Rates Daily: All PEPPed up

- 27 March 2020

- Rates

The US crisis response has been huge. The Eurozone is right up there too; the ECB showed its determination to support bond markets by ditching the issuer limit for the PEPP, another “whatever it takes” moment. A tip of the hat from markets was overdue. We are not there yet and expect rates to test lower again, with US cases having overtaken China's yesterday.

Market rates to continue to test lower

On a number of fronts the market place is in better shape. The primary market has been active again in recent days as the credit stress implied in spreads and CDS eased off the highs, across both the corporate and sovereign landscapes. Safety nets that have been built by the official sector, practically on a global scale, have been given a deserved tip of the hat by financial markets.

But evidence of stress remains. One measure of this comes from the $Libor curve. As practically every other measure of credit stress has eased, Libor in fact edged even higher, widening the spread to the risk free rate to 115bp. Part of the issue here is continued implied pressure on banks as the various rescue mechanisms take time to take-off.

But it is not just that. Behind the scenes there is ongoing default event risk spanning the financial and corporate world that will likely be uncovered in due course. In addition, even in a scenario where economies re-open by the summer, there will be some severe collateral damage left in its wake. Some of this is currently being masked by rescue mechanisms.

These have been a welcome few days, but the risks remain elevated. We still look for lower market rates and yield in the near term. Eventually we will have a big supply-driven curve steepening process, but we are not ready to make that switch just yet. We still think the US 2yr yield can hit zero by the summer.

The ECB shows determination

Eurozone government bond markets rallied across the board yesterday, 10Y German bond yields falling by 10bp to -0.36%. The spread of Italian bonds over Bunds tightened by more than 20bp. We agree with the move lower in EGB yields but, pending more steps towards common fiscal risk-sharing, we think the risk-reward in core bonds is more palatable.

The ECB had greeted markets with new details regarding its Pandemic Emergency Purchase Programme (PEPP) which we believe has been rightly touted as a game changer. The official legal decision, the publication of which kick-started the new facility yesterday, laid out a flexibility going well beyond what was initially announced.

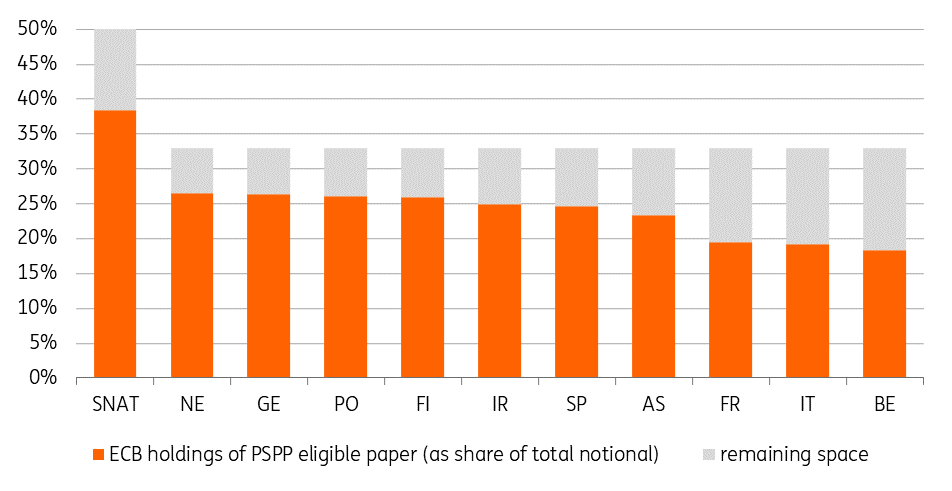

ECB holdings as share of the outstanding PSPP eligible bond markets

Most importantly the ECB has decided not to apply the issue limits to PEPP purchases. This is crucial for countries where the Public Sector Purchase Programme (PSPP) has already approached the 33% share limit of what the central bank allowed itself to hold. According to our estimates these countries are Germany, the Netherlands and Finland, but also Portugal and Ireland where more substantial purchases should now be possible under the €750bn envelope. That does not mean Italy is left out in the cold. While the ECB's capital subscription key remains the guiding principle for the cumulative distribution of purchases among jurisdictions, the PEPP explicitly allows for flexibility “over time, across asset classes and among jurisdictions.”

Additionally the ECB will allow PEPP to buy public sector paper with maturities as short as 70 days. Making shorter dated public sector paper eligible for the PEPP means that the ECB could potentially buy treasury bills from 3 month maturity onwards. This matches the strategy of debt agencies ramping up bills supply to cover their immediate funding needs. And it would be consistent with the nature of the crisis which constitutes a short term emergency. However, as a result the duration impact of PEPP purchases could be substantially smaller if the ECB picks up a larger part of what could be a substantial increase in money market issuance in coming months. In combination with the relaxed issue limits this will have contributed to yesterday's remarkable 6bp steeping of the German 10Y-30Y bond curve.

A final thought: There has been no mention of reinvestments of PEPP holdings. While the €120bn envelope was added to the existing APP and thus falls under its respective communication regarding reinvestments, the PEPP has been set up as a separate programme. There may still be a decision towards the end of the year on the matter, but again the short term nature of the crisis suggests that initially it may have been intended to let the portfolio run-off after 2020 when purchases have concluded. This potentially being the trade-off for allowing the PEPP to go beyond the limits that constrain the PSPP.

Let these be tomorrow’s worries, however. For now we would take the ECB's decisions as testament to its determination in supporting bond markets, opening the door to lower rates and further spread tightening. This is just as well as yesterday's EU Council ended with little agreement on a way forward to tackle the impending economic crisis. The call of 9 member states to issue joint debt instruments (coronabonds) was reportedly rebuffed by the Netherlands and Germany.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Covid-19 crisis: What you need to know

- This bundle contains 14 Articles