Prudent Dutch government finances prove challenging under new NATO target

- 24 February

- The Netherlands

Don’t expect large changes to the economic outlook on the back of policy changes in the Netherlands, but some structural growth improvements could be in the making. The budget is getting a large makeover to meet the NATO target with higher taxes and cuts elsewhere. The debt-to-GDP ratio is set to rise further in the long run, albeit from a low level

The new Dutch government was sworn in on Monday, 23 February. When it comes to the economy and public finances, its focus is very much on increasing the defence budget towards the NATO target and improving structural economic growth. But this will come at the cost of higher taxes, cuts elsewhere and a weaker long‑term debt outlook.

Large boost to defence spending is main budgetary challenge

The Dutch government aims to remain fiscally prudent while increasing defence spending to meet the new NATO target. That is laudable as 17 other EU countries, including Dutch neighbours Germany and Belgium, are currently using the national escape clause under the Stability and Growth Pact, which allows additional defence spending of up to 1.5% of GDP per year until 2028.

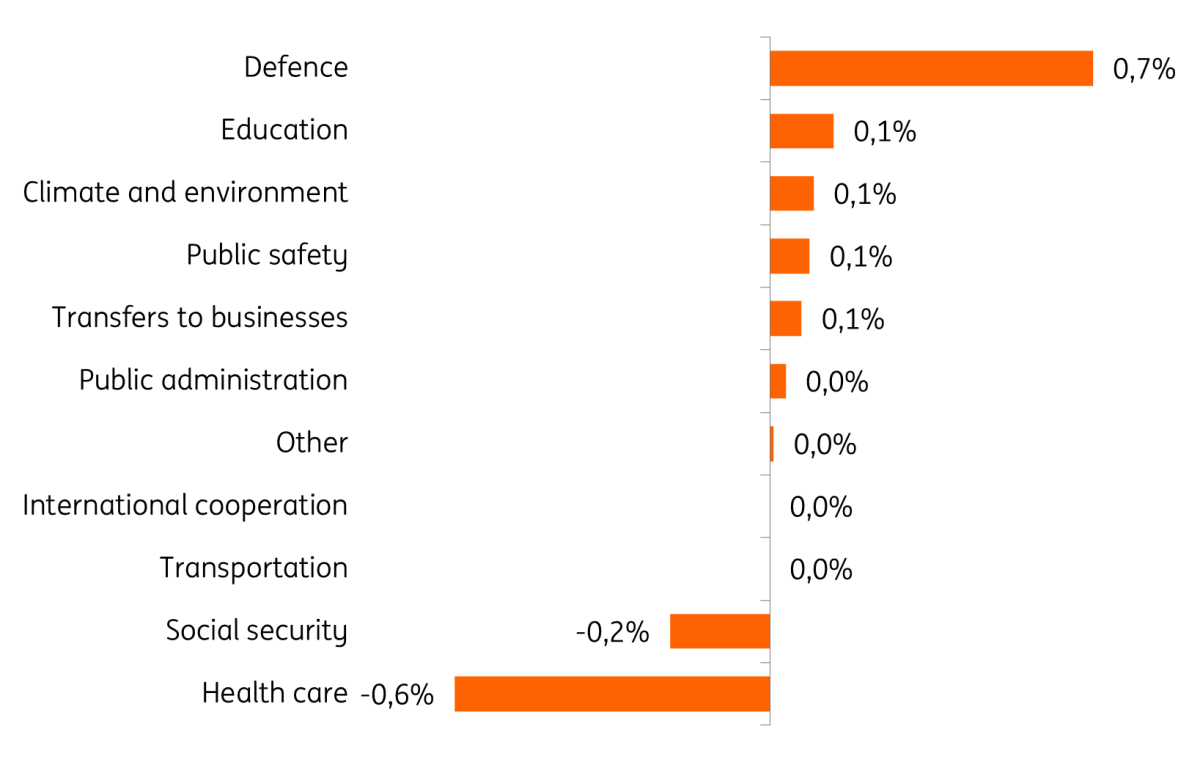

But the budgetary effort announced by the Dutch government is sizeable, with defence spending set to rise by €8.1bn (0.7% of GDP) by 2030, alongside further increases of €1.6bn for education, €1.1bn for climate and the environment, and €1bn for public safety – the largest spending adjustments relative to the no‑policy‑change baseline.

Jetten coalition imposes short-term austerity on social security, health care to fund defence

Change* in government expenditure – expressed as a percentage of GDP in the year before the start of the term – in the final year of the governing period, resulting from the policies set out in the coalition agreement.

