Portugal: An astounding recovery but not yet out of the woods

- 30 October 2018

- Portugal

Portugal's recovery from the depths of the eurozone crisis has been nothing short of astonishing. But a high debt pile and issues within the banking sector leave the country vulnerable to another economic downturn

Astonishing growth

Over the last decade, Portugal has sailed through some stormy waters. The global financial crisis of 2008 and the eurozone crisis of 2011 plunged the country into a severe recession, which led to a bailout in 2011. In return for financial support, Portugal was forced to cut spending and implement reforms. Today, the economy is doing much better and is also structurally stronger. Nevertheless, there are still some areas of vulnerability, such as high public debt and a weak banking sector. Continuing with reforms, therefore, remains important.

The recent economic figures for the Portuguese economy are astonishing. Economic growth started to pick up in mid-2016 and now, for the first time after the crisis, we can finally talk about a solid recovery.

- In 2017, the economy grew by 2.7%- the fastest annual growth rate in 17 years.

- The unemployment rate is now below 8%, around pre-crisis levels and below the eurozone average, after peaking at 17.5% in 2013.

Finances improve

Government finances are also moving in the right direction. The fiscal deficit and government debt continue on a downward trajectory due to economic reforms and the strong economy. This improvement has enabled Portugal to exit the Excessive Deficit Procedure of the European Commission in May 2017. The improvement of the fiscal position also led rating agencies to upgrade their rating on the country.

Support for EU remains high

So the headline macroeconomic figures are all going in the right direction. But what about the more structural indicators? Well, here too, there are reasons to be optimistic.

Due to the crisis and subsequent bailout programme, Portugal had to implement structural reforms and cut spending. The economy and government finances are therefore healthier today. And an important point is that there was political support for these. The Prime Minister of the right-wing government during the rescue programme, Pedro Passos Coelho, viewed the crisis as an opportunity to implement reforms that previous governments avoided. This, of course, helped to smooth their implementation. While Coelho lost the election on the back of his austerity policy, support for the EU remains high. Today, 57% of the population has trust in the European Union, the second highest in the EU after Lithuania. In Spain, this stands at just 42% and it's just 27% in Greece.

It's important to note, however, that many structural indicators were already moving in the right direction well before the three-year bailout programme, which started in 2011. It's therefore incorrect to attribute the structural improvement of the economy solely to the reforms that were then introduced. Portugal already understood that structural reform was necessary for strong and sustainable growth.

Educated workforce

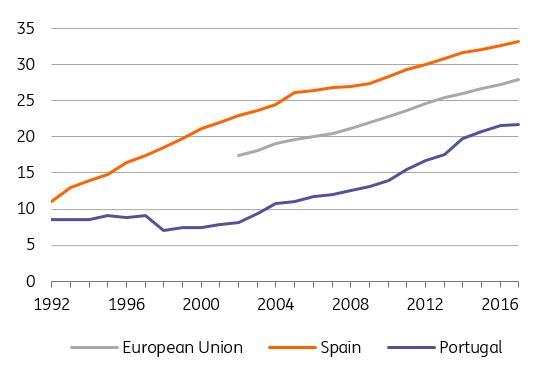

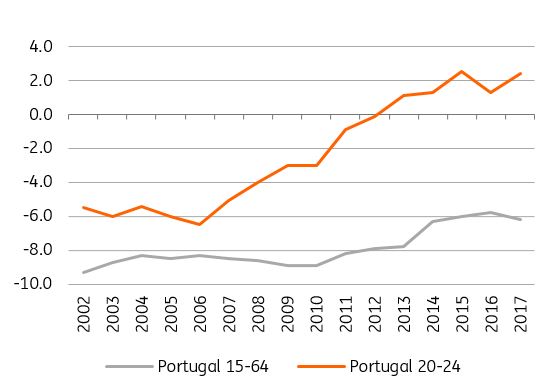

The improvement of human capital, which is a crucial indicator for companies in their decision to invest abroad, is a good example. The share of people with tertiary education has been increasing since the early 2000s, from about 8% to 22% in 2017 (see Figure 1). Moreover, the difference in the population with post-secondary education between Portugal and Europe is falling rapidly (see Figure 2). The tertiary qualification gap was -9.3 percentage points in 2002 and in 2017 this was reduced to -6.2. Admittedly, this is still large but that's related to the legacy of older generations who have lower levels of education. The tertiary qualification gap actually turned positive for the younger population (18-24 years old) in 2013.

And it's not just the quantity of skilled people that's risen. There's evidence that the quality of skills has improved, too. The results of PISA assessments show that Portugal has been on an upward trend. In the latest round of educational assessments in 2015, Portugal scored above the OECD average in all areas (science, reading and mathematics).

Percentage of population (15-64 years old) with tertiary education

Challenges remain

Even though the current improvement in economic figures is a reason for optimism, there are still challenges ahead. It is true that government finances are healthier today, but the high public debt pile still makes the country vulnerable to economic downturns. Government debt as a percentage of GDP equalled 126% in 2017, which is the third highest in the eurozone after Greece and Italy, and this needs to be reduced. The challenge in the next couple of years will be to strike a balance between reducing debt and protecting the economic momentum.

A second area where more work is needed is the strengthening of the banking system. Strong banks are crucial for a well-functioning economy as they help to allocate capital efficiently which in turn helps productivity. But as the value of all non-performing loans still represents 13.3% of total loans, bank intermediation is somewhat impaired.

Wind in its sails

We can conclude that the current economic situation in Portugal has much improved compared to a couple of years ago. The country succeeded in reforming the economy, a process which was already underway in some areas before the bailout programme. However, there are still some issues where more work is needed to reduce its vulnerability. If Portugal manages to do this, the country is clearly setting sail for stronger economic growth.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more