RBNZ preview: A closer call than markets expect

- Yesterday, 12:00

- New Zealand

In our view, there are enough arguments to hike at this 27 May meeting (an underpriced risk), but the Reserve Bank of New Zealand has erred on the dovish side and looks more likely to opt for a hawkish hold. New projections may show tightening already in 3Q, and we expect the first of two hikes in July. NZD moves should stay mostly externally driven though

A hold is more likely, but the risk of a surprise hike is underpriced

That is the main reason why, despite the worsened energy price story, markets are pricing close to zero (5bp) probability of a hike at the 27 May meeting, and consensus is unanimously calling for a hold at 2.25%. This is also our call, but we think markets are underestimating the chances of a surprise hike. If the April statement is taken at face value, raising rates as early as May would not be such an aberration (we explain why below). Some members had already argued in favour of an “early monetary policy response” in April.

In any case, a hike in July is looking increasingly likely in our view, and should not be a one-and-done. Our current forecast is for 50bp of tightening in 2026, though this is highly dependent on energy market dynamics. Swap market pricing is 21bp for July and 75bp by year-end, and we suspect RBNZ communication at this meeting will seek to preserve this hawkish pricing.

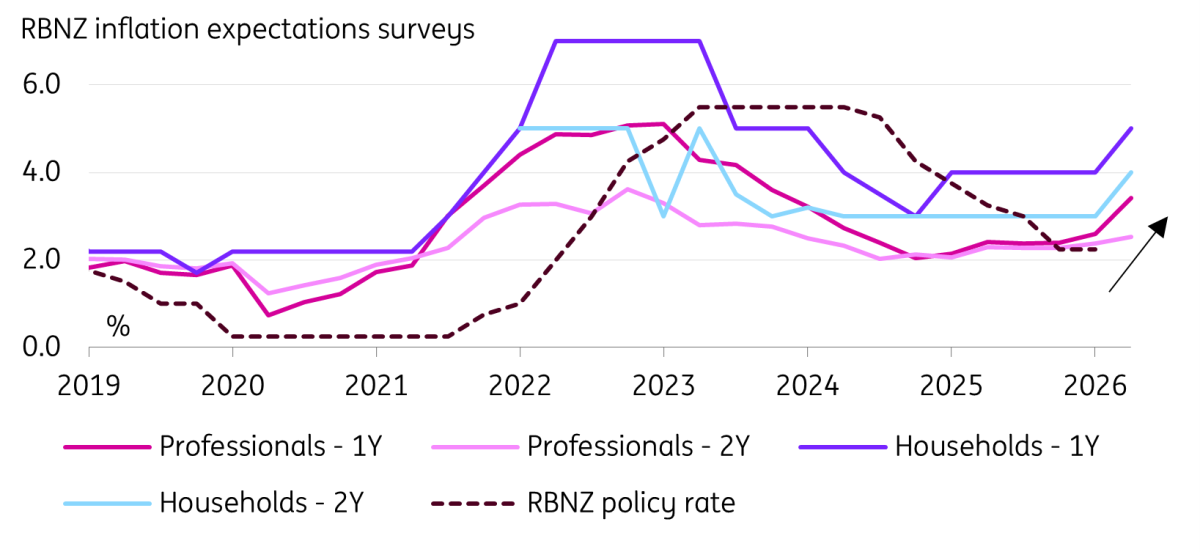

Inflation expectations on the rise

Our argument for hiking already at this meeting hinges on inflation expectations, which featured prominently in the April statement. The RBNZ was explicit about the conditions that would warrant “decisive and timely increases in the OCR”: inflation and wage growth need to remain contained, and medium to long-term inflation expectations must stay anchored around 2%.

While inflation and labour market data arrive with a lag and are released only quarterly in New Zealand, inflation expectations are already flashing warning signs.

Publishes two inflation expectations surveys: one covering forecasters, economists and industry leaders, and another covering households. The former, released on 13 May and more closely monitored by markets, showed a sharp rise in one-year inflation expectations, up 0.82pp QoQ to 3.41%, with two-year expectations also edging higher by 0.16pp to 2.53%. The household survey is noisier and typically overstates CPI inflation, but the signal is similar: one-year expectations rose from 4.0% to 5.0% in Q2, and the two-year measure from 3.0% to 4.0%.

Inflation expectations are on the rise

These surveys must obviously be assessed alongside labour market conditions. First-quarter figures show unemployment declined slightly to 5.3%. That is well above the 3-3.5% levels that preceded the inflation surge, but not far from the 4.8% five-year pre-pandemic average.