To counter this, significant cuts of €7.9bn in health care (mainly through higher copayments) and €2.5bn in social security have been announced. In addition, a ‘freedom' tax on households and businesses results in €5.1bn extra government revenue. Together with some smaller tax increases, this represents the largest rise in the tax burden since the Rutte II government (2012-17), amounting to 0.5% of GDP.

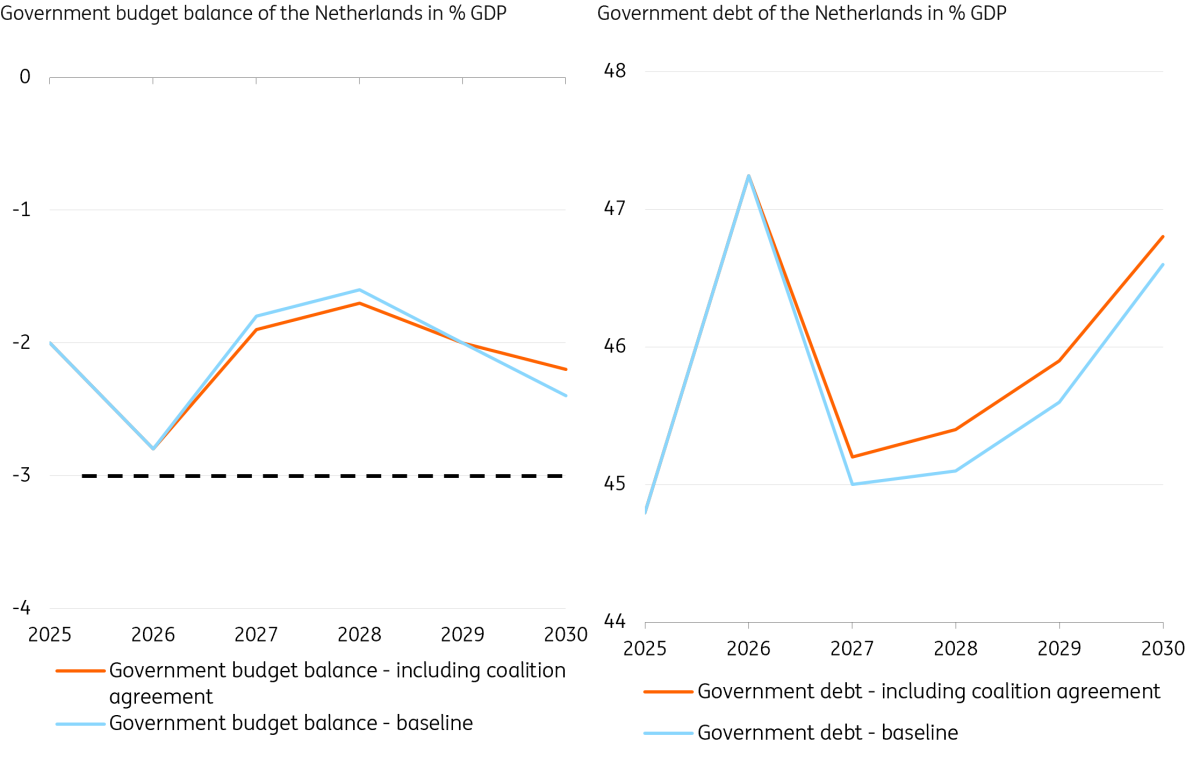

Overall, this means that the expected budget deficit for the coming four years is little changed under the incoming government’s plans. The calculations by the Netherlands Bureau for Economic Policy Analysis (CPB) show that the budget deficit will remain around 2% of GDP for the four-year duration of the cabinet, with a modest increase in the debt-to-GDP ratio to 46.8%. This would leave the Netherlands among the eurozone’s best performers for government finances by 2030.

Coalition pact with higher defence spending leaves Dutch public finances largely unchanged in the short term

Budgetary challenges for future governments remain

But the period after becomes more interesting. Continued increases in defence spending between 2030 and 2035, together with continued (albeit mostly temporary) investments in climate (including windmills), the environment, agricultural reform and housing, and structurally higher spending on education and police, will result in a more rapid than expected increase in the budget deficit. This means that while the new government keeps the budget deficit below 3% of GDP throughout the cabinet’s term, it is still expected to see a structural increase in debt levels. This partly reflects the fact that structural spending cuts take longer to deliver their full savings than the additional spending takes effect. One of the key reforms – the adjustment of the statutory pension age – will not be implemented before 2033.

