Philippines: ‘Revenge’ spending to fade as new central bank governor takes over

- 9 January 2023

- Philippines

Philippine growth received a nice boost from 'revenge' spending but we don't think that will continue in 2023

Philippines: At a glance

The Philippine economy benefited from election-related spending in the first half of 2022 on top of pent-up demand after mobility restrictions were finally relaxed. Lockdowns in the country were particularly long (almost two years) which may be contributing to 'revenge' spending, which appeared to be quite robust at the end of 2022. Household consumption remained solid despite surging prices and rising borrowing costs. In particular, spending on items such as air travel, restaurants and hotels and recreation has now registered at least four quarters of double-digit growth giving more credence to the reopening story.

Meanwhile, the potent mix of resurgent demand, currency depreciation and elevated commodity prices have all contributed to a pickup in price pressures. As a result, Bangko Sentral ng Pilipinas (BSP) has been busy, hiking rates by 350bp in 2022. BSP Governor Felipe Medalla has been particularly worried about the peso’s weakness given its impact on inflation but we could see an eventual reversal in policy stance as early as the first quarter of 2023.

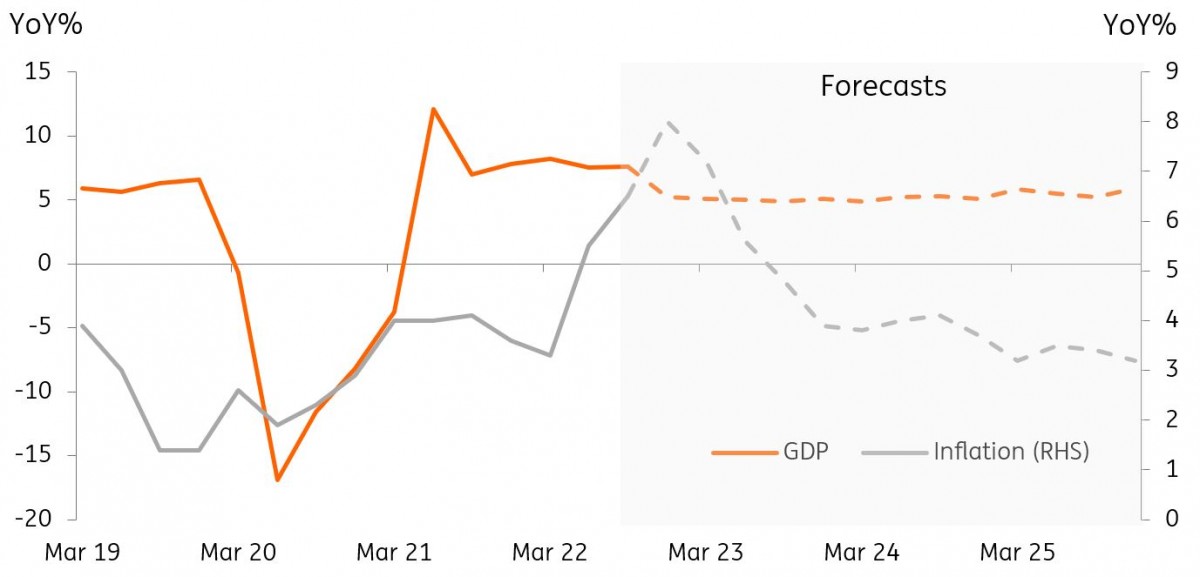

Growth and inflation outlook

3 Calls for 2023

Revenge spending to fade by 2Q 2023 after savings depletion

Pent-up demand explained the better-than-expected growth numbers from the Philippines recently, but we need to ask the following questions: how much longer will this last? And more importantly, how are households funding these purchases amidst multi-year high inflation? In the past, surging prices resulted in a sharp cutback in spending, however, the reopening story appears to be more compelling, at least for now.

Robust spending is likely supported by improving labour market conditions. However, we believe that the recent run of spending may also be funded by a drawdown in savings. The most recent BSP consumer expectations survey showed a decline in the number of households able to set aside savings. This could explain why consumption remains strong despite the twin headwinds of surging prices and rising borrowing costs.

With savings likely depleted to fund an extended run of spending, we expect households to eventually move to rebuild savings by the second quarter of 2023. As households shift a portion of their income back to savings, household spending should fade, resulting in the much-anticipated pullback in consumption, with GDP growth potentially slowing to below 5.0 YoY%.

BSP policy stance up in the air but high inflation to persist

Although the current BSP governor has expressed his preference to match any Federal Reserve policy adjustment from here on, Governor Medalla is set to retire by July 2023. Thus, we can expect the BSP to maintain a 100bp differential with the Fed but only until mid-2023. After that, we believe that the policy direction and the pace of any adjustment by the BSP next year will be largely dependent on who President Marcos appoints to head the central bank. And his choice for this post will be a key point to watch next year.

Regardless of who will sit as the BSP governor, inflation will likely stay stubbornly high in 2023. Inflation is expected to peak by the end of 2022 at around 8.2% YoY and then only grind lower throughout 2023. Price pressures are spread across the CPI basket with nearly 60% of the items experiencing inflation above 4% YoY suggesting price pressures are well entrenched. Thus, we forecast 2023 full-year inflation to settle at 5.4%.

Debt to GDP ratio still an issue. Wealth fund pushed by new administration

The current government debt-to-GDP ratio remains elevated (62.5%) and should remain above 60% for the next four years. The government expects this ratio to slip below 60% by 2026 suggesting that tight fiscal space will be the norm in the medium term. This would mean that government outlays will only have a limited ability to support growth should the economy face headwinds and this could in turn cap growth prospects for the Philippines.

Given the tight fiscal space, the new administration is pushing for the creation of a sovereign wealth fund (SWF) to help attract foreign investors and generate fresh revenues. The proposed SWF hopes to attract foreign investors for big-ticket infrastructure projects. If successful, the SWF would help bring in foreign currency to help stabilise the currency and boost capital formation although we need to wait for more details on how the fund would operate.

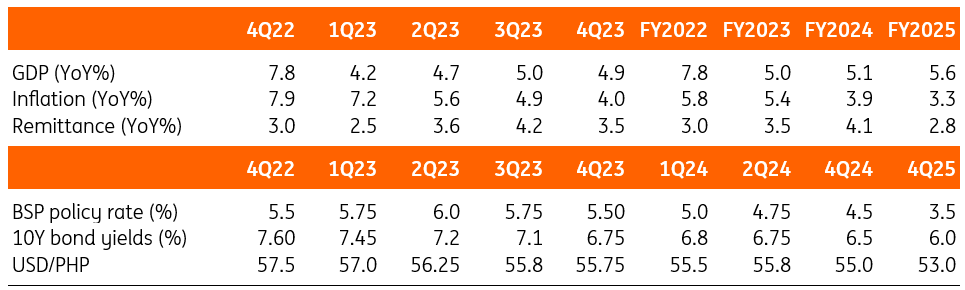

Philippines summary forecast table

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

This article is part of the following bundle

Asia Outlook 2023: Darkest before the dawn

- This bundle contains 11 Articles