Rates Spark: Whatever you say

- 24 February 2021

- Rates

Fed Chair Jerome Powell's testimony is a delicate balancing act between acknowledging the upsides ahead, while keeping both hands on the easing button. If this is the real deal and rates upside continues, the US 5yr should not be as rich as it still is, and US real rates should not be as low as they still currently are. But then again, these anomalies also add pause for thought on the structural validity of the reflation theme

Fed, tapering, in the market’s mind, that boat has sailed

There was little to surprise financial market participants in Chair Powell’s testimony yesterday but his forceful tone did manage to elicit a non-negligible reaction in rates markets. In summary, a repeat of the familiar dovish theme was his main message. The Fed will remain accommodative to favour broader and more inclusive job market gains. He also dismissed the inflationary risk brought by fiscal stimulus.

The tapering boat has sailed already

The message to rates markets is clear: it is too early to discuss asset purchase tapering, let alone raising rates. Yet both are being priced with an increasing degree of conviction in rates markets. In our view, market confidence in the strength of the US recovery is so strong and widespread that the tapering boat has sailed already, in investor minds. Surveys carried out in January by Bloomberg and by the New York Fed both highlighted that consensus is for tapering to start in 1Q 2022, we think it could start earlier, in 4Q 2021, and we expect consensus is converging to our view.

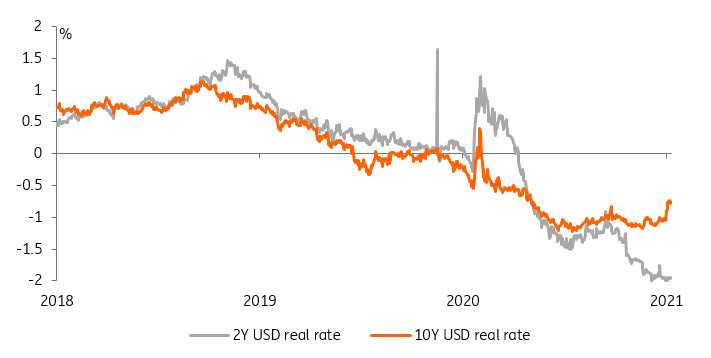

USD 10Y real rates have risen, showing a focus on policy tightening

Focus is on Fed tightening, and this is weighing on inflation swaps

There is an even greater disconnect between the Fed’s message on interest rates and what the Fed funds curve is pricing. The latest Fed projections show no hike taking place before 2024, while the curve is pricing roughly one hike in 2022, two in 2023, and two in 2024. This in itself is sufficient to explain sluggish performance in risk assets, and why inflation swaps have flatlined recently.

And yes this may only be the start. Bill Dudley, formerly of the New York Fed, has flagged that up to 200bp of tightening per year could be necessary once full employment is reached in the US. Clearly, this is a high bar to clear but some prominent economists, including Treasury Secretary Janet Yellen, think this can be achieved by 2022. Compared to Dudley’s 200bp estimate, the less than 50bp of hikes priced for 2023 and 2024 each does not seem that high any more.

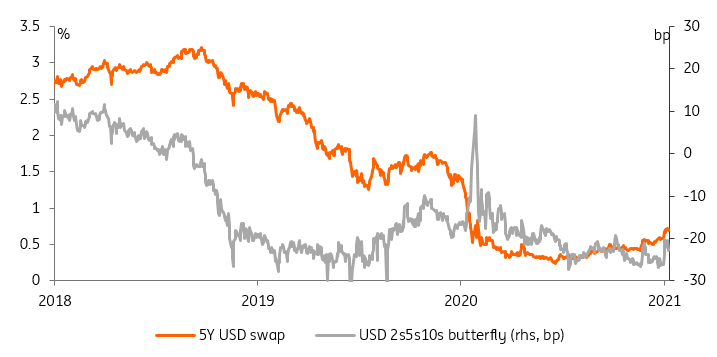

5yr could cheapen further if hikes come ino focus

If he’s right, the belly (5Y) of the curve has further adjustment to do. Right now, the 5yr remains rich to the curve. As the outlook for rates ahead shifts, the 5yr should cheapen to the curve. As a guide, in 2013 when the Fed tapered, the 5yr swung viciously from rich to cheap; a sure sign we were in a bear market at the time. While this is not a taper tantrum, in some ways it is a tamper on inflation concern, a more traditional route to higher yields. If so, that 5yr should not be as rich as it still is.

5yr should not be as rich as it still is

The same should be said of US real rates. If this is the real deal, then the 10yr real yield should not be at -90bp. While it has moved from -120bp (in fact causing the implied inflation breakeven to edge tighter in the past week) it is still not consistent with a true structural reflation theme ahead. The real deal requires higher real rates (or at least less negative) - then we'd really be talking true reflation, one that is not a 2021 flash in the pan.

ECB: look at what I say, not what I do

With all the debate happening in the US, it is tempting to overlook the policy debate in the eurozone. This would be a mistake. EUR rates have recently been more volatile than their USD counterparts. They retraced the whole of the drop that followed ECB President Christine Lagarde’s verbal intervention in less than 24 hours.

There has been no discernible increase in the ECB's weekly asset purchase amount

We think there is a stronger rationale for the ECB to prevent rates rises than the Fed, due to the more sluggish inflation outlook in the eurozone than in the US, and much more modest fiscal support. Yet markets seem to have almost dismissed Lagarde’s comments. One factor might be that so far, the ECB has not put its money where its mouth is: there has been no discernible increase in its weekly asset purchase amount.

A way forward could be a form of ‘real’ yield curve control

Something more profound might also be at play. With a history of tightening policy too early, markets might question whether the ECB would actually increase purchases to revert an increase in rates that has its roots in a better economic outlook. We suspect opposition from the hawkish wing of the ECB to greater purchases could be fierce, but our economics team thinks that a way forward could be a form of ‘real’ yield curve control, where it seeks to limit increases in real yields. This we think, should be sufficient to put USD-EUR rates differentials back on a widening path.

Today’s events and market views

The events calendar is actually fairly light, but there are plenty of macro dynamics to drive rates markets (see above). We think this macro environment is conducive to higher rates. There are indeed legitimate concerns about the speed of the rise and its impact on other markets so we expect its speed to be limited.

The focus will probably be on central bankers. From the Bank of England, Governor Andrew Bailey, Deputy Governor Ben Broadbent, and policymakers Gertjan Vlieghe and Jonathan Haskel are due to testify before the Treasury Select Committee. From the Fed, Jay Powell, Lael Brainard, and Richard Clarida make up the slate.

The main economic release of note will be US new home sales.

Germany will auction €4bn of 10Y debt.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more