Rates Spark: The tone is set

US CPI expected to rise to 7% will be the main headline-grabber today, but we think the (hawkish) tone is already set in markets. In EUR rates, the curve steepening shows that supply is the dominant driver. We think further rates upside will happen at the long-end, given the already high hike discount

Powell didn’t pour more oil on the fire, but the tone is set

We’d argue that, at this stage, higher-than-target inflation is a well-accepted fact across markets, and that investors are more focused on how central banks will react to it. Fed Chair Powell largely refrained from pouring more oil on the hawkish fire at his Senate hearing yesterday, save for comments that will prompt markets to bring forward the expected date of balance sheet reduction (quantitative tightening, or QT). His comments that QT will come 'sooner and faster' might achieve to cap the number fo hikes priced by the curve this year at four, and instead put the focus on balance sheet reduction, starting around the middle of 2022.

Powell's comments will prompt markets to bring forward the expected date of balance sheet reduction

In this light, we think the bar for today’s US CPI print to prompt another large rates sell-off is slightly higher than the 7% Bloomberg consensus. There is also the argument that, as last week’s job report has demonstrated, employment indicators carry more weight in the way interest rates anticipate Fed tightening. This isn’t what Powell said yesterday, but we think the fall in unemployment in particular has already set the tone in markets. All this is to say, we expect USD rates to continue drifting higher today, but US CPI might not be the main driver.

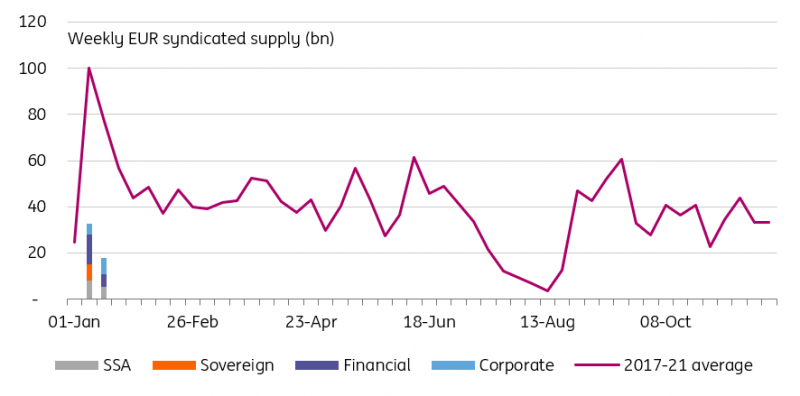

EUR curve steepening shows that supply is the dominant driver

Meanwhile, borrowers continue to queue around the block to sell bonds to investors. Given the context, and despite some spikes in yields throughout yesterday’s session, that process has been relatively orderly. We reckon that a lot of the supply-related adjustment upwards in rates has happened since mid-December. That this process saw a steepening of curves is a sign that, at least in the Eurozone, supply pressure is the dominant factor in the rates sell-off, rather than concerns about ECB tightening.

Syndicated volumes are set to spike in January

We only expect the focus to shift to ECB tightening after the 1Q 2022 supply surge

We think both are potent drivers but we only expect the focus to shift to ECB tightening after the 1Q 2022 supply surge. For now, the debate is raging between hawks and doves on the ECB’s board. The deciding factor of which camp gains the upper hand is how the ECB’s inflation forecast evolves in the coming quarters (updates are due in March and June). If, as Isabel Schnabel fears, sticky energy prices prevent future inflation from falling back below 2%, then the focus will quickly shift to tightening. If, as Philip Lane believes, inflation falls back, markets are looking at a quieter second half of the year.

The EUR swap curve is already pricing more than 50bp of hikes by late 2023

The EUR swap curve is already pricing in a decent amount of hikes, over 50bp by end-2023, which is roughly in line with our own expectation. Even if markets have a well documented tendency to overshoot, we think this points to most of the further upside in rates being at the long-end. This is all the more true that supply looks sure to ramp up in the coming days and weeks.

Today’s events and market view

European economic releases offer little prospect of market moves in our opinion, but primary market activity continues. In addition to Germany’s 30Y auction, Portugal has mandated banks for the sale of a 20Y, a break with the tradition of starting the year with a 10Y launch. Based on previous long-end Portuguese deals, this one amounts to €3-4bn.

The December US CPI release looms large on today’s calendar. The acceleration of the core component is probably what will focus investors’ minds the most.

In supply, the US Treasury will sell 10Y T-notes.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more