without any compromise

For example, a pre-mixed, canned cocktail can be quickly and easily served without the hassle of a pantry with numerous ingredients. A ready-to-drink option also makes it easier to meet different flavour preferences. In other words, consumers prefer the convenience of having what they want, when they want it, without compromise.

We also see how the ready-to-drink market functions as a snack or a meal replacement for consumers on the go too.

Functional ready-to-drink beverages rising in popularity

Health & well-being is the second main driver behind the growth of the ready-to-drink market.

This trend was already gathering pace even before the pandemic, but in our view has accelerated, as consumers become ever more conscious of the benefits of a healthier lifestyle.

Functional ready-to-drink beverages are an alternative to carbonated soft drinks, with lower sugar content, natural flavours and ingredients to enhance performance, and so on. This is valid for both alcoholic and non-alcoholic drinks. Although alcohol consumption is hardly ‘healthy’, consumers looking for healthier alternatives to cut down alcohol and sugar intake can have some indulgence and a healthy lifestyle simultaneously.

Market expected to grow by 41%

Lastly, we believe the shift from at-home consumption to out-of-home consumption has only been temporarily reversed due to Covid-19 lockdown measures. And as we have seen, the ready-to-drink market was the only category to experience growth during 2020, and more growth is very likely.

According to the drinks industry analytics group IWSR, between 2019- 2024, the market is expected to grow by 41%.

More canned beverages mean more aluminium consumption

Another sie to the ready-to-drink market is that more canned beverages mean more aluminium consumption.

Even before the pandemic, there was plenty of tightness in the aluminium can market due to the strong demand growth, and Covid-19 has exacerbated the market imbalance, particularly from North America.

There has been a structural shift in beverage packaging materials due to the growing recognition that aluminium is infinitely recyclable

There are two primary drivers behind the strong aluminium can demand. Firstly, demand from the global beverage industry has seen strong growth even before the pandemic. Secondly, there has been a structural shift in beverage packaging materials due to the growing recognition that aluminium is infinitely recyclable and a more sustainable packaging alternative compared to glass and PET plastic.

One scenario is that the shortage in the aluminium can market may morph into a more secular one if beverage makers stepped up to slash their carbon footprints, as they face rising environmental, social and governance pressure. As such, they may seek to boost their use of either recycled aluminium or virgin aluminium but with a low carbon identity.

The trend in sourcing aluminium with lower carbon footprints is not unique to the packaging industry. Other industries, such as the consumer goods and transportation industry, face similar ESG pressure.

Aluminium supply breakdown versus consumption from major regions (2018)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Night boat to Cairo

- This bundle contains 10 Articles