Rates Spark: Economic resilience pushes rates higher

Long-end rates have returned to – or even surpassed – yield levels seen just before the start of the conflict in the Middle East. This is not to say that the market is becoming complacent about the crisis. Without it, we would likely be closer to a 5% UST 10y yield already, as data continues to point to a surprisingly resilient economy

Geopolitical concerns linger, but the story of economic resilience is also not going away

How the situation in the Middle East will evolve is still very uncertain, but high-level diplomatic efforts are all about containing the situation. Taking the oil price as a gauge for the tensions, we see no let up, with prices still 8% higher compared to just before the crisis.

At the same time, domestic data in the US continues to paint a picture of surprising resilience. Strong retail sales data proved wrong earlier indications derived from weekly credit card spending data. Industrial production data also surprised to the upside. Growth estimates for the second half of this year are being revised up, with our economist also seeing third-quarter growth in the region of 4% as likely.

The more dovish tones of Federal Reserve speakers that pointed to the rise in long-end term premia doing some of the Fed’s work and lessening the need for further hikes look less convincing in the face of resilient data. Markets are seeing chances slightly tipped in favour of another hike, not yet in November but in the months ahead. But more importantly, the prospect for meaningful rate cuts is being pared back, with the December SOFR futures implied rate having risen above 4.3%. For the 2Y Treasury, this has meant a rise to 5.23%, the highest since 2006.

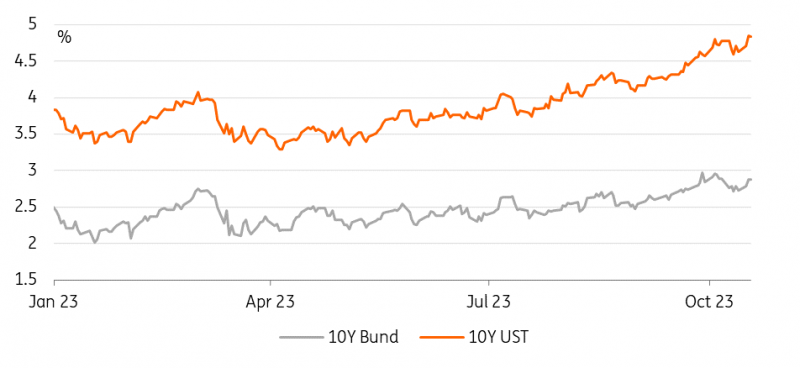

The US Treasury 10Y yield has risen above 4.84% again. Recall that 4.8% was the level where it closed the week following a strong payrolls number and just ahead of the Middle East conflict. Supply has probably played a part as well. After the weak 30y auction of last week, more price concession ahead of tonight’s 20Y UST tap should have contributed to yields surging higher again. Usually, auction-related market moves prove fleeting, but this time around the weaker demand is also symptomatic of more general concerns about the sustainability of the US government’s fiscal policies.

Over in Europe, yields are also moving higher again, though not as fast as their US counterpart. The 10y Bund yield closed above 2.88%, with the yield gap gradually widening again to above 190bp.

Long-term inflation expectations are still closer to their lowest reading since July, with the 5y5y forward inflation swap around 2.5%. However, oil prices complicate the situation for the European Central Bank as it risks putting a timely return to the inflation target out of reach. Front-end rates are above where they left off before the Middle East conflict.

Rates are pushing higher as data continues to surprise on the upside

Today’s events and market view

Long-end rates have returned or even surpassed yield levels seen just before the conflict. This is not to say that the market is becoming more complacent about the crisis. We would argue that, without it, we would likely be closer to a 5% yield in the 10Y US Treasury already. Purely looking at front-end pricing and the trough that is priced for the Fed funds rate, such a yield level would not look out of line.

After the September CPI for the UK this morning, the data calendar for the rest of today looks a little lighter. The eurozone looks at the final CPI reading for September and in the US, we get data on housing starts and building permits. More interesting will be the Fed’s Beige Book released later in the day. Last time, it mentioned concerns about the prospects for consumer discretionary spending. Today also sees another busy slate of Fed speakers.

Supply could prove the market moving again, with the US Treasury tapping its 20Y bond tonight for $13 billion. The European session sees government bond sales in Greece and a German tap of the 10Y Bund benchmark for €4 billion.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article