The return of twin deficits will complicate recovery in the Philippines

- 13 July 2021

- Philippines

As the rating agency Fitch, revises its outlook to negative for the Philippines, we think the path to economic recovery will be challenging and compounded by the return of the twin deficits. We have lowered our 2021 growth forecast to 4.7% with possible downward revisions if the deficits widen further

| 4.7% |

2021 Philippine GDP growth forecastLowered from 5% |

Recovery status: It’s complicated

It’s been more than six months since our last Philippines economic outlook, and since then, there have been several developments on the Covid-19 front, but not much has changed in terms of outlook.

Back in late 2020, we viewed the Philippines as an economy gradually losing momentum with overall activity weighed down by mobility curbs. We expected a modest pickup in growth in 2021 with momentum hampered by high unemployment, poor consumer confidence and a rapid decline in bank lending, all of which pointed to anaemic consumption and constrained capital formation. So what’s changed, and what has pretty much stayed the same since the end of 2020?

What’s new?

The Philippines began its vaccination program in March 2021, deploying a mix of vaccines, but the program's speed has varied with up to 322,000 jabs administered per day in June, while deployment slowed considerably in July as the country ran out of supply. As of mid-July, the government has fully vaccinated roughly three million citizens (out of 110 million Filipinos), while 9.3 million Filipinos have had at least one dose of the vaccine. Officials target vaccinating 58 million Filipinos in the capital region by the end of November 2021 as new and more infectious variants surface across the globe. Meanwhile, intra-regional movement within the Philippines has resumed as authorities lower restrictions to support the beleaguered tourism industry. But the combination of relaxed international and intraregional movement means that the Philippines remains susceptible to surging infections if new variants enter the country.

What hasn't changed?

Despite the varied developments on the economic and Covid-19 front, we believe the economic trends we highlighted in November last year are still intact.

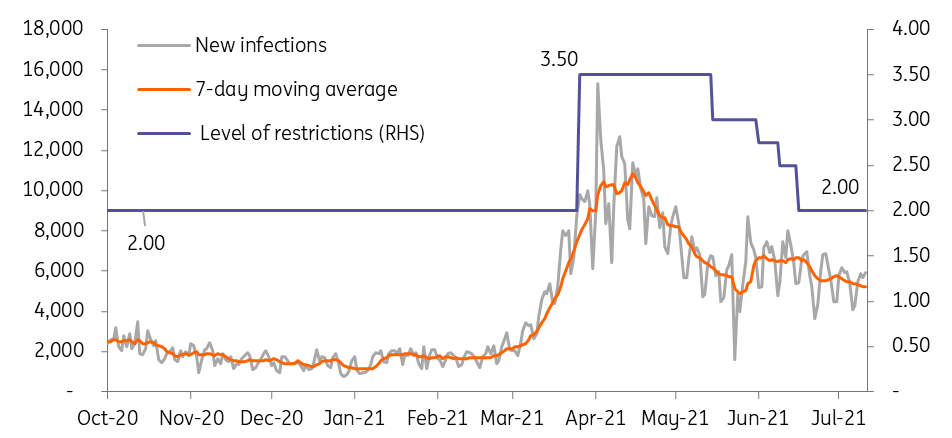

Firstly, partial mobility restrictions have remained with lockdown measures, even intensifying in April 2021 to fend off an alpha-variant induced spike in cases. Partial lockdowns have been fairly stringent for most of 2021 (vs end-2020) and are back at the same level since our last economic review. Meanwhile, economic indicators have either enjoyed modest improvements like consumer confidence while others have been volatile like unemployment data, and some have even deteriorated like bank lending.

Philippine Covid-19 cases and the simplified scale of mobility restrictions

Downward revision to growth outlook

Disappointing first-quarter GDP growth of -4.2%, protracted mobility curbs and a relatively slow vaccination rollout factor into our downward revision to 2021 GDP to 4.7%.

