Rates Spark: Central banks’ heavy hands

- 3 August 2022

- Rates Spark

Central banks retain a heavy hand in these markets. The Fed is pushing back against the dovish interpretation of the July meeting, while the European Central Bank started intervention in peripheral bond markets through Pandemic Emergency Purchase Programme reinvestments

Here's how the US 10yr can re-test 3%

Yesterday we sent out a short report that focused on the dilemma to be potentially faced by the Federal Reserve in the months ahead. On the one hand, market rates have fallen dramatically, bringing with them falls in inflation expectations (the last bit is good). On the other hand, the Fed has an ambition to pitch the funds rate comfortably above the current rates that it terms the "neutral" rate. The problem is, should market rates continue to fall, by the time the Fed hikes again in September the 10yr rate will be below the Fed funds rate. If it were to break below 2.5% in the coming weeks, it risks being below the funds rate ahead of that meeting. While this is not catastrophic, it is also not a great look. The Fed should ideally be in tune with the market mindset, even if it needs to re-tune that mindset from time to time to get there.

The logic for a retracement higher is our view that the Fed is not done with hikes

We want to be clear here. We called the turning point at 3.5% in a timely manner. And turning points mean that market rates have peaked, and are set to move lower. But at the same time, turning points can be followed by structural falls in market rates, but interlaced by re-tracements higher, sometimes significant. The logic for a retracement higher is our view that the Fed is not done with hikes, and won't be done after it delivers another one in September. They will likely slow to a 50bp rhythm. But they are not done. We think policymakers will want to get the funds rate at least 1% above the neutral rate. To get there, the last thing they want is for the US 10yr to break below 2.5%. There is no precedent for the Fed moving so aggressively against such a market discount. So watch for the Fed to find ways and means to facilitate a rise in the 10yr back up towards 3%. That would be a better look for the Fed to work with.

Risk aversion explains low yields, but the Fed isn’t happy

We think there was a credible undercurrent of poor economic news driving government bond yields lower in the recent rally. The macro mood music is equally unpleasant on both sides of the Atlantic with the important distinction that Europe’s woes owe in large part to geopolitics, and more specifically to Russian gas flows. This is typically the sort of risk most investors aren’t comfortable putting a probability on. For that reason, we think current euro bond valuations are at least partially dictated by risk aversion flows, even if we agree with the view that more ECB hikes need to be shaved off the swap curve.

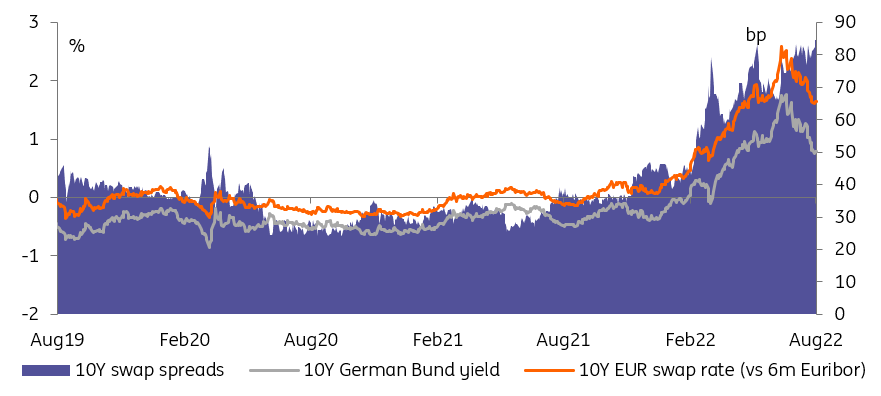

Wide swap spreads shows the important role played by risk aversion

current euro bond valuations are at least partially dictated by risk aversion flow

The most compelling piece of evidence for safe-haven flows playing an important role in the recent Bund rally is how wide swap spreads have become. To be sure, there are a host of underlying reasons that could explain it, for instance, fear of a more systemic crisis in Europe if Italy decides to tear up the EU fiscal rulebook after the September elections. Another potential explanation would be a drop in repo rates relative to euro short-term rates (Estr) as short sellers struggle to find bonds to borrow. There is probably some truth to both but we think the dominant factor remains investors seeking the safety of German bonds.

