Portugal: Good end to the year, but slowdown set to continue

- 14 February 2019

- Portugal

Fourth quarter growth was better than expected, but nonetheless, the economy slowed down in 2018. For 2019, we forecast 1.6% growth and 1.4% in 2020

Good fourth quarter, but on the year the economy slowed

The Portuguese economy grew by 0.4% in the fourth quarter of 2018, which is 0.1 percentage point more than the third quarter. Detailed data isn't available, but the Portuguese statistical agency said this was due to both improved external and domestic demand. However, the contribution of external demand remained negative.

With the Eurozone stuck at 0.2% quarter on quarter growth, Portugal joined Spain with above Eurozone average growth and an acceleration in the in the fourth quarter.

These figures imply an annual growth rate of 2.1% and so Portuguese growth decelerated by 0.7 percentage points compared to 2017, but still remained above the Eurozone average. This was driven by two key factors. First, there was a sharper deceleration of exports than imports. as the slowing global economy had a clear impact on exports in the third quarter of 2018, and this seemed to continue in the fourth quarter. Second, investment growth was bound to slow after a healthy growth rate of 8.7% in 2017.

Outlook less bright

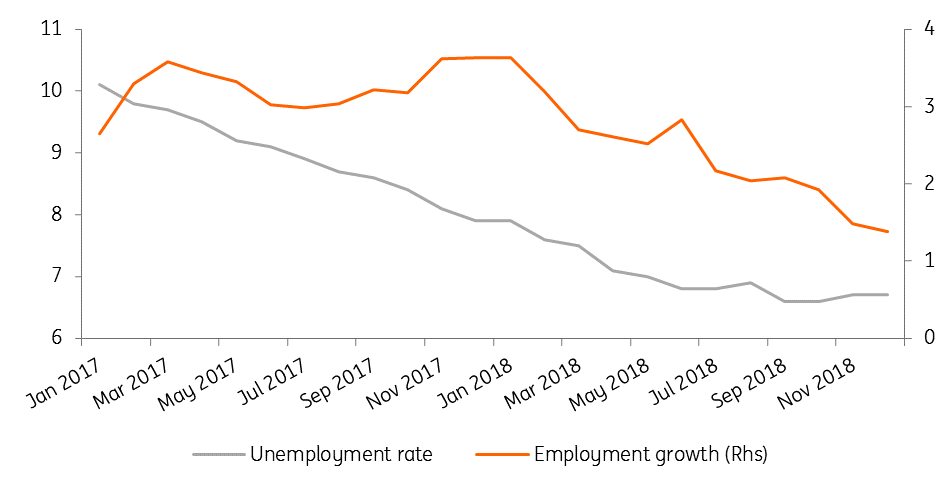

Looking ahead, we foresee a further slowdown in 2019. First, there is the actual weaker external environment, but also the uncertainties related to Brexit and the ongoing trade war which hampers confidence. Second, employment growth continues to decelerate. In early 2018, employment grew at about 3.6% year-on-year, but in December this was only 1.4%. The strong decline in the unemployment rate, therefore, came to a standstill. This should start to impact consumption growth negatively in 2019.

All in all, we forecast a 1.6% growth in 2019 and 1.4% in 2020.

Labour market cools down

Government debt should continue to decline

In terms of budgetary consolidation, the deficit (excluding one-offs) improved again to -0.3% of GDP in 2018 from -0.9% in 2017. The new fiscal policy measures in the 2019 draft budgetary plan (DBP) are structural in nature with deficit-decreasing measures offsetting deficit-increasing ones. The DBP does not include any major change to taxation.

Based on the DBP, we expect the deficit to remain at -0.3% in 2019 which should further allow a reduction of the debt to GDP ratio, raising the probability of an upgrade to the Portuguese credit rating in 2019.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more