RBNZ emulating the SNB? The risk could be an antipodean currency war

It's remote but the Reserve Bank of New Zealand might be looking at a Swiss-style mix of negative rates and FX intervention in future if economic conditions worsen. However, market intervention would likely imply significant purchases of the Aussie dollar, and a possible adverse reaction by Australia's central bank may not be worth the risk

The RBNZ has started to hint at intervention

The RBNZ is dealing with the adverse impact of a relatively strong currency, and has so far failed to effectively curb the New Zealand dollar's gains through its threat of more rate cuts. In our article “Can the RBNZ really curb the Kiwi $?” we discuss how the Bank may not succeed in curbing the NZD's appreciation unless it effectively delivers on its threat to jump into negative rates.

The latest RBNZ policy statement mentioned the purchase of foreign assets as a possible monetary tool deployable alongside negative rates. Such a policy mix highly resembles the one currently used by the Swiss National Bank. The most obvious difference, however, is that the RBNZ is currently making use of a large quantitative easing programme (the SNB is not) to provide stimulus to the pandemic-hit economy.

The RBNZ statement claims that the choice to deploy more stimulus will depend on “the outlook for inflation and employment”. Inflation slowed from 2.5% in the first quarter to 1.5% in the second, while the unemployment rate has remained at 4% in 2Q (surprisingly inching lower) largely thanks to government subsidies and a rise in underutilisation. We may need to see inflation staying in the lower half of the 1-2% band in the second half of the year and the unemployment rate moving above 5% to prompt another round of RBNZ stimulus.

It's important to remember that third quarter data will be published at the end of October and the first few days on November, and so a move by the RBNZ might have to wait until the 11 November policy meeting.

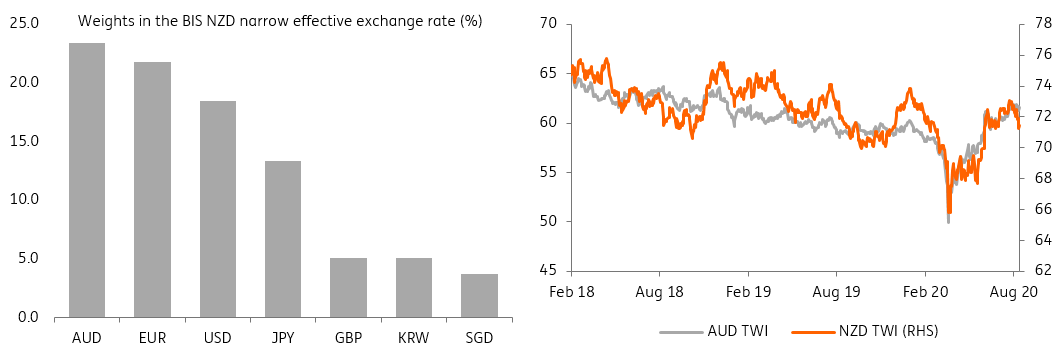

Intervention could mean heavy AUD buying

The BIS provides the weights of its widely-used effective exchange rates (or trade-weighted indices) for each currency, which can be used as a framework for which currencies a central bank would most need to buy in order to put downside pressure on the domestic currency. In the case of the Swiss franc, the euro carries a weighting of 61.5% in the total narrow effective exchange rate, and the SNB intervenes by buying EUR for CHF to limit the appreciation of the franc. The best demonstration of the euro’s relevance to the SNB is the choice of EUR/CHF as the currency floor in 2011.

In the case of New Zealand, there isn’t a similarly high portion of the exchange rate which is attributable to only one currency. The chart below shows how the currency with the biggest weight in the BIS narrow NZD effective exchange rate is the Aussie dollar (23.4%) followed by the EUR (21.8%) and the USD (18.5%). The sum of all those currencies make up the share of EUR in the CHF effective exchange rate.

In order to effectively drive down the value of the Kiwi dollar, the RBNZ may need to purchase a good share of Aussie dollars.

The RBA may not like it

The implications of such move would obviously go beyond the simple monetary policy perspective. While the RBA has shown a (surprisingly) relaxed stance towards the recent strength of its currency, the AUD is unarguably a key shock absorber for the Australian economy as NZD is for New Zealand. Should the RBNZ really start to purchase Australian dollars to weaken the trade-weighted NZD, the question is how the RBA would respond.

It is worth noting that the weight of NZD in the AUD TWI is minimal (less than 5% according to BIS narrow indices), so the impact on the AUD would hardly be significant. With this in mind, the RBA could either ignore the intervention of the RBNZ, even if AUD is purchased, or simply emulate the RBNZ and intervene itself in the FX market, but by purchasing USD and EUR (the two main contributors to its effective exchange rate) and not NZD.

The risk, however, would be of a more political nature, as the RBA may not tolerate the RBNZ’s purchase of its currency, which is already facing excessive buying pressure amid a fragile global economy. An antipodean “currency war” is something the RBNZ would like to avoid in the first place, considering the NZ economy is far more dependent on Australia than vice versa.

AUD/NZD would likely benefit from it

A move towards a mix of negative rates and FX intervention is not our base case for the RBNZ, and a considerable worsening in NZ economic conditions would likely be needed to trigger such an extreme policy reaction. Our analysis aims to highlight how a hypothetical emulation of the SNB's policy mix would be complicated for the RBNZ given the more dispersed nature of the NZD effective rate, which does not show a currency with such a dominant weight like the EUR for CHF.

Incidentally, the RBNZ would need to purchase the Aussie dollar to effectively drive down the NZD value but the risk of triggering an adverse reaction by the RBA and a possible currency war (or political implications in general) may outweigh the benefits of a weaker currency.

While the dovish RBNZ tone has not been enough to truly dampen the NZD so far, steps towards the ultra-dovish policy mix described above would hardly leave NZD at its current levels. AUD/NZD may be a key beneficiary in such a scenario, as NZD/USD may remain partly supported by USD weakness, while the loss of NZD attractiveness on the back of the RBNZ policy would leave asymmetrical interest in favour of AUD to play reflationary trades, especially in the sphere of proxy investments on the Chinese economic recovery. Still, much would, inevitably, depend on the RBA reaction, as highlighted above.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article