Rates Spark: 50bp brewing for May

Markets are looking up again, and central banks are seeing fewer excuses to delay tightening. The Fed hiked by 25bp yesterday, and 50bp in May now looks possible. The Bank of England is very likely to hike today, but is already more advanced into the cycle and market focus has shifted to growth risks, thus inverting the curve

Market sentiment is looking more upbeat. China’s vow for more market-friendly policies had helped, but progress towards a diplomatic solution to the conflict in Ukraine also appears more tangible. That should also mean fewer excuses for central banks to delay policy tightening.

The Fed just delivered a first 25bp hike, which may well have been a 50bp if it were not for geopolitical uncertainties. Optimism gives rates markets more room to overshoot on the pricing of tightening cycles as the scenarios of severe growth impact get priced out again. For the European Central Bank, markets continue to price more than one hike before year end, and aggressive pricing for the BoE could also prove sticky even if temporarily dented by a still more cautious tone today.

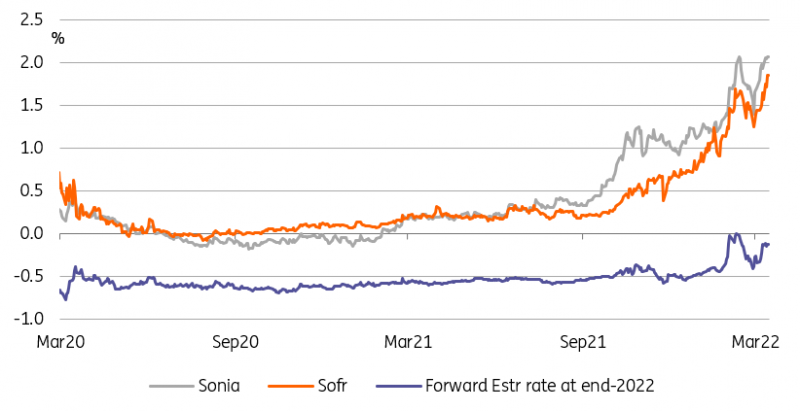

Geopolitical optimism means rate hike pricing can overshoot in Europe

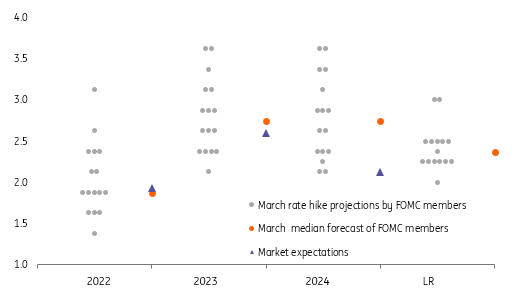

Flatter curve led by a front end reacting to a 3% handle in the Fed’s central forecast range

Impact reaction on the bond market has been a marked flattening of the 2/10yr curve, with the largest impulse coming from the rise in the 2yr yield. It’s just short of 2% now, a nod towards the upward revision to the dot plot, one that now features a 3% handle for the funds rate at the upper end of the central tendency range. The 2yr went into the meeting at quite an aggressive discount versus the funds rate anyway, one reminiscent of rate hike cycles that were typical before the great financial crisis, when 50bp hikes were not unusual. The 2/10yr spread is now below 25bp, which is a remarkably flat curve for the very beginning of the rate hiking cycle.

Live risk for a 50bp hike from the May FOMC meeting

The Fed will be pleased with the fall in inflation expectations following their decision, with for example the 5yr breakeven down by some 10bp, to 3.4%. Real rates have matched that by moving higher, and thereby less negative. The path ahead should see inflation expectations continue to fall and real rates continue to rise. The net outcome should see nominal market rates remain elevated, with a 2% handle the norm right along the curve. The fact that the 30yr rate is now at 2.5% does signal that the debate now is whether a 2% handle can morph to a 3% handle for market rates in the months and quarters ahead. The inflation dynamic suggests yes, and indeed we now pivot towards a live risk for a 50bp hike from the May FOMC meeting.

