Rates Spark: Shifty fifty

- 17 November 2022

- Rates Spark

Markets outside the US are also increasingly leaning towards 50bp being the next probable moves by central banks. European Central Bank speakers turning less hawkish and the rediscovered UK austerity should validate the rally in rates

50bp is becoming the new norm

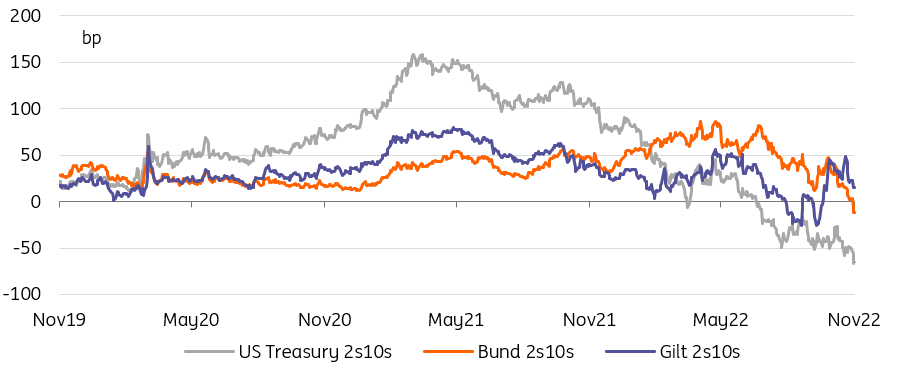

Looking at the Fed, markets have converged on a 50bp hike in December following the US CPI data. Fed officials have attempted – with some success – to push back against the pricing of the terminal rate dropping too much, and it has since hovered just below 5%, but it hasn’t prevented longer rates such as the 10Y UST slipping below 3.7%. Appetite seems to have returned to longer durations with yesterday’s 20Y auction also posting very decent metrics.

In the eurozone, ECB officials also appear to have dialed down their hawkishness. When arch-hawk Holzmann of the Austrian central bank is mindful that too strong tightening would not just lead to stagnation but to a recession, then markets should take note. Even with its new ECB reaction function, there appears only so much pain officials are willing to tolerate.

Renewed appetite for duration risk is flattening yield curves

The ECB’s hawks might ask for more progress on quantitative tightening

The ECB's shift was later corroborated by a Bloomberg story suggesting that momentum for a further 75bp move was lacking. With the market still eyeing a 20% probability of a larger move in December, there is still room to test a little lower. Alongside central bankers seemingly more mindful of the recessionary risks appears to validate the rally in rates that has also pushed the 10Y Bund yield below 2%. But mind you, that the ECB could eventually slow once the key rate approaches a neutral level – seen around 2% – is not news. With a view to the December meeting we caution that the ECB’s hawks might ask for more progress on quantitative tightening in return for less aggressive action on rates. The tightening of monetary policy could thus just rely to a growing degree on the balance sheet. That could eventually test the current indiscriminate rally across sovereign credit in the eurozone.

Gilts benefit from both fiscal tightening and the need for less BoE hikes

When it comes to the Bank of England, the next expected policy moves have become more interlinked with fiscal policies. This puts the attention squarely on today’s Autumn Statement that will outline the government’s fiscal plans. The government’s main task with a view to financial markets will be to rebuild credibility lost in September’s ill-fated mini budget. To that end much is already achieved by having forecasts of the independent Office for Budget Responsibility accompany the new plans. And looking at 10Y gilt yields, they have indeed already slipped back towards levels seen before the September budget just now.

The government’s main task will be to rebuild credibility lost in September’s ill-fated mini budget

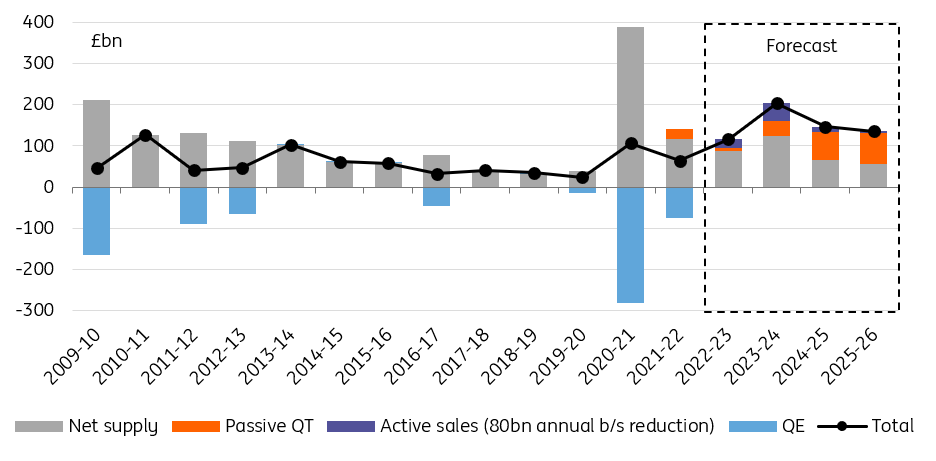

Perhaps the greater risk is that the government decides to push austerity too far under the impression of the rattling experience in the wake of the last budget. That could see markets further pricing out their Bank of England hike expectations. Long-end yields could also decline further, though our expectation would be that of an overall steeper curve. Keep in mind that the effective debt that private investors will have to absorb will see a considerable increase nonetheless. A Reuters survey among gilt dealers sees issuance in the 2022/23 financial year falling to £185bn compared to DMO’s September plans, but issuance in 2023/24 will rise towards £240bn. Crucially, one has to add the Bank of England’s quantitative tightening.

Private investors will be required to increase their gilt holdings by a record amount in FY2023-24

Today’s events and market view

Main event on the calendar is the UK government’s Autumn Statement. The FT has reported that up to £60bn of savings may be required, which is higher than had been expected. Reports also suggest the Chancellor will more heavily focus on spending cuts than tax rises.

As our economist notes, the impact on the economy will depend on how much of the burden is placed on consumers via higher taxation, and how immediately those changes come through. A fair amount of pain could be delayed until after the 2024 election. Another point to watch are details on how the government intends to restructure its flagship Energy Price Guarantee, which can have more direct bearing on funding needs.

Away from the UK the focus remains on central bank speakers and how they bridge the gap between signaling a slower pace and ensuring that financial conditions don’t already ease too much. Scheduled today are the Fed’s Bullard, Mester, Jefferson and Kashkari.

In data the focus is on the US housing market where numbers should be softer due to the rapid rises in mortgage borrowing costs that have prompted a collapse in demand. Also on the calendar are initial jobless claims as well as Philadelphia and Kansas Fed activity indices. The eurozone see the final CPI for October.

Today’s supply comes from France in shorter dated bonds as well as inflation linked securities, as well as Spain with taps in 3Y to 20Y bonds.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more