Poland gears up towards faster rate hikes; 50bp in February with upside risk

- 4 February 2022

- Poland

A change in Monetary Policy Committee rhetoric, particularly by the Chairman, suggests faster rate hikes, starting with the 8 February meeting. We see the reference rate reaching 4.5% at year-end vs 4.0% previously

Change in rhetoric by Governor Glapinski

National Bank of Poland Governor Glapinski has made another hawkish pivot since the MPC meeting in January. Back then he said rates should rise to 3% or 4% as long as the economy was growing at a fast rate. Recently he said hikes would exceed market expectations and added that a stronger Polish zloty (PLN) would be consistent with the ongoing monetary tightening.

We find this as an important change of rhetoric and also as a verbal intervention aiming at strengthening PLN. The reasons behind this hawkish pivot are the following: the NBP recognizes upside inflation risk due to CPI developments recently and there has been very strong activity data.

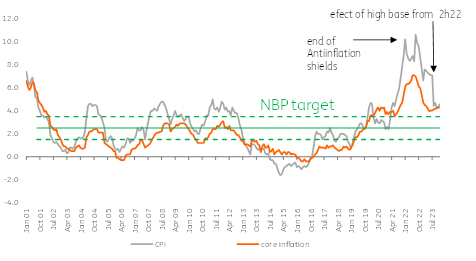

Inflation and the NBP CPI target corridor

Raising our inflation forecasts

Despite the implementation of two anti-inflation shields, our average inflation forecasts for 2022 have increased, due to the following reasons:

(1) Sharp increases in energy and natural gas prices for the retail sector, but also for businesses

(2) Historically high price increases in November and December 2021, suggesting CPI will go above 10% in January 2022

(3) Strong GDP for 4Q 2021: continued consumption boom, high overall GDP growth (closing of demand gap)

(4) Highly likely second-round effects, namely how easily the companies may pass their high costs on to retail prices plus the wage-price spiral. The last NBP Beige Book points at elevated wage hike plans motivated by high inflation.

As a result, we see average inflation in 2022 at 9.1% (in a scenario with anti-inflation shields staying till July) or, 8.1% (in case the shields are extended to the year-end); in 2023 we expect inflation to be 6.1% and 7.1%, respectively.

In our base-line scenario we stick to a 50bp hike in February with upside risk, ie, 75bp hike. In response to the governor's hawkish comments we change our previous forecast and look for more hikes in 2022 and the 4.5% terminal rate should be reached already in 2022 and not 2023 as we forecasted previously.

During the February meeting the NBP governor should repeat his hawkish rhetoric. PLN should be the main beneficiary of this change. It seems the NBP wants to lean in line with the wind, and his hawkish comments nicely align with other factors calling for stronger PLN, ie, ECB hawkish pivot supporting €/US$ and CEE FX as well as government attempts to build a compromise with the EU to unfreeze Recovery Fund for Poland.

Recovery Fund for Poland

As a reminder, Poland appealed to the European Court of Justice regarding the conditional mechanism. In practice this mechanism is used by the EC to freeze the Recovery Fund for Poland as long as the government does not want to close the Disciplinary Chamber of the Supreme Court, which is seen as a violation of judiciary independence. The last days brought some progress on two fronts the PiS government has with the EC. Firstly, Poland reach a compromise with the Czech Republic on the lignite mine the Czech government appealed to the ECJ, and secondly Polish President Duda proposed to close the Disciplinary Chamber in Supreme Court and replace it with another body. We still think it is far from a compromise that would lead to unfreezing the Recovery Fund for Poland, but the government's attempts to make a deal with the EC is showing some kind of progress. This should support PLN and strengthen the pass-through from NBP hawkish comments to PLN. Importantly, should the Polish government fail to reach a compromise with EC till the end of 2022, Poland may lose 70% of €22bn allocated in grants to the country.

More rate hikes ahead

Still, verbal interventions are not enough to cause that kind of PLN strengthening, which would bring a significant CPI slowdown. Given the uncertain NBP communication in recent quarters and its less hawkish approach than other central banks in CEE, the NBP should keep delivering hikes, and not just verbal interventions. That is why we raise our forecast of interest rates in this year to 4.5% vs 4.0% we expected for 2022 previously. It is not that easy to contain inflation with a strong PLN and without credible hikes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more