Rates Spark: Action at both ends of the curve

In the US, we reiterate the notion that the 10yr yield can't really break lower, as there is no room to do so. So it must, in effect, head higher. While long-end EUR rates are also looking up, the Bundesbank's cut to government deposit remuneration added a twist steepening as it pressured the front-end lower

Continue to get comfortable with the US 10yr Treasury yield above 4%

We maintain our view that the US 10yr Treasury yield can remain above 4% for now. The key rationale centres on the material change in the rate cut discount that had evolved once the mini banking crisis (kicked off by the fall of Silicon Valley Bank) had materially eased. Once those fears abated, the market effectively went risk-on, and lo and behold the macro data began to perk up through June and July. That prevented the discount for Fed rate cuts from becoming overly aggressive.

Effectively the fund strip is discounting a move down to 4%, but not much below. That puts a floor on where the US Treasury yield can go when looking to the downside.

Remember, when Silicon Valley Bank went down, that same market discount saw the funds rate getting cut to 2.75% in 2024. That provided much more room for the 10yr Treasury yield to fall, and it did fall (to 3.3%). Things are different now though. Until something materially breaks in the economy, there will be no elevation in the rate cut discount. And in that environment, there is a more credible path towards higher market rates. Just for now. It won’t last long. We could well see the prior high in the 4.25% area.

But always remember that we are just one or two dodgy observations away in some key activity datasets for it to all come crumbling down. Payrolls have just past though, and that was not weak enough. So room to test higher.

The Bundesbank remunerates government deposits with 0% starting October

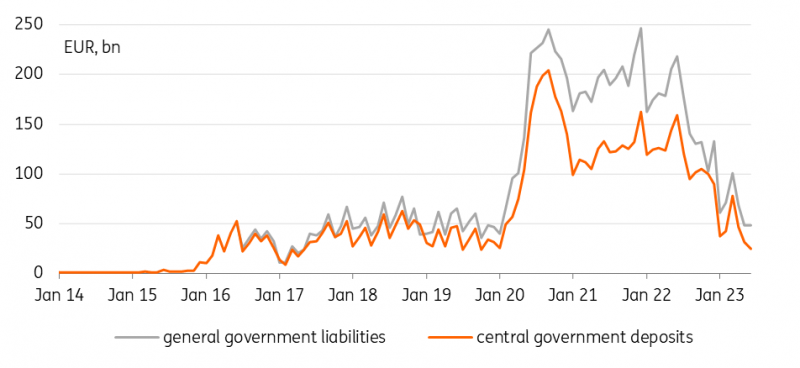

Starting in October, government deposits held at the Bundesbank will no longer be remunerated. The Bundesbank’s decision has raised fears of renewed collateral scarcity – after all, it was the European Central Bank’s waiver of the 0% remuneration cap on government deposits that was needed to counter the severe distortions in 2022 when ECB policy rates were lifted into positive territory.

The Bundesbank had signalled its desire to return to a 0% remuneration earlier, but expectations were generally for a more gradual return in line with the ECB’s incremental adjustments of the remuneration ceiling, rather than the one-time cut by effectively 345bp we are now seeing. Affected are only domestic government deposits which currently amount to around €50bn, and which could now push back into the market for high-quality liquid collateral.

The impact reaction yesterday morning was for the Schatz asset swap to widen more than 6bp towards close to 80bp, but it has already partially faded. For one, the largest part in the adjustment of government deposits away from the central bank is already behind us, as it had reached levels of close to €250bn during the pandemic at the Bundesbank alone. The changes will take effect only in October after all, so until then that still leaves uncertainty on how collateral will eventually be affected.

Flight risk: Government deposits at the Bundesbank

Today’s events and market view

As outlined above, in the near term we continue to see steepening risks with the US 10Y Treasury maintaining the 4% handle, all the more with this week's US issuance slate.

For European rates, the Bundesbank decision turned a bear steepening into a twist steepening as the German front end was pressured lower by renewed collateral fears. But the EUR long end is also seeing upward pressure as inflation swaps are marching higher. The EUR 5y5y inflation forward rose to 2.66% yesterday, the highest level since 2010. With the ECB having toned down its hawkishness at the last meeting, it has seemingly lost a grip on the market's long-term inflation expectations. But it is only one of many measures the ECB looks at to gauge expectations. Today the ECB publishes its consumer expectations survey, which also includes a survey on prices.

In primary markets, Austria reopens two bonds for €1.5bn and Germany issues €4bn in 5Y bonds. Later in the day, the US kicks off its quarterly refunding round with a new 3Y note issue of US$42bn.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more