Momentum slows in the Philippines as headwinds mount

- 27 July 2023

- Philippines

Economic growth in the Philippines has surprised on the upside but signs point to growth slowing over the rest of the year

| 5.6% |

2Q GDP YoY forecast |

Growth at a glance: 1Q growth impressive but momentum is slowing

The Philippine economy continued to surprise on the upside with 1Q GDP growth outpacing market expectations. Growth was powered mainly by surprisingly robust household consumption (4.8 percentage points of 6.4%) with government officials confident of achieving their growth target of 6-7% year-on-year for 2023.

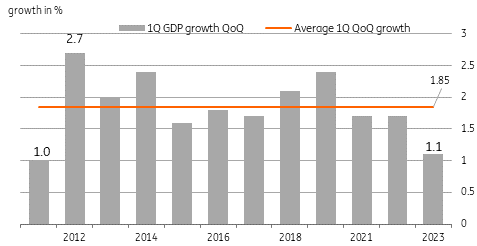

Despite the impressive growth numbers recorded so far, signs point to growth moderating as early as the second quarter. Quarter-over-quarter growth reported in 1Q (1.1%) was the slowest pace of expansion since 2011 and below the 1.9% QoQ average growth outside the Covid-19 recovery period. Perhaps we are seeing the initial signs of a pullback from so-called “revenge spending” as households shift to more normal savings and spending behaviour a year after lockdowns were lifted.

On top of slowing topline economic activity, we are also seeing worrying trends in imports and bank lending which support our expectation that the 6.4% YoY expansion reported in 1Q will likely be the peak for the year. Slowing growth momentum in tandem with mounting headwinds on the global front suggests growth will slow over the coming quarters, with 2023 growth likely settling at 5.6% YoY in our view.

1Q 2023 QoQ growth was the slowest since 2011

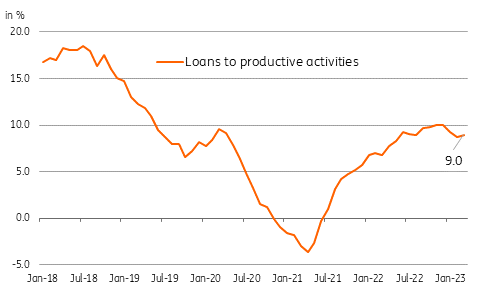

Bank lending slows as rate hikes bite

Elevated commodity prices and resurgent domestic demand drove inflation to a peak of 8.7% YoY in January 2023. With inflation blowing past the central bank’s target band of 2-4%, the Bangko Sentral ng Pilipinas (BSP) resorted to aggressive tightening in a bid to quell inflationary pressures and to support the ailing currency. In total, BSP rattled off a cumulative 425bp worth of tightening beginning mid-2022 with the most recent hike carried out in March.

BSP’s aggressive tightening helped steady the peso but has begun to weigh on bank lending activity. The lagged impact of rate hikes takes roughly 12-to-18 months to take effect according to the BSP. Thus we can expect the lagged effect to continue to weigh on bank lending until early next year should March 2023 be the last move for this particular hiking cycle.

Loans to productive activities decelerated to 9.0% YoY after hitting a recent peak of 10% YoY last November. Bank lending in the Philippines is concentrated in six sectors, namely manufacturing, utilities, retail trade, information & communication, finance & insurance and real estate. These sectors, accounting for two-thirds of total lending, represented 6.3 percentage points of the 7.7% expansion. Although a number of sub-sectors have recorded double-digit growth, the rest have shown a moderation. The modest slowdown does not quite fit the narrative of an economy accelerating and gearing up for faster growth. In the past, periods of rapid GDP growth were accompanied by bank lending sustaining strong double-digit gains, which does not appear to be the case currently.

Thus, as expected, the recent string of rate hikes appears to be doing the job of snuffing out excess demand, with bank lending showing signs of cooling. Although this is a welcome development on the inflation front, there are some negative implications for future growth.

Rate hikes weigh on bank lending

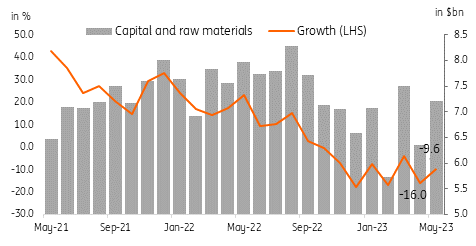

Import trends show flat or moderating capital and raw materials imports

Meanwhile, import trends also suggest that growth momentum may be fading. Year-to-date, imports are down 6.6%, with all sectors in contraction save for consumer imports. Capital goods and raw materials, two key leading indicators of future growth, are down 5.8% and 13.7% year-to-date, respectively.

Combined, capital and raw materials imports have posted negative growth for eight straight months, suggesting that potential output will be constrained as imports such as electrical machinery, aircraft, office machinery, semi-processed raw materials and unprocessed raw materials are all in contraction. Philippine economic growth may still be heavily reliant on household consumption but the trend of falling imports could point to the economy hitting constraints sooner rather than later.