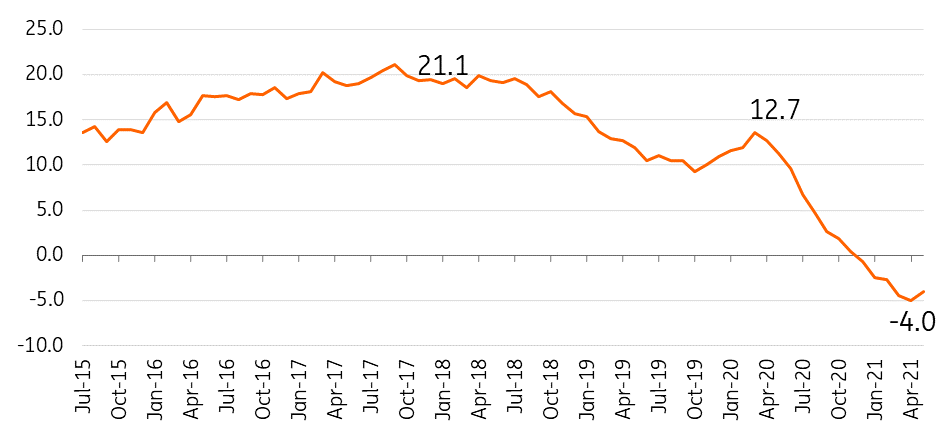

Bank lending has since slipped into negative territory, indicating depressed demand for investment outlays. Consumer confidence improved but remains negative, suggesting a modest recovery in consumption in the near term while unemployment bounces between 7% to 8% depending on the level of mobility restrictions in place.

The little improvement in economic indicators coupled with the threat of the Delta variant-induced spike point to growth losing even more momentum in 2021. The economic recovery remains challenging and could be further complicated by the return of twin deficits as we move into the second half of the year.

Philippine bank lending shows no appetite for investments just yet

Reopening could bring back an old nemesis: The current account deficit

In a curious case of “be careful what you wish for”, the spirited push by authorities to reopen the economy may usher in an old nemesis - the current account deficit.

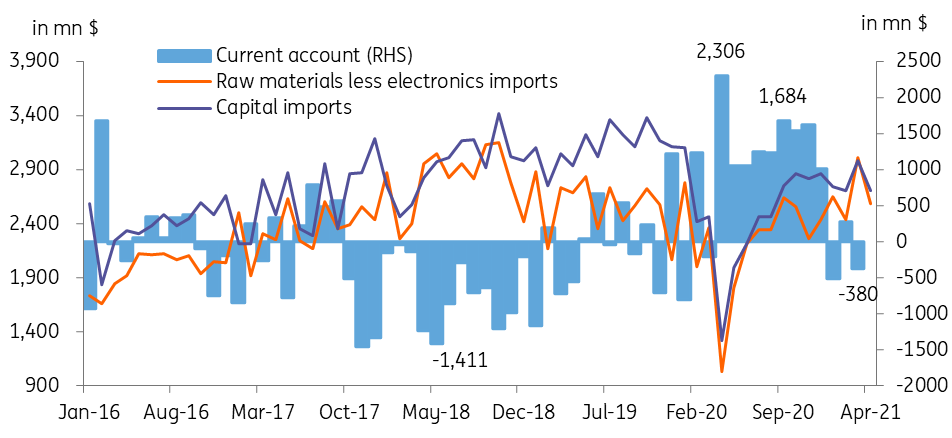

The Philippine economy contracted by 9.6% in 2020, and as a direct result of the slowdown, imports fell by 19.5%, narrowing the trade deficit by 39.5%. Corporate dollar demand evaporated for most of 2020 due to import implosion resulting in a current account surplus and an appreciating bias for the currency.

Noticeably absent from the 2020 import bill were capital goods and raw materials, which together comprise 73% of total imports. The stark drop in capital and raw materials mirrored the steep decline of capital information in 2020, which likewise weighed heavily on overall GDP last year. Not too long ago, the government’s infrastructure push in 2017-19 saw a substantial surge for capital and raw materials imports, which bloated the country’s trade deficit and sent the current account balance deep into deficit territory.

The widening of the current account deficit in 2019 left the Philippine external position vulnerable, resulting in a general depreciation trend for the peso. But sustained currency weakness ultimately forced the central bank to hike policy rates by 175 basis points as inflation surged past target. The central bank rate hikes quickly extinguished investment momentum from the economy and slowed growth to a four-year low of 6%.

