Rates Daily: There’s always OMT

- 24 March 2020

- Rates

It's never been used before, but it's there; unlimited front end buying (OMT). Something for the ECB to bat back to the Fed's unlimited QE stroke. And Italy is as good a candidate as any. Meanwhile, a surge in weekly ECB QE purchases underscores the resolve to lean against any spread widening move. We see rates moving lower amid central bank support

ECB OMT support for Italy nearing?

The notion of using the European Stability Mechanism (ESM) as a means to provide financial support in the Covid-19 crisis is gaining traction, although potentially falling short of issuing joint “Coronabonds.” Germany is reportedly prepared to support granting Italy enhanced credit lines via the ESM with minimal conditions attached. Importantly, this would open up the possibility of unlimited ECB purchases of Italian government bonds with up to 3Y maturity under the Outright Monetary Transactions (OMT) programme. Italian government bond spreads had benefited from the ECB's announcement of the additional €750bn Pandemic Emergency Purchase Programme, but continued to linger at around 200bp over Germany in the 10Y sector.

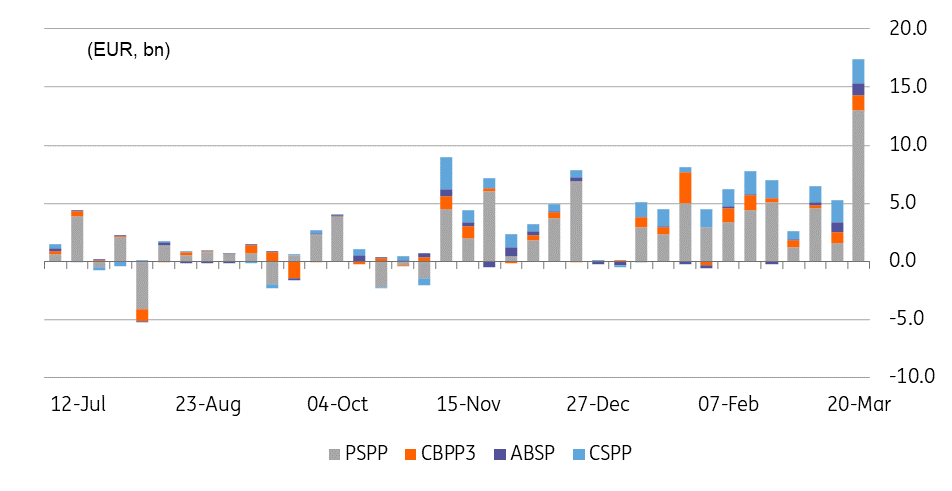

ECB PSPP buying jumped last week

Over the past week ECB net asset purchases amounted to €17.4bn, of which €13bn was in public sector paper (PSPP). These are the highest level of purchases conducted in a single week since 2017. Given the more modest increases in the other private sector buying programmes, we assume this also reflects the reported interventions of last week in the Italian government bond market. While purchases under the additional €120bn envelope should already be reflected in the data for last week, any PEPP purchases under the €750bn envelope announced last week are not be included as they would have settled only this week.

ECB weekly net asset purchases

The coming issuance avalanche

The broad fiscal measures announced to stem the economic fall out of the COVID-19 crisis will have significant implications for eurozone government funding plans. The first details have been trickling in over recent days. With a view to the ECB’s expanded quantitative easing measures it means more available bonds to buy, particularly in a market that was already close to hitting the (“self-imposed”) limits: Germany.

Germany passed a supplementary budget yesterday that foresees an increase of borrowing needs for 2020 to the tune of more than €150bn. The German debt financing agency has released an updated 2Q funding plan, which included the increase of bond re-openings by €8bn in total and an increase in bills issuance by €24.5bn. Additionally, the outstanding amounts of 21 existing bonds will be increased by €2bn each, though these €42bn will be issued into the government’s own holdings. They are to be used to raise short term funding mainly by lending the securities out in repurchase operations. We assume these holdings could be gradually sold off though at some point, which should also make them available for ECB QE purchases. In total, this equates to €74.5bn in additional funding. Looking ahead, the debt agency indicated that the second half will see additional issuance of around €87bn and flagged the possibility of additional increases in the government’s own holdings.

The Netherlands had announced an extra funding need of €45-60bn. We estimate that around €15bn of the additional funding need could be covered via bonds (DSLs) and the rest via the money market (mainly DTCs). The auction calendar for 2Q features six DSL auctions and weekly DTC auctions. Earlier, France was the first to announce amended 2020 funding plans, but the finance minister’s announcement that there will be “no limit” to spending implies it may not be the final adjustment. Long-term bond funding was increased by €5bn, while the net new funding via bills was increased by €17.5bn.

Lower rates amid forceful central bank support

Sure, the delays of the US fiscal response have done their part in keeping a lid on interest rates and the passage of the relief package may still see a temporary rise. But forceful intervention by central banks has also managed to halt the slide higher in rates even as deficts are ballooning. Yesterday, the Fed essentially announced what is unlimited QE and added new tools to "support the flow of credit to households and businesses".

Europe appears closer to getting the ESM involved, potentially unleashing unlimited purchases of Italian governments bonds up to 3Y via OMT if needed. German Bund yields at the start of the week shrugged of a supplementary budget that foresees at least €150bn in additional funding this year. The full extent of Covid-19's human and economic toll will only gradually unfold. We expect interest rates to continue moving lower as optimism fades, being a market that is directly supported by central banks, and that performs well in times of stress.

Fed SPV also prevents tainting the banks

As we continue to digest the Fed's latest moves, we pay particular attention to the new Special Purpose Vehicle to be set up to help corporates - with both a primary and a secondary market facility. Here the SPV would face corporates, providing them with lines of credit and/or issuance monies. The secondary facility would buy bonds on the secondary market. Although short dated (just out to 5 years), these are important complements to the Fed's commerical paper backstop.

This is not QE; in fact we have a suspicion that this could be the Fed's answer to calls for a corporate bond QE programme. But we doubt those calls will go away very soon, noting in particular the angst still being felt in high yield. It should take some pressure off the banks. So far it has not facilitated an easing in Libor though. This partly reflects ongoing stress in the CP market where financials still prefer not to print on pricing grounds.

What’s up today? PMIs, Eurogroup to discuss Italy, Schatz auction

All eyes are on the preliminary purchase managers survey’s for March. The depth of the plunge in the data for Germany, France and the eurozone should provide a first gauge of the economic toll of the Covid-19 crisis.

Eurozone finance ministers are expected to discuss options to support Italy after Germany is reportedly open for granting ESM credit lines with minimal conditions attached.

In supply, Germany issues €4bn via a 2Y bond reopening. Spain is set to sell a new 7Y bond via syndication.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more