Rates: three questions going into the July ECB meeting

Will the curve continue to front-load hikes? Will the wider curve tip into a flattening regime? And will the fragmentation instrument keep sovereign spreads in check? These are the three questions investors need to answer going into the July ECB meeting. They will set the tone in rates markets this summer

EUR front-end: front-loading hikes?

Our economics team has said for a while that the window for the ECB to hike rates is much shorter than that implied by the market. With recession fears coming to a head, and an energy crisis looming, that view is gaining in popularity in the market. Curve pricing has not yet converged to our view, however. The next move lower in rates will be along the following lines:

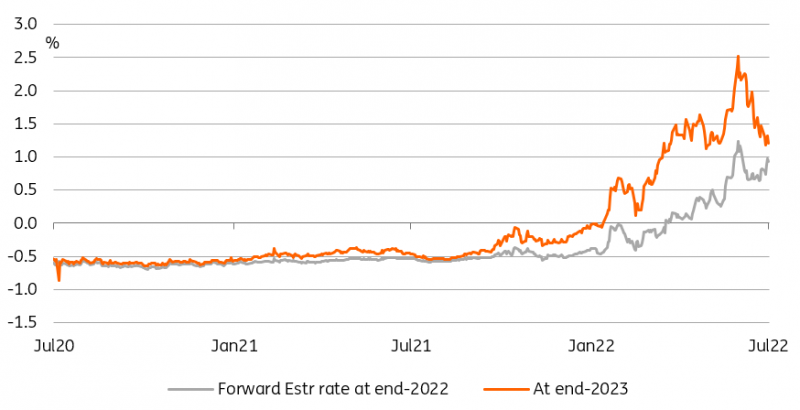

- Halfway through the drop in rates: At its peak in mid-June, the Estr swap curve was pricing over 300bp of ECB hikes by end-2023, this is down to 175bp currently, still some distance from our estimated 100bp. We think there is more to come, but this will be far from a straight line. The catalyst would be a further reduction in gas flows to Europe, or a complete interruption, when Nord Stream 1 is supposed to come back online (ironically on the same day as the ECB meeting).

- 2023 hikes in the balance: With a recession looming in Europe this winter, it is difficult to see the ECB hiking rates in 2023, with currently 25bp priced. This is the part of the forwards curve we take the most issue with. This is even before looking at the discrepancy with the USD curve, the forwards are pricing 60bp of cuts in 2023. Of course, the ECB has proved it can hike in a recession, for instance in 2008, but can it hike while the Fed is cutting? We doubt it.

- Front-loading at the ECB: The last question, in light of the first two on the magnitude of hikes and their timing, is whether there is a trade-off between the length and magnitude of hikes. In other words, would the ECB front-load hikes, Fed-style? A first sign of that would be a 50bp hike at the July meeting, compared to 25bp signalled by President Christine Lagarde and fellow board members.

The curve is pricing more hikes in 2022 but less in 2023

EUR curve, finally time to flatten?

That last question on the front-loading of hikes is closely linked to that of potential curve flattening at longer tenors. The ECB has so far promised gradual tightening. This has prevented, in our view, the kind of curve inversion seen in the US with the Fed hiking 25bp in March, 50bp in May, 75bp in June, and perhaps 100bp in July. Front-loading of ECB hikes is not a vital condition for the curve to flatten but, if it doesn’t happen, market participants need to have a high degree of confidence that the ECB keeps hiking throughout the winter and through 2023, with a recession and energy crisis looming.

Inflation concerns are no longer a deterrent for investors to buy long-dated bonds

Another argument for curve flattening is that inflation swaps are now fully pricing inflation coming back to target. 5Y5Y HICP swaps have touched the symbolical 2% level. Of course, long-dated inflation swaps correlate better with commodity prices and tend to decline heading into recessions. This doesn’t necessarily mean that inflation will settle at these levels, but this shows that inflation concerns are no longer a deterrent for investors to buy long-dated bonds. The question is how low are they willing to chase yields. 10Y Bund yields are close to our 1% mid-2023 target. If the energy situation worsens, nothing says they can’t trade lower, but the front-end would follow too.

The German curve is starting to flatten alongside international peers

Sovereign spreads: playing for time?

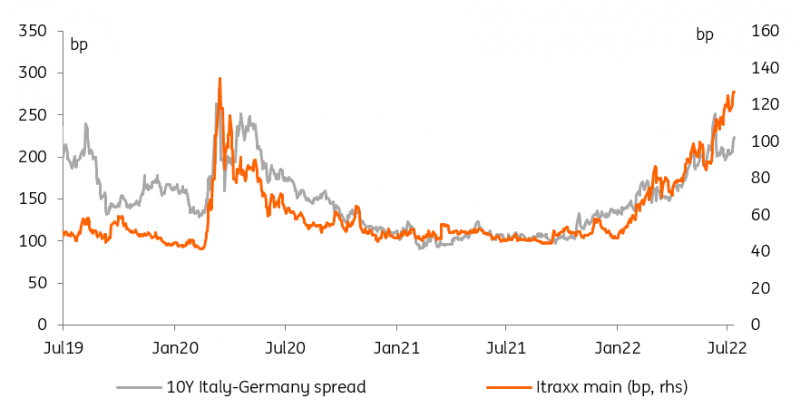

Then there is the question of sovereign spreads, and how they react to more details on the ECB’s fragmentation facility. We’ve argued before that spreads, taking 10Y Italy-Germany as an example, are already too tight when compared to other market-based measures of risk and credit. This may seem like a good result for the ECB but we think tighter spreads could actually be a problem. As the ECB winds down its quantitative easing (QE) programmes, the challenge is to find private investors to replace the ECB as the marginal buyer of Italian debt. These private investors are likely rate-sensitive so too tight a spread over Germany would prevent them from buying sovereign bonds.

Tighter spreads could actually be a problem

Too tight spreads, and the thorny technical, legal, and political issues faced by the fragmentation facility means market suspicion that the ECB would play for time at its July meeting is rife. A political crisis in Italy would add a layer of complexity. If extended, the crisis could propel spreads over Germany to the ‘danger zone’ close to 250bp where the ECB has reacted in the past. On the other hand, it is hard to argue that spreads widening on the back of political risk and fear of fiscal slippage is unwarranted.

Sovereign spreads fail to reflect the widening of broader credit indices

The new fragmentation facility is also supposed to come with some degree of conditionality. It is not our base case but were Italy's Mario Draghi government to fall, it would be harder to argue that this conditionality is met, turning an already fraught political debate into a toxic one. A more likely outcome is that some sort of deal is reached that would keep the current coalition in place. Italian spreads could well re-tighten below 200bp on this news but we doubt their tightening potential much below that level, as the current crisis has fired the starting gun on the campaign for the next elections, in the spring of 2023 at the latest.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article