The reopening of the economy and the pickup in import demand may have already begun to exert pressure on the peso, with the currency reeling by 1.98% in July. A combination of corporate demand and financial outflows triggered by the recent ruling by the global money-laundering watchdog Financial Action Task Force’s (FATF) has sparked the recent PHP swoon, and a sustained pickup in import demand in the coming months will translate to a wider current account deficit and further pressure on PHP.

A protracted weakening bias for the currency could force the central bank to reverse its ultra-accommodative stance and hike rates from the historical 2.0% level. A mild tightening of policy stance may arrest the peso’s woes momentarily but could also work to undermine the fragile growth prospects with bank lending contracting for six months and counting.

Will the reopening bring the current account deficit back?

Will swelling debt raise alarm bells?

The pandemic forced fiscal authorities worldwide to counter stalling economies via huge fiscal stimulus packages at a time of soft revenue collection, resulting in wide fiscal deficits. The Philippines was running fiscal deficits even before 2020, with the pandemic simply pushing the deficit deeper into the red to 7.5% of GDP in 2020. For 2021, the government expects the deficit to GDP ratio to deteriorate further to 9.4% as revenue collections remain meagre when the government has also slashed corporate taxes.

Wider monthly budget deficits pushed the overall debt to GDP ratio to 62% as of May 2021, with authorities banking on a pickup in economic activity to help bring down this metric under 60% by year-end. With the fiscal position challenged, it’s no surprise that authorities have been actively curtailing expenditures to limit the impact on the 2021 budget deficit to lower the debt to GDP ratio ultimately.

One example of this spartan strategy was the modest 9.5% increase in the 2021 national budget with finance officials preaching the importance of prudence to ensure long-term fiscal viability. Secondly, the budget allocated for the two 2020 stimulus packages was not fully utilised, with unspent funds returning to government coffers to augment the current budget deficit of 9% of GDP recorded last March. Lastly, officials have not supported numerous legislative bills filed by congress for a third stimulus package, citing a lack of funding sources. Overall, government spending is up by a modest 8.8% for the year (as of May), with authorities indicating spending will likely decelerate in the second half of the year.

As of May, total debt to GDP stands at 62.1% of GDP, with domestic and foreign debt totalling Php11.07 trillion. Given the official GDP projection of 6-7%, the 2021 deficit will need to stay below Php445 bn come December - a tall order considering that budget deficit breached this level by May (Php566 bn).

Authorities have been quick to downplay the current elevated levels of both the country’s deficit and total debt. At the same time, finance secretary Dominguez remains confident that fiscal metrics will improve in the near term as soon as revenue streams normalise and the economy begins to recover.

However, since we forecast growth and revenue collections to stay modest in the near term, we expect both the deficit and overall debt levels to remain at dangerously elevated levels. Lacklustre growth and a widening deficit could result in the overall debt to GDP ratio staying above 60% by end-2021 - a development that has undoubtedly caught the attention of at least one major rating agency, with Fitch downgrading the Philippines outlook to negative. A possible credit outlook revision or an outright downgrade will be detrimental to the country’s recovery fortunes with borrowing costs for the already cash-strapped economy move higher.

Will Philippines debt pile be enough to catch the attention of debt watchers?

A complicated recovery, compounded by return of the twin deficits

The Philippines has made some strides in the last six months since our last report with the vaccine program getting off the ground and with some cross border and regional travel restrictions relaxed. However, many concerning economic trends, such as relatively high unemployment, negative bank lending and weak consumer confidence, remain, suggesting that overall economic growth will stay modest in 2021, largely driven by base effects.

We have lowered our 2021 growth forecast to 4.7% from 5% with possible downward revisions should the twin deficits widen further

Meanwhile, we note further complications to the growth narrative with the return of the so-called “twin deficits”. Authorities have moved to reopen the economy to jumpstart growth quickly, but that has also ushered in the return of the current account deficit and the depreciation of the peso that tends to accompany it. The weak currency, in turn, may magnify price pressures making it extra vulnerable given the resurgence of the dollar. At the same time, the confluence of strained revenue streams and lacklustre growth has resulted in successive months of wider fiscal deficits, resulting in the overall debt-to-GDP ratio crossing the 60% level.

Given these developments, we have lowered our 2021 growth forecast to 4.7% from 5%, with possible downward revisions should the twin deficits widen further.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 14 July 2021

- This bundle contains 3 Articles