Contracting capital and raw materials to cap future growth

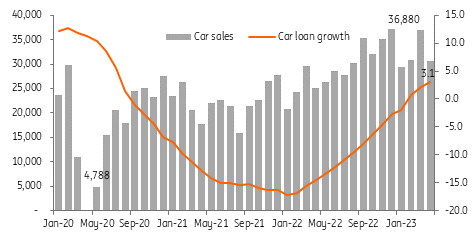

Car sales have been brisk, but how are Filipinos buying them?

Road vehicle sales recovered steadily after cratering during lockdowns with monthly sales of cars and trucks reverting to pre-Covid levels of more than 30,000 units. Road vehicles have been used in the past to measure growth in capital formation given that it represents roughly 16% of total capital formation and 49% of total investment in durable equipment. The strong pickup in vehicle sales helped support growth momentum over the past year but will it be sustainable?

One interesting development that we’ve noted is the relatively slow pickup in motor vehicle loans despite the strong rebound in vehicle sales. Lending for vehicles has only recently moved back into expansion, almost two full years after the recovery in actual vehicle sales. This begs the question: how are vehicles being purchased if not through bank loans?

One explanation is that vehicles are purchased with cash. However, given the sharp downturn in economic activity during lockdowns, it may be difficult to assume that all households had ample savings to purchase vehicles upfront once the economy reopened. One alternative possibility would be that vehicle purchases were financed by non-bank institutions such as the financing arm of car dealers, which are not covered by the reporting standards of the Bangko Sentral ng Pilipinas. Lending companies could be offering financing however it may be difficult to determine the structure and pricing of such loans given the lack of data.

A sharp uptick in rates for such loans could constrain the cash flow of households which purchased vehicles through this type of financing and eventually lead to a slowdown in overall consumption in the coming months.

Notwithstanding questions on the source of financing, road vehicle sales have been a solid contributor to growth in the past few quarters. However, an eventual slowdown in vehicle sales, whether it be due to expensive financing or buyer fatigue, could also weigh on growth momentum in the coming quarter.

Car sales have been stellar but auto loan growth has lagged

Market outlook: Steady PHP and an extended pause from BSP

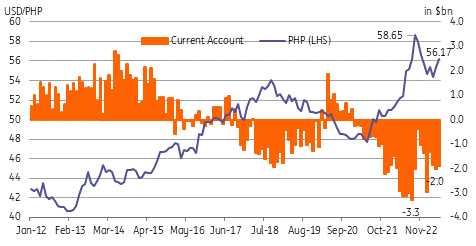

The Philippine peso has rebounded from being one of the region’s worst-performing currencies in 2022 (-9.2%) to the second best-performing currency this year (+1.9%). The improved performance can be tied to a slightly less pronounced current account deficit due to a narrower trade deficit. A drop in imports this year (6.6% year-to-date) has helped this development along with imports of most major items (capital, raw materials, fuels) in the red. Fading imports have led to a much smaller current account deficit ($3.3bn vs $1.9bn) which has eased pressure on the PHP compared to last year.

Should this development continue, we can expect the PHP to remain steady and even enjoy further appreciation towards the end of the year if general dollar strength fades at the end of 2023.

Meanwhile, a stable currency and moderating inflation give the BSP space to extend its recent pause for an extended period of time. Recently appointed BSP Governor Eli Remolona indicated he is open to both rate hikes and rate cuts, depending on how the data evolves. The governor shared that he would be open to eventually cutting rates should inflation settle well within target and if growth is in need of support. Given current inflation (5.6% as of June) and growth at 6.4% YoY, we expect BSP to hold rates steady through to at least the fourth quarter.

PHP is region's second best in 2023

Momentum slowing as headwinds mount

Philippine economic growth has surprised on the upside of late. However, signs have surfaced pointing to a loss of momentum and an eventual moderation in growth for the rest of the year. Despite an easing of headline inflation, we have noted trends in imports and bank lending that point to a likely slowdown in growth with capital formation capped by underinvestment. Aggressive monetary tightening carried out last year will likely continue to stunt bank lending growth as the lagged impact from rate hikes feeds through to capital formation until early 2024.

Against this backdrop of slowing growth momentum, the Philippine economy will face additional headwinds from the slump in global trade and the struggles of major trading partners apart from the United States. Although the export sector contributes only modestly to overall growth, a slowing China could translate into soft demand for Philippine exports and also cap potential tourist arrivals from the mainland to the Philippines.

Thus, despite posting a surprise expansion in 1Q, signs of slowing growth momentum suggest that 6.4% YoY growth in 1Q will likely be the peak for the year. We have pegged 2Q GDP growth to settle at 5.6% YoY while full-year growth should settle at 5.5%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more