Fed dot plot points to aggressive hikes from here

The Fed also decided to keep things simple by hiking all key rates by 25bp. So not just the funds rate range, but also the rate on excess reserves to 40bp and the rate on the reverse repo facility to 30bp. That range between 30bp to 40bp is where the effective funds rate should sit post today’s hike. Its currently at 8bp. It should settle in the mid 30’s bp post the rate hike. The SOFR rate by the same token should settle at the floor of the funds rate at around 25bp. The Fed could have chosen to under-hike the rate on excess reserve (20bp instead of 25bp) so that it could sit on the funds floor and help take some of the size away from USD1.6bn going back to the Fed on a daily basis. It looks like this will be left to another day.

The BoE should follow up with a third hike today, albeit also only 25bp

BoE tightening that markets are pricing still looks too ambitious

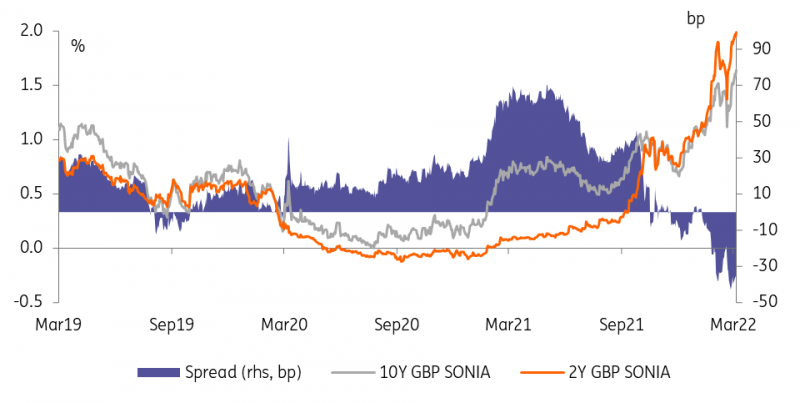

The BoE should deliver its third rate hike today. Our economist expects a 25bp hike in line with the broad consensus, though market pricing suggests a small chance of a larger 50bp hike today for an even more frontloaded tightening. Overall the amount of BoE tightening that markets are pricing in looks too ambitious, especially considering the pushback it had received from some MPC members. Markets see the overnight rate 140bp higher by year end which would take the Bank Rate to above 2%. But being more advanced into the hiking cycle, aggressive rate hike expecations have inverted the yield curve where the market is weighing the growth risks of the supply shock in the medium to longer maturity tenors.

The 2s10s SONIA curve has already inverted for some time

Could that pricing reverse? The BoE may still turn more cautious today as despite recent market optimism the geopolitical uncertainty remains well in place. We will look out today for a shrinking camp voting in favour of a 50bp hike compared to the four members in February, and for the BoE potentially signaling more strongly that inflation should drop below 2% within its forecast horizon. But to an extent the Sterling curve is also dragged higher in the slipstream of global central banks that are turning more hawkish. And that still appears to be the general direction of travel.

Today’s events and market view

Central banks stay in focus. Today's main event of course is the Bank of England very likely delivering its third hike of the current cycle. But following the Fed decision the Fed's Barkin and Bowman are scheduled to speak and it is not uncommon to hear from more FOMC members clarifying their position. And in Europe the ECB Watchers’ conference starts with appearances of President Lagarde, Chief Economist Lane and Executive Board member Schnabel. She will talk on policy strategies amid prolonged higher energy prices, already a challenge in the context of the green transition, but the geopolitical backdrop has added an new level of acuteness.

In data Europe will see the release of the final CPI figures for February, the US sees housing data and the initial jobless claims.

France will auction up to €11.5bn across short- to medium-term bonds and inflation linked securities, Spain will tap 3Y, 6Y and 10Y bonds for up to €6bn in total.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more