Rates Spark: Hawkish blinkers

- 1 September 2022

- Rates Spark

Markets now favour a 75bp hike by the European Central Bank in an upcoming meeting, ignoring the drop in energy prices this week. Gilts are suffering from fears of fiscal spending and foreign outflows

Bonds have their hawkish blinkers on and miss a drop in energy prices

A beat in core eurozone CPI, with our economist flagging worrying signs of second-round effects from energy to goods prices, has tipped the scales in favour of a 75bp ECB hike in September. The market is now pricing 125bp of tightening over the next two meetings. Another flurry of hawkish comments, from the usual suspects Joachim Nagel and Robert Holzmann, helped convince investors that hawks are winning the front-loading hike debate. What’s more surprising is that the further rise in front-end rates and, expectedly, curve flattening, occurs while European-traded energy prices continue their decline this week.

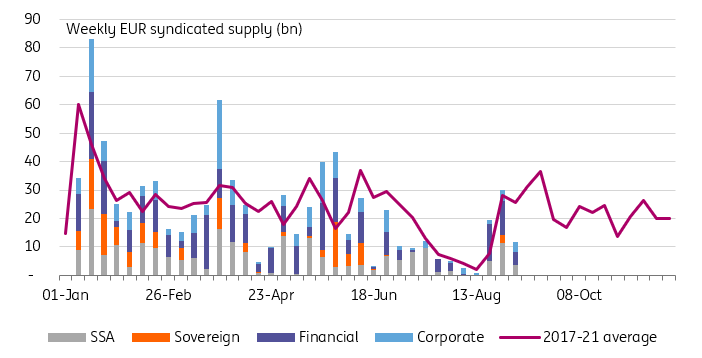

September and October are shaping up to be busy months in terms of supply

With so much hawkishness priced and some relief in traded energy, it is tempting to call the peak in 10Y Bund yields, but there is another factor at play. September and October are shaping up to be busy months in terms of supply. Even if volumes do not match the previous years, we ascribe lower issuance to more difficult liquidity conditions, we would expect a greater market impact. The first eight months of the year are a case in point, despite lower volumes, supply has put greater pressure on bond yields across the credit spectrum.

Bond sales should push bond yields higher in September and October

Gilts have no (foreign) friends

UK rates continue to rise relative to their European and US peers. As we wrote recently, divergence in energy prices and inflation explains their jump relative to USD yields. As for the faster rise than European peers, one needs to dig deeper into UK-specific problems. In an economy that is generating a greater proportion of its inflation domestically, the coming fiscal support package stands a greater chance of resulting in a more aggressive Bank of England (BoE) tightening cycle. These fears are probably exacerbated by the current leadership vacuum and the uncertainty about the extent of extra spending and tax cuts that will be unveiled.

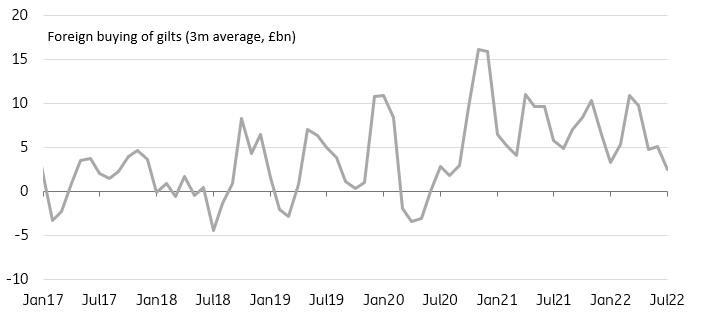

Fears of fiscal profligacy tend to hit gilts harder. Due to a (historically at least) wider current account deficit, UK markets are more sensitive to a worsening of its twin deficits. The recent decline in net overseas buying of gilts, still positive but the lowest on a rolling three-month basis since 2020 when fears of a mini run on the sterling were rife, did not help. We’re still far from the simultaneous sell-off in UK bonds, stocks, and currency that occurred in March 2020 and prompted the BoE to restart quantitative easing, but the parallel sheds an awkward light on its plan to actively sell bonds, on top of ‘passive’ balance sheet reduction.

Foreign buying of gilts is at its lowest since 2020

Today’s events and market views

Most manufacturing PMIs released today will be second readings with the exception of the Dutch, Spanish, and Italian indices. Italian and eurozone unemployment complete the list of European releases.

Supply will remain an important driver of short-term price action with Spain (3Y/10Y/30Y and linker), France (9Y/10Y/16Y), and Ireland (10Y/30Y) lined up for today.

In the afternoon, US PMI manufacturing is a second reading but its ISM equivalent is a first. In addition to a decline in the headline figure, markets will look closely for a further drop in the prices paid component. Jobless claims and construction spending are the other US releases we look out for.

The pre-ECB meeting quiet period starts today so we would be surprised to hear Fabio Centeno make any comment on monetary policy. The Fed’s own quiet period only starts this weekend so Raphael Bostic might try to out-hawk his colleagues.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more