Rates: where to now?

- 14 August 2020

- Rates

The move higher and steeper in global rates should extend further in the near term, up to 0.90% in 10Y US Treasuries. We see it as mainly technical and not supported by fundamentals but supply pressure continues to be felt

Ground zero: US Treasury supply pressure

The week came and went and with it the adjustment higher and steeper in the USD yield curve driven mostly by supply as we expected. Given that we withheld our judgment about the prospect for another leg higher in USD rates until after the result of yesterday’s 30Y auction, we owe you a tactical rates direction update.

The auction itself was poor. Besides the lower bid to cover ratio and discount compared to secondary market levels, weak price action around the sale speaks to the soft demand. The signal about the US Treasury market’s ability to absorb large amounts of duration is not encouraging, especially as the Treasury has another $25bn 20Y auction lined up next week.

Truth be told, we tend to be dismissive of the macroeconomic drivers behind the adjustment higher in rates. Granted, economic data of late have presented investors with a glimmer of hope but the outlook remains resolutely gloomy, especially with diminished fiscal support to US consumers. If there is a relevant macro backdrop to this adjustment higher in rates, it is to be found in the lengthening duration of government supply.

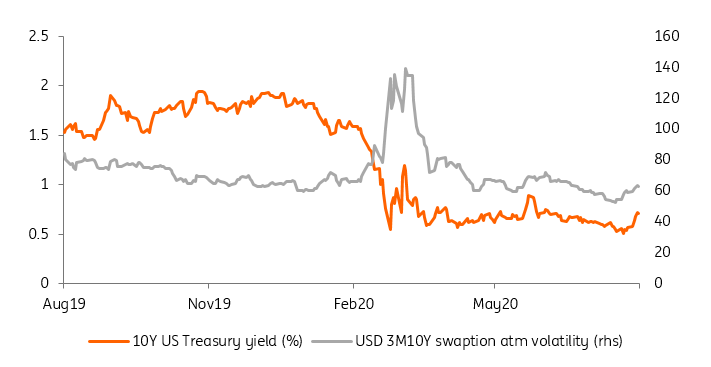

The move higher in rates and volatility has been modest so far

Near-term target: 0.90% in 10Y US Treasuries

Both in EUR and USD, the prospect for higher duration issuance is well flagged and our expectation was that yield curves would have to adjust steeper at the end of August to accommodate it. Markets being forward-looking in nature, it is not entirely surprising the move came a couple of weeks earlier than we thought.

In short, we see the August rates sell-off has having called time on carry-driven summer trading conditions. Low realised rates volatility is key in attracting investors to fixed income assets over the summer months. The recent sharp adjustment higher has shattered that illusion which in turn should limit rates’ ability to revisit their recent lows, both in EUR and USD. This is all the more true since a lot of the bad economic news is already priced in, for instance, Congress’s inability to reach a deal on fiscal support for the US economy.

Going forward, USD rates strike us as having a greater scope to adjust higher. 10Y US Treasury yields are currently about 20bp from their all-time lows, and we see scope for the move to extend another 20bp to 0.90%, the level reached in its June spike. To be clear, we have doubts about the fundamental case for higher rates but think summer liquidity conditions and angst about the upcoming wall of supply skews the odds in favour of higher rates.

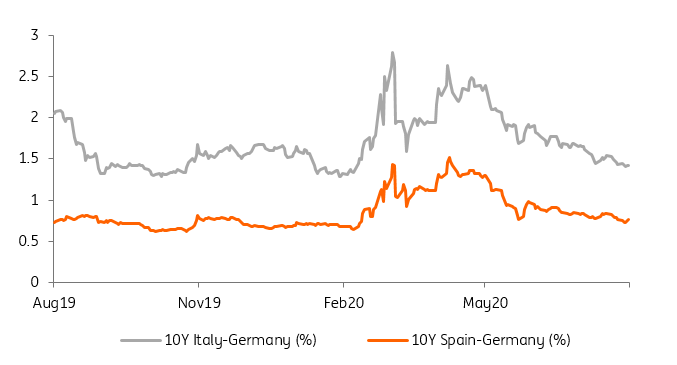

Peripheral spreads undeterred

Beyond US Treasuries: No threat to periphery spread tighteners

In the near term, stocks and the Fed are the potential kill switches to a USD rates sell-off. On the former: risk assets do not seem troubled by the, admittedly small by historical standards, rise in rates and rates' volatility so far. A correction lower in risk assets would help stabilise price action in US Treasury by re-directing some much-needed flight to quality flow toward them. Fed verbal intervention could also help investors regain confidence in US Treasuries. The Fed’s caution in its recent communication echoes our own, but we think something more tangible, for instance, a discussion of longer duration of QE purchases in next week’s FOMC minutes, is needed.

In EUR rates, we feel this is not enough to call our view of ever-tighter peripheral spreads into question. Granted, higher rates' volatility puts carry-driven longs in peripheral bonds at risk but, as our economics team pointed out, hopes of the ECB boosting PEPP should more than offset this temporary spike. We thus stick to our 125bp target for 10Y Italy-Germany spreads. Core and EUR swap rates should suffer from the same pullback as their USD counterparts but we see their capacity to rise as being more limited. The result should be a further widening of USD-EUR yield spreads.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid-19, Asia’s lamentable green response, and a slow, slow recovery

- This bundle contains 8 Articles