Rates Spark: Second round effects

Don’t look just at how many hikes are priced by yield curves to assess whether investors have come to terms with central bank tightening. We think second round effects on broader markets are under-priced. Barring any further adverse developments from Russia, we think this week will be used by investors to reduce their fixed income exposure

The Bank of Japan (BoJ) is the latest central bank to add to upward pressure on rates. Its decision today to revise growth and inflation projections upwards lets markets envision a world where the BoJ takes its foot off the monetary easing accelerator. In the same vein, the central bank has also upgraded the risk around its forecast to "balanced". Governor Kuroda stressed that no tightening decision is needed yet, but the impact of Japanese investors chasing higher rates abroad means that any hint of slower easing in Japan would remove a lid on yields elsewhere in the world.

Can bond yields rise without new information?

This week is a good opportunity to answer an academic question: is all new information priced instantly by financial markets? This is because the lack of what we would term tier one economic releases and the Fed’s pre-meeting quiet period should translate into a lower volume of headlines. This is if the new German foreign minister’s visit to Moscow does not serve as an opportunity for another volley of hawkish comment by the belligerent party. Market reaction would be relatively predictable: curves bull-flattening across core markets. On the positive side, investors have had to contend with fairly adverse headlines last week so the hope is that the threshold for a rally is slightly higher as a result.

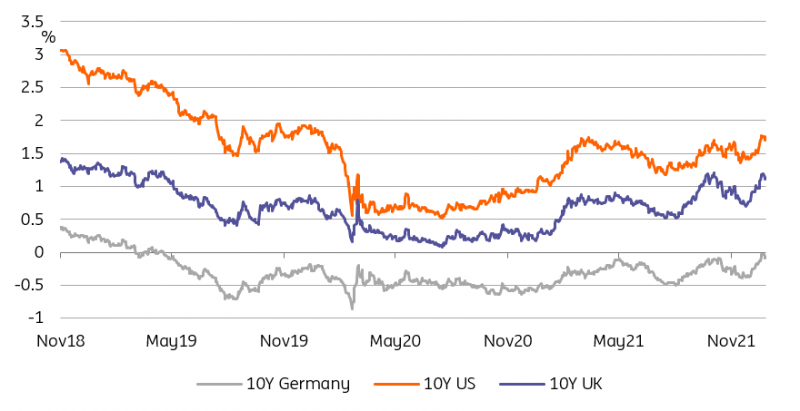

We expect the rise in core bond yields to continue into this week

Our hunch is that investors will use this window of opportunity to reduce their fixed income exposure

On the broader question of what we expect price action to be into next week’s FOMC, our hunch is that investors will use this window of opportunity to reduce their fixed income exposure. There can be, and is, a legitimate debate about how much the Fed can tighten policy (see our detailed analysis here). According to one side of that argument, the curve is already pricing more tightening than signalled by the Fed over the two coming years. This in turn is seen as a sign that markets have come to terms with a hawkish Fed (by recent standards).

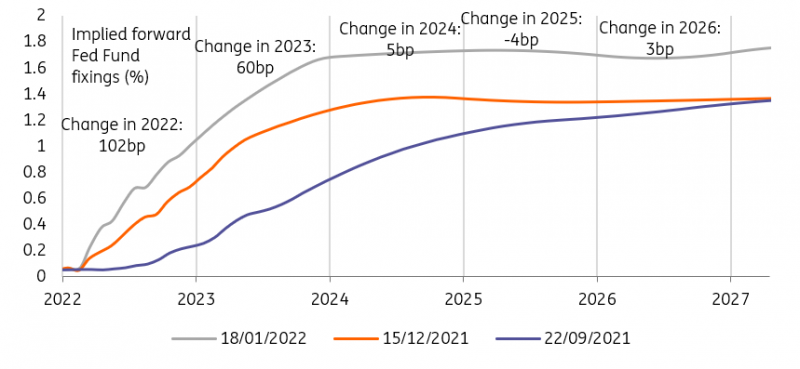

The US curve now pricing 4 hikes this year is only half the story

Second round effects have been drowned by plentiful liquidity and ongoing Fed purchases

We are not so certain. A single-minded focus on the number of hikes priced by the curve misses the second round effect of tightening. Markets are forward-looking by nature but they tend to give precedence to the short-term situation over the longer term when they give contradictory signals. For now, these second round effects have been drowned out by plentiful liquidity and ongoing Fed purchases. This is a dangerous situation for bonds everywhere, and the Fed’s new habit of apparently taking pot-shots at the long-end means that the usual strategy of shifting exposure to longer maturities is no longer valid, at least until the Fed has clarified its intentions.

Today’s events and market view

The most market-moving potential in European hours comes from the January ZEW survey. Consensus is for a modest improvement of the forward-looking component.

Belgium has mandated banks for the launch of a new 10Y via syndication yesterday. As an indication on size, it raised €6bn via a deal in the same sector this time last year. Other bond supply include Germany launching a new 5Y Obl via auction and Finland selling bonds in the same sector.

Francois Villeroy is the sole ECB speaker on the slate for today.

In US hours, the empire manufacturing survey will give an early flavour of sentiment in January. This will come on top of the NAHB housing market index.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more