Rates Spark: The burning question is whether payrolls agrees with the ADP

- 7 July 2023

- Rates Spark

Moves yesterday took us to break-out levels for market rates. It does not feel like the move is over yet, and today's payroll report will have its say first. A weak report would look like a contradiction given the ADP, but payrolls are still the dominant driver. The market will also have an eye on US CPI next week

A consensus-type outcome for payrolls will take market rates off their highs

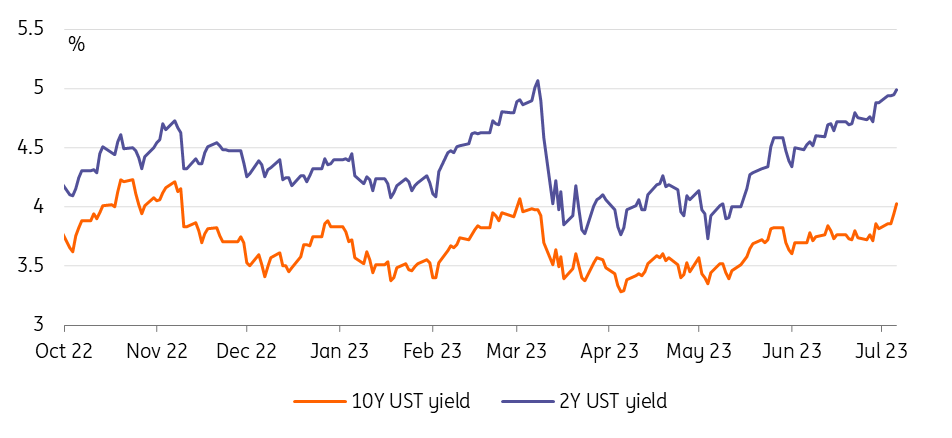

The latest report from ADP National Employment for June reported a 497k increase in US jobs. That is undoubtedly strong, and double the 250k average seen in recent months. Challenger job cuts also showed a slowdown in cuts, also pointing to resilience in the labour market. The American economy is fighting back, despite what the Fed has been up to. The 10yr is now at over 4%. We think it will stay above 4% over the coming weeks and potentially months. And the 2yr will hold on to a 5% handle, with a 100bp curve inversion being sustained. The inversion points to a reversal lower in market rates ahead, and a recessionary tendency. While that sounds unseemly given what we see in front of us, the rise in market rates will ultimately have its effect. But that’s not the focus for now – the focus is on taking out prior highs hit in this cycle for market rates.

The Services ISM report confirmed that the situation popped higher in June. The employment component, which had dipped below 50 in the previous month, is now at 53.1. New orders rose to 55.5, and the overall index to 53.9. These are not particularly high readings, but importantly they are reversing some of the declines seen in previous months. Prices paid also eased lower, to 54.1. That in fact is a very tolerable outcome, as the long-run average for prices paid is 60. Market yields can be comforted by the calming in implied inflation expectations. But it can, at the same time, be a tad concerned that macro strength in the services sector could frustrate ambitions to get inflation materially lower in the coming months. So nothing here to reverse the tendency for yields to test higher.

Get used to a 4% handle on the 10yr – it’s here to stay for a while. That said, we will need to see the payrolls report first. It's a June report, the same as the ADP. The question is whether it shows the same spurt that the ADP did. Often the correlation between the two is remarkably weak. But even if we get a consensus outcome in 200k plus territory that would not take market rates materially off their highs. For that, we'd need to see a material rise in the unemployment rate and a notable fall in wages inflation. Neither of these are expected. If we get a consensus-type report, it is possible that the market takes yields off their extremes into the weekend, but we'd still maintain that there has been enough in the past few days of data for any pullback to be reversed next week, and for the push higher in yields to continue.

2Y UST at 5%, 10Y at 4% and now eying cycle peaks

The week ahead will shine a light on the inflation side

Data in the week ahead will shine a light on the inflation development in the US with CPI taking centre stage on Wednesday. The consensus is looking for the headline rate to drop to 3%, but given that this is mainly down to known base effects, it will likely be outweighed by core inflation remaining uncomfortably high at 5%. Persistent core inflation also means no let-up in Fed hawkishness. Nonetheless, there are also other indicators to watch which should point to declining pipeline pressures like the producer prices. Also, keep an eye out for the University of Michigan consumer sentiment survey and its inflation expectations measure.

In the eurozone, the main releases are the final CPIs as well as the European Central Bank accounts of the June meeting. Remember that the ECB all but preannounced another hike for this month. Given the disappointing macro backdrop and question marks surrounding the tenability of the ECB’s hawkish stance, markets will most likely scrutinise the accounts for any growing concerns about the underlying economy which could pave the way for a more heated debate between the hawkish and dovish camps. The balance sheet may feature given the targeted longer-term refinancing operations repayment, but we don’t suspect any discussion around extending quantitative tightening with asset purchase programme reinvestments having stopped just this month.

UK jobs data, and in particular wages, will be a focus for sterling markets where the 6.50% terminal rate is now almost fully priced for the first half of 2024.

Today's events and market views

All eyes are on US non-farm payrolls number today after the huge surprise in the ADP estimate. The consensus still stands at 230k, but Bloomberg’s whisper number, which compiles individual user estimates, has jumped to 270k. The unemployment rate is expected to ease back to 3.6% while average hourly earnings are seen to have risen by 0.3% month on month again.

Unless there is a huge downside surprise, that would put the job market’s resilience into question. We think the 4% handle for the 10Y UST could accompany us for a while. The counter notion is that the sheer size of the move should call for at least some reversal, but if anywhere we would make that case for Bunds that got dragged higher alongside Treasuries. It also appears that fall-out for risk sentiment was more noticeable in EUR space, in sovereigns certainly with spread widening, which could add to the resistance against a further move higher.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more