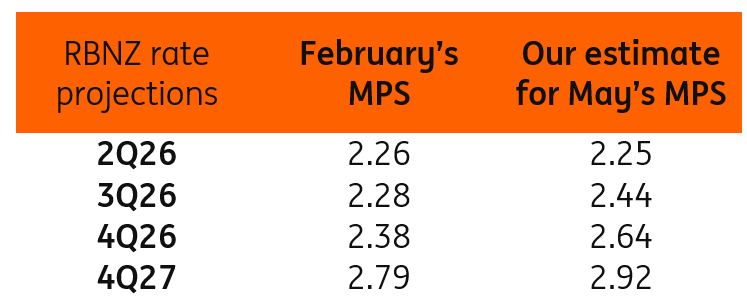

Expect a hawkish revision of projections

We think markets are underestimating (5bp priced in) the chance of a surprise hike at this May meeting, but our base case is a hold next week. Governor Anna Breman has a dovish reputation from her Riksbank years. Policymakers may still want to await more clarity on Middle East developments and inflation dynamics.

However, there is a tangible risk of losing control of inflation expectations before the summer, and we believe the RBNZ has an incentive to keep market pricing as hawkish as it is now (75bp by year-end). We expect it to do that by clearly opening the way for rate hikes in the statement and revising up its rate projections in the Monetary Policy Statement (MPS).

Our best guess (see table below) is that the projections will show one full hike, with an implied probability above 50% of a second move by year-end. Other economic projections will also matter. Consensus has moved towards Q2 CPI at around 4.0-4.5%, with inflation not falling below 3.5% until at least year-end.

Our estimates for new rate projections

Our new RBNZ call

Developments in the Middle East will remain the key driver of RBNZ policy. For now, we pencil in a 25bp hike in July, followed by another in September or October, and then a prolonged pause.

Relative to this baseline, risks are skewed to the hawkish side, either via a surprise move already at the May meeting, as discussed, or through three to four hikes over the coming quarters.

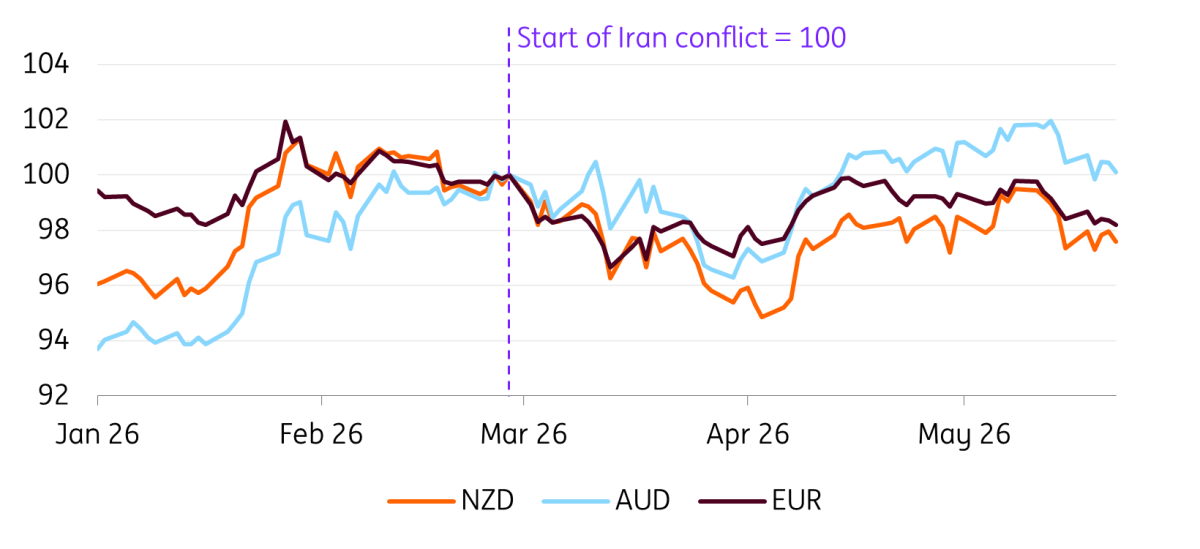

NZD remains mostly externally driven

The Kiwi dollar has had a less negative May than most other G10 currencies, as European FX has absorbed most of the impact from deteriorating Middle East sentiment. Even so, NZD remains the second-worst performer after SEK since the start of the war, reflecting in part the RBNZ’s cautious-dovish stance.

If our expectations for revised rate projections are confirmed, markets would receive an implicit green light to keep pricing around three hikes by year-end. Even in a scenario of Middle East de-escalation, there would be limited incentive to push pricing much below two hikes.

This backdrop is supportive for NZD, given the market's tendency to reward currencies backed by proactive tightening by central banks. However, the near-term outlook remains dominated by Middle East headlines, global risk sentiment and US rate expectations.

Beyond the short term, our call for NZD/USD to return above 0.60 in 2H26 continues to rest on a relatively benign resolution in the Gulf, alongside our expectations for two RBNZ hikes and one Fed cut by year-end.

NZD has been a laggard

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more