This additional rise in debt comes on top of an already projected debt accumulation driven by rising long‑term care and social security costs, reflecting an ageing population and the increased generosity introduced by previous governments. The next government will therefore continue to face a significant budgetary challenge. Under current CPB projections, the debt‑to‑GDP ratio is still expected to rise to 137% by 2060, from 118% even in the absence of the current government’s plans.

This highlights the challenge facing European countries in maintaining broadly sustainable debt levels as the ‘peace dividend’ fades and defence spending rises rapidly. While 17 of the EU’s 27 member states have now activated the national escape clause, 2028 will come around quickly. The Dutch case shows that even substantial spending cuts elsewhere and higher taxes may still be insufficient to fully offset rising costs.

Previous governments already initiated much higher (structural) spending

Change* in the final year of the governing term (as a percentage of pre‑term GDP) resulting from the coalition agreement’s policies.

No big impact on short-term growth but some structural improvements

While the underlying changes to the budget are sizeable, the short-run fiscal impulse coming from the new government is negligible compared to the public finances of the outgoing government. CPB doesn’t expect the package to have any noticeable impact on actual GDP growth for the coming years, but there will be an impact on underlying expenditure categories. The higher income taxes and lower social security spending (which affect lower income groups more) will likely curb consumer spending growth modestly. Business investment and government spending are set to grow somewhat faster.

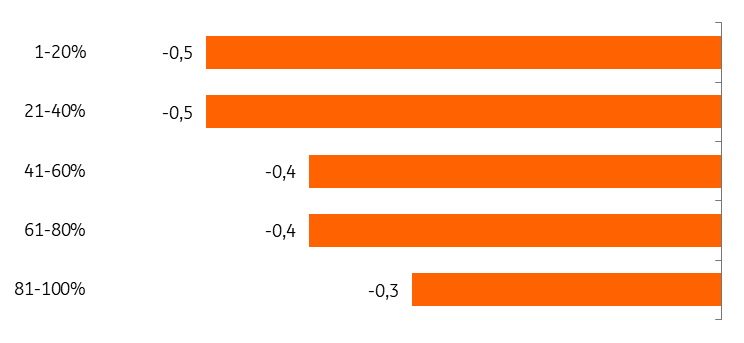

Coalition agreement affects purchasing power negatively, especially for lower incomes

Impact of coalition policies on purchasing power, 2027–30 (percentage points per year relative to median, by income group).

But structural growth is positively influenced by policy changes as CPB expects an increase in labour supply through the increase in the pension age and changes to social security. Although this is difficult to model and thus not explicitly included in CPB calculations, there is also a possibility that more effective measures to address congestion in the energy grid and the still looming nitrogen problem can create scope for investment. And the modest additional public infrastructure is helpful, too.

Finally, the reversal of austerity measures in education also benefits human capital and thus potential growth.

Higher tax burden does not impact Dutch inflation much

The coalition does not significantly influence consumer prices, despite its intention to fund part of the increased defence expenditure through higher taxes. Measures that do directly increase consumer prices include a higher VAT on ornamental horticulture from 9% to 21% in 2028 and a sugar tax for producers in 2030. On the other hand, there are a few subsidy measures that lower energy prices for producers, which may have an indirect effect on consumer prices.

In the shorter term, adjustments to gasoline excise duties have the largest impact on the HICP. During the energy crisis, fuel excise duties were temporarily reduced and not indexed to inflation. The coalition is now postponing the return to the normal, inflation-indexed level by yet another year – pushing the increase for gasoline from 2027 to 2028, following similar measures taken by previous governments (then applying to all motor fuel excise duties). This brings down inflation expectations for 2027, but raises the forecast for 2028, resulting in a smoother inflation profile. We expect Dutch inflation to remain around 2% in 2026 and 2027.

What we're watching as the government begins its term

With a minority government, the question is how many of the current plans are set in stone. The government parties only hold 66 seats out of 150 in parliament, which means that negotiations with the opposition could still lead to different outcomes for the policies currently proposed.

We are interested in seeing how those negotiations unfold – whether, for example, the current budgetary impact holds. There has already been criticism of how the tax burden is split between income and wealth, an area where changes remain possible. Likewise, opposition to the higher statutory pension age could yet lead to adjustments. With a minority government, much can still change after day one.

We're also curious to see how quickly the government can make progress on bottlenecks currently holding back investment (think of nitrogen and net congestion) and deregulation efforts. Both would likely stimulate investment, but these are tough issues to tackle, and previous governments have had a hard time making progress on them. If government policies do deliver the desired effects quickly, this could boost growth, not only in the short term but also more structurally – something that would be very welcome given the budgetary challenges still ahead.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more