Over in the US, repeated warnings from Fed officials have helped to bring some much-needed two-way risk into Treasury yields. Comments from the likes of Mary Daly and Charles Evans sound increasingly like a concerted pushback against the dovish interpretation of the last FOMC meeting. It is only natural that the sharp sell-off seen since the comments has been in the policy-sensitive parts of the curve, with 2s10s bear-flattening in the process. We think any break of 10Y Treasury yields below the Feds funds rate would prove a temporary state of affairs.

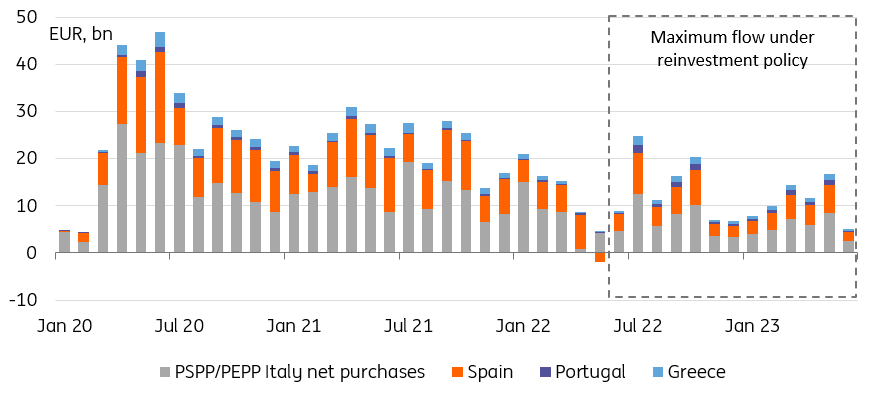

ECB intervention started in July, keep it up

Also on the topic of central banks, the data released by the ECB lumping together its purchases operations in June and July, does suggest reinvestments were indeed directed at peripheral bonds. The data isn’t very precise but it looks like the amounts are not far from the maximum allowed by core redemptions that month. In our view, PEPP reinvestments are a credible tool to manage spreads down, provided we are right in seeing only a limited amount of hikes in this cycle, and provided the ECB uses it persistently and to its full extent. In that regard, the data released yesterday is a step in the right direction.

The ECB should use PEPP reinvestments persistently, and to the full

PEPP reinvestments are a credible tool to manage spreads down

Other tools, such as the Transmission Protection Instrument, are a more distant prospect and come with heavy political baggage. It is clear the ECB would only use it in the most extreme cases. The irony is that this tool is so credible in fighting monetary-induced spread widening that spreads are unlikely to widen much for this specific reason. On the other hand, the TPI is more likely to be activated for edge cases, when its use is more controversial, and so when markets have reason to doubt it would ride to the rescue. We reviewed the size and effectiveness of the ECB’s toolbox in a dedicated note yesterday.

Today’s events and market view

Germany will auction €1.5bn of 15Y debt.

European services PMIs this morning are mostly final readings. The exceptions are Spanish and Italian indices. Their US cousin, ISM services, stands a better chance of dictating price action this afternoon. After the collapse in the ISM manufacturing prices component earlier this week, there will be a laser-like focus on price in today’s release. Markets might also look for last minute cues about the trajectory of the labour market ahead of Friday’s nonfarm payrolls. And this is not all, other US releases include mortgage applications and durable goods orders (final release).

Besides the busy economic calendar, the main focus is likely to be on Fed speakers. Today’s roster features Patrick Harker, Tom Barkin, and Neel Kashkari. As actual headline inflation prints continue to surprise to the upside, the Fed probably isn’t satisfied with the dovish interpretation of the July FOMC meeting or, at least, isn’t in a position to validate it. Recent Fed comments point in this direction and we ascribe most of yesterday’s sell-off to them.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more