Rates Spark: The Fed to set the tone

- 21 September 2022

- Rates Spark

So here we are. Another FOMC meeting, and another 75bp hike. But there is a rump going for 100bp, so 75bp could be positive for risk assets (albeit briefly). The dot plot will be watched, as the terminal rate is key for where market yields peak. A 75bp hike takes the effective funds rate up to 3.08%, but leaves the Fed with more to do as the 2yr heads for 4%.

Expect a 75bp hike, although there is a rump positioned for 100bp

Ahead of the Federal Open Market Committe (FOMC) meeting there has been some market flows positioning for a 100bp hike, but the dominant discount as we head into the meeting is for 75bp to be delivered. A 100bp hike would be an over-reaction, in our view, while 75bp would be enough to solidify a market discount that is already projecting a terminal funds rate north of 4.25%. Chair Powell's Humphrey-Hawkins testimony followed by a re-acceleration in core CPI inflation has been enough to push the market discount up by some 100bp in the space of a month. At this juncture the Fed does not need to do much more than deliver the 75bp hike, and maintain a hawkish bias.

The Fed does not need to do much more than deliver the 75bp hike

The dot plot will be important, but not critical, as the dots do move over time. We think the median dot will print above 4% for 2022 (to be read as end year), and the Fed may well choose to keep it above 4% for 2023. The Fed's dot plot does print a longer-run rate at 2.5%, which is deemed to be their neutral rate, and is broadly where the funds rate is now. So the 75bp hike, when delivered, moves the policy rate into a tightening stance for the first time in this cycle. The calls for 100bp area partly premised on the notion of pitching the funds rate 1% tight versus neutral in one go. But 75bp also tightens policy reasonably aggressively, and avoids unnecessary market consternation with respect to future intentions.

The Fed's message is finally delivering tighter financing conditions

The terminal funds rate remains key for the bond market

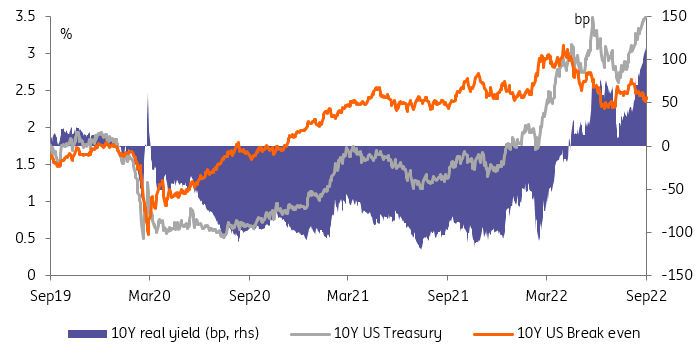

Beyond this meeting, where the funds rate peaks is critical for pitching bond yields. Once the funds rate is hiked, the new reference for market rates is north of 3% (with the effective fund rate set to settle at 3.08%). A similar hike in November would then have the ceiling at 4%, an area that the 2yr Treasury yield is currently targetting. History shows that the 2yr will anticipate moves in the funds rate well in advance, but as we get towards the end of the rate hiking cycle, reaction from the 2yr yield becomes smaller. Based off the price action of the past few weeks we are not quite there yet. But if the funds rate peaks at 4.25% to 4.5%, we'd be surprised if the 2yr yield were to get much above 4.25%.

Further out the curve the 10yr yield has more capacity to trade through the funds rate sooner than the 2yr. This is typical as the curve has moved into a state of inversion. In that sense longer tenor rates are being pulled higher by higher short tenor rates at this stage of the cycle. This is the opposite to what happened before rate hikes were discounted, as the curve steepened from the long end. Now the long end is waiting for the funds rate to come up and hit it. From there, likely around the 2 November meeting, the 10yr can trade flat to the funds rate (at around 3.75%, or slightly higher), and that would anticipate a peak in the fund rate at around 4.25% (actually 4.33%).

Right now the Fed does not want any focus on a rate hike discount

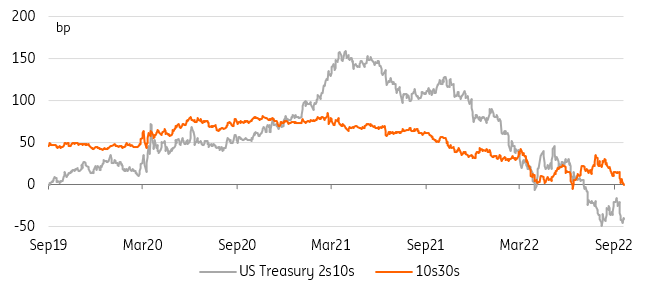

Once the peak in the fund rate is in with a reasonable degree of certainty, the 10yr can free itself from the shackles of terminal rate uncertainty, and can begin to trade well through the funds rate (anticipating cuts). Right now the Fed does not want any focus on a rate hike discount, but in fairness the market will tend not to aggressively discount a top until it actually sees it. This is where the value of a hawkish tone comes to the fore, as it helps to sustain that link with upward pressure on market rates generally. That said, with the 10/30yr spread now on the verge of inversion, expect any future peaking and fall in market rates to come earliest from the 30yr.

The Treasury 10s30s slope is on the verge of inversion

Today’s events and market view

Italy will exchange short-end bonds for issues in the 10Y and 15Y sectors worth up to €2bn. Germany will auction €4bn 10Y bonds. Austria mandated a new 4Y bond yesterday, which should be today's business.

Luis de Guindos is the only European Central Bank official on the schedule.

Both UK CBI prices and orders are expected to decline in September..

The FOMC meeting this evening looms large in an otherwise quiet session. The tone of the conference and quarterly economic and rates projections will be closely watched to shape future hike expectations. The thought leadership taken by the Fed, and the continued dollar rally, mean read-across to other rates markets is even greater than usual.

Ahead of the FOMC, US releases to watch will comprise mortgage applications and existing home sales.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more