Rates Spark: Geopolitical distractions

- 21 January 2022

- Rates Spark

While the discussion on inflation risks is becoming more open also at the European Central Bank, Lagarde is still setting her policy apart from that of the Fed, which could well decide to end Quantitative Easing entirely next week. A case for higher rates, but the policy nuances are currently pushed to the background as geopolitical fears continue to rise

Bond yields are driven lower as geopolitical fears rise to the fore with little sign of de-escalation surrounding the Russia-Ukraine tensions. That supportive backdrop for rates markets may well extend as technical headwinds are also subsiding – new issuance activities are likely to calm with the next crucial central bank meetings drawing closer.

But the latter should come as a reminder that monetary policy is tightening faster and sooner. Our economists do not exclude that the Fed will announce an end to its asset purchases already at next week's meeting, setting the stage for a first interest rate hike in March.

Some at the ECB are concerned about too flat a yield curve as hikes approach

The ECB keeps its flexibility, but the fate of ECB QE is likely sealed already

ECB President Lagarde, in an attempt to defend the more cautious approach to rising price pressures, stressed the different backdrops against which the ECB and – for instance – the Fed are currently acting. While holding on to the projection of inflation easing back below 2% by 2023, the minutes of the December ECB meeting showed a more open discussion of risks surrounding the inflation outlook, highlighting also the shortcomings of the ECB models that are calibrated on pre-pandemic data.

All dovish soundbites aside, the minutes are a reminder that the ECB is normalising policy.

We think sealing the fate of also the ECB's asset purchases, is the Council’s view that the cost/benefit of additional asset purchases was worsening. Market distortions surrounding the increasing collateral scarcity into the end of 2021 likely played into that notion and Isabel Schnabel had outlined these issues already in a speech ahead of the December meeting – noting deteriorating market functioning and rising risks to financial stability if not properly managed. Interestingly, there was also an argument put forward that continuing asset purchases could flatten the curve at the time the ECB starts its hiking cycle. This is quite similar to recent Fed thinking. All dovish soundbites aside, the minutes are a reminder that the ECB is normalising policy. The trajectory net purchases are now set on a course that will likely see them end with this year.

Scarcity of German government bonds implies durably wider swap spreads

The QE stock alone is unlikely to prevent higher rate levels

The ECB probably will hold c.50% of the German Bund stock...

Of course the emphasis is now shifting to the large bond holdings accumulated after years of QE. Understandable, as the ECB probably will hold somewhere around 50% of the German Bund stock for instance by the end of 2022 – a rough estimate given one has to take into account the prices the ECB paid and also on how many German agency and regional bonds are included in the reported data for German public sector holdings.

... but this alone will unlikely be enough to prevent the further rise of yield levels

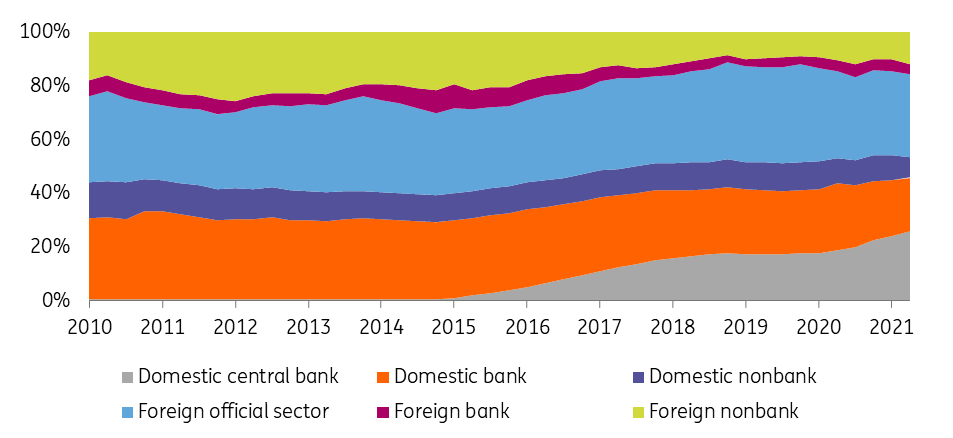

And the ECB is not the only official sector entity buying bonds. An IMF paper estimates other foreign official sector holdings of the German general government debt stock (i.e. a wider base than just Bunds) at 31% as of 2Q 2021, at a time when domestic central bank holdings were at 26%. That means over 50% of a pool of highly quality liquid assets, into which also banks have to tap in for regulatory purposes – they held 20%, is already tucked away. The ECB’s pledge to reinvest its holdings will prolong this situation. While this will likely ensure relatively low German government bond yields versus swaps for instance, we don’t think this alone will be enough to prevent the further rise of yield levels as policy normalises.

Holders of German general government debt

Today’s events and market view

With little sign of de-escalation surrounding the Russia-Ukraine tensions, the demand for safe havens keeps the upper hand for now. There should also be an easing of supply activities going into the important central bank meetings of coming weeks, which implies that rates markets could stay supported until then.

In terms of events today, we will be listening into a virtual panel at the World Economic forum where ECB’s Lagarde will join the discussion of the global economic outlook.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more