Rates Spark: Real yields ease

A remarkable pull back in US real yields, reversing the post Powell spike, with demand for linkers in play. Despite geopolitical tensions stirring in the background the Fed meeting has refocussed markets on the ongoing monetary policy shift, thus setting the stage for the policy setting meetings of the Bank of England and European Central Bank next week

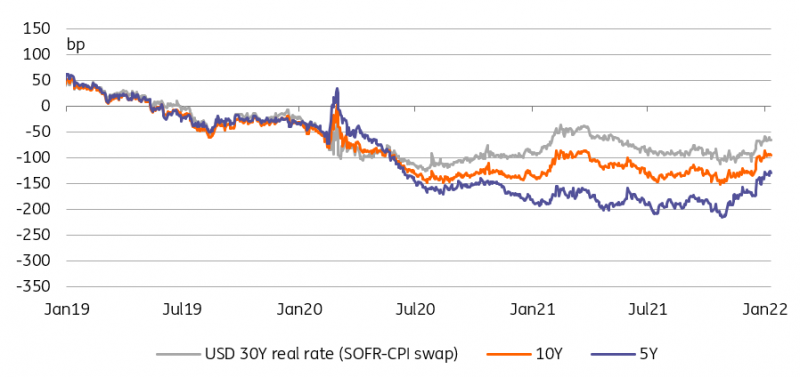

US long real yields have manged to retrace 100% of the post Powell spike. Why?

There has been interesting price action in US rates in the past 24 hours, especially in longer tenors. It’s not that the 10yr yield eased off the highs hit post the FOMC outcome; that was always a possibility. It’s more the unusual fall in the 10yr real yield, which in fact retraced 100% of the rise seen after Chair Powell said what he had to say. The rise in the 10yr yield post Powel was 100% driven by higher real yields, so this about-turn is quite something. The only reason that the 10yr yield itself did not retrace fully was that inflation expectations in fact rose, if only by a couple of basis points.

10yr real yield is back below -60bp. It likely reflects a spike in demand for inflation linked bonds

The full retrace of the 10yr real yield is quite a disappointment for players that look for a move, even if gradual, towards a less negative real yield environment, thus returning rates to a more normal footing. The 10yr real yield is back below -60bp. This likely reflects a spike in demand for inflation linked bonds, as these pay a real yield. And the negative real yield is compensated by the fact that they also pay delivered inflation, which remains impressively high. The GDP report yesterday confirmed this, with the price index running at just short of 7% and core PCE at just below 5%. Heady numbers.

US real rates have retraced their post-FOMC jump

For as long as inflation plays out like this, real yields can be kept under wraps. As inflation eases, we should see the reverse, and real yields should ease higher again. We remain of the opinion that this is the clearest route to getting nominal yields higher in the months to come.

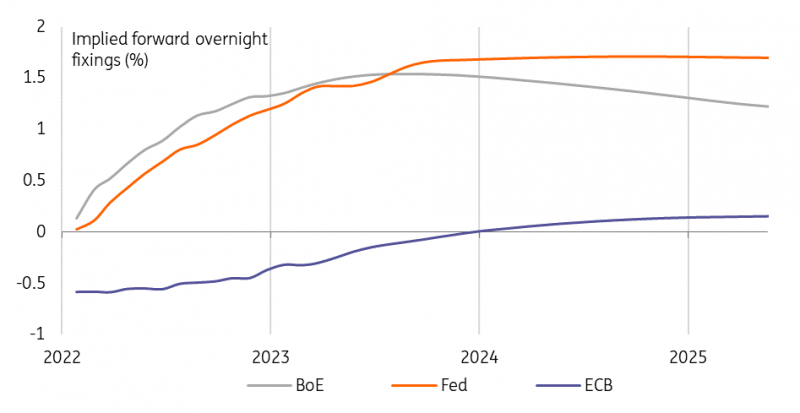

Meanwhile, US money markets have moved towards pricing in five 25bp hikes this year and two more in 2023, that is despite the underlying weakness behind the latest 4Q growth figures, and also fears that the upcoming jobs data next week could disappoint. Fed Chair Powell has strongly hinted the central bank is prepared to look through near-term economic weakness as inflation pressures remain elevated. Barring escalation of geopolitcal tensions this sets the course towards higher rates, not just in the US but other developed markets are likely to get caught in the slipstream.

Markets discount a steeper rise in central bank rates

The ECB is gradually shifting position, but markets are well ahead

As much as the ECB likes to stress its independence and differentiate itself from the US, there has clearly been a pass through of tightening expectations into Eurozone markets. EUR money markets are pricing a 35bp increase in the overnight rate by the end of the year. This is more than a full 25bp hike of the deposit facility rate even accounting for some uncertainty surrounding the potential repayment of the ECB targeted liquidity operations and resulting reduction in banks’ excess reserves over the summer.

expectations are still at odds with ECB statements that a rate hike would unlikely occur this year.

Money market expectations are therefore at odds with ECB officials' multiple statements that a first rate hike would very unlikely occur before the end of the year. That position is in line with the prospective sequencing of the ECB's gradual policy normalisation and the guidance it has provided on net asset purchases. Recall, only last December it was announced that PEPP net buying will end after March and APP purchase volumes, initially to be ramped up to buffer PEPP's end will then gradually decline towards €20bn per month again by the end of the year. What happens thereafter is left open.

Eurozone inflation retreating from 5% next week could lessen the pressure on the ECB

Is market pricing overdone? Perhaps with regards to the current year. The upcoming week will also see preliminary CPI data for January, starting with Germany on Monday which should show a significant drop in headline inflation from close to 6% to below 4%, mainly as a temporary VAT cut drops out of the calculation. It will filter through to the Eurozone inflation rate that should retreat from 5% and presumably that could lessen the pressure on the ECB to shift its position more quickly. But as said, it's partly base effects that have been well flagged and the underlying pressure may well stay elevated going forward.

Making an argument for noticeably less aggressive pricing would also have to rely on geopolitical tensions flaring up and severely denting risk sentiment. And keep in mind that there is the BoE to contend with on the same day as the ECB meeting...

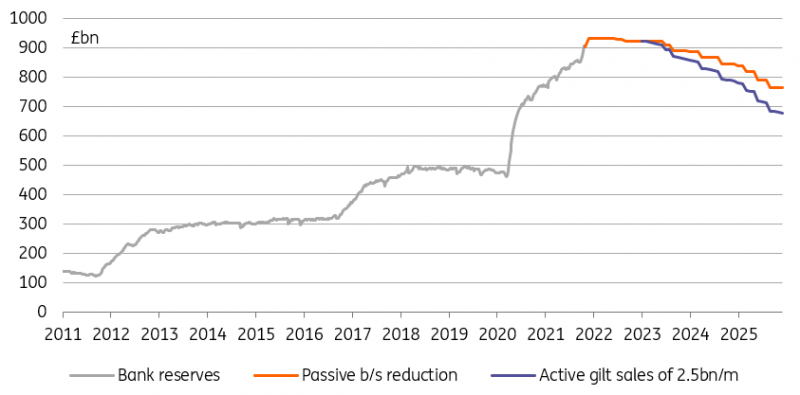

It is the BoE we will be looking to for more concrete action

While we will be following the ECB closely to catch the nuances of a further shifting discussion surrounding the inflation outlook, it is the BoE that we will be watching for concrete action. Our economist sees a 25bp hike next week as a base case. That hike has implications beyond the mere key rate level – it will kick off the quantitative tightening of the balance sheet as the Bank said it would stop portfolio reinvestments once the key rate reaches 0.5%. And there are sizeable Gilt maturities coming up in March.

Another BoE hike means balance sheet reduction can start in March, passively at first

a 25bp hike next week as a base case – and it will kick off quantitative tightening

If the past November and December meetings have taught us anything, it is that the BoE is not shy about surprising markets. But our economist thinks that the more modest impact of Omicron on the economy seen in the data paired with Bank's growing worries about inflation will be enough to pull the trigger. Markets agree, discounting a more than 90% chance for a hike, and they go farther in plotting a path towards a rate of 1.5%, or more than four hikes in total, by the end of this year. Even if that may appear steep, market pricing currently works in favour of the BoE, doing some of the effective tightening of financial conditions. The BoE is unlikely to do anything to dispel this just yet.

Today's events and market view

As the end of the month nears, rates usually find themselves in a more supportive flows backdrop, also given that the supply activities should subside after the flurry of deals in recent weeks. But one reason for some of the syndicated deals being pulled forward (the 20Y Finnish bond for instance) are the upcoming central bank meetings. Arguably, for the slow moving ECB it could be more of a communication exercise, but from the BoE we expect concrete action in form of a rate hike. For the direction of rates that still points up.

Data wise today’s focus remains on the US. The Fed’s preferred inflation measure, PCE inflation is seen rising to 5.8% year-on-year. December personal income and spending should see spending fall sharply given the steep decline already seen in the retail sales figures.

Primary markets will see Italy selling 5Y and 10Y bonds as well as floating rate notes.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article