China’s not so happy 70th birthday

- 7 October 2019

- China

The 70th anniversary of the People’s Republic of China came against the difficult backdrop of the trade war, protests in Hong Kong, swine fever and a struggling economy

The 70th anniversary of the People’s Republic of China came against the difficult backdrop of the trade war protests in Hong Kong, swine fever and a struggling economy.

Policy tools are being tweaked continuously and the net result is that, so far, the economy as a whole continues to hang together. This is taking a lot of effort though and has brought the currency into play as a prominent, if not a very effective new policy lever.

Swine fever no laughing matter

Given the energy-sapping influence of the trade war and the political irritation of the Hong Kong protests, the very last thing that China needs right now is a food safety shock. But the swine fever is rampaging, not just through China, but across the region leading to the decimation of swine herds and soaring pork prices.

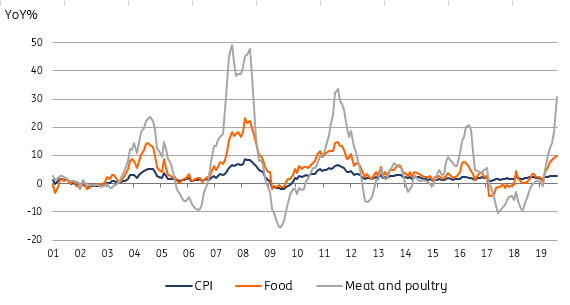

Inflation rising - a tax on households

Overall food price inflation has already soared to more than 12% as a result. And this is effectively a tax on households, weighing on their ability and inclination to spend.

This would be bad enough in normal times. But right now, with authorities in China on a “war-footing” to prevent the trade war from derailing the economy – it is even more concerning.

Chinese inflation

More fiscal and monetary tools being used

Fiscal tools have already been activated, including tax cuts and subsidies, as well as infrastructure spending financed by local government bond issuance. Monetary policy levers have also been added and incremental nudges to policy accommodation are ongoing, as we saw this month with the further downward push to the loan prime rate by 5 basis points, and cuts to required reserve ratios.

The trade war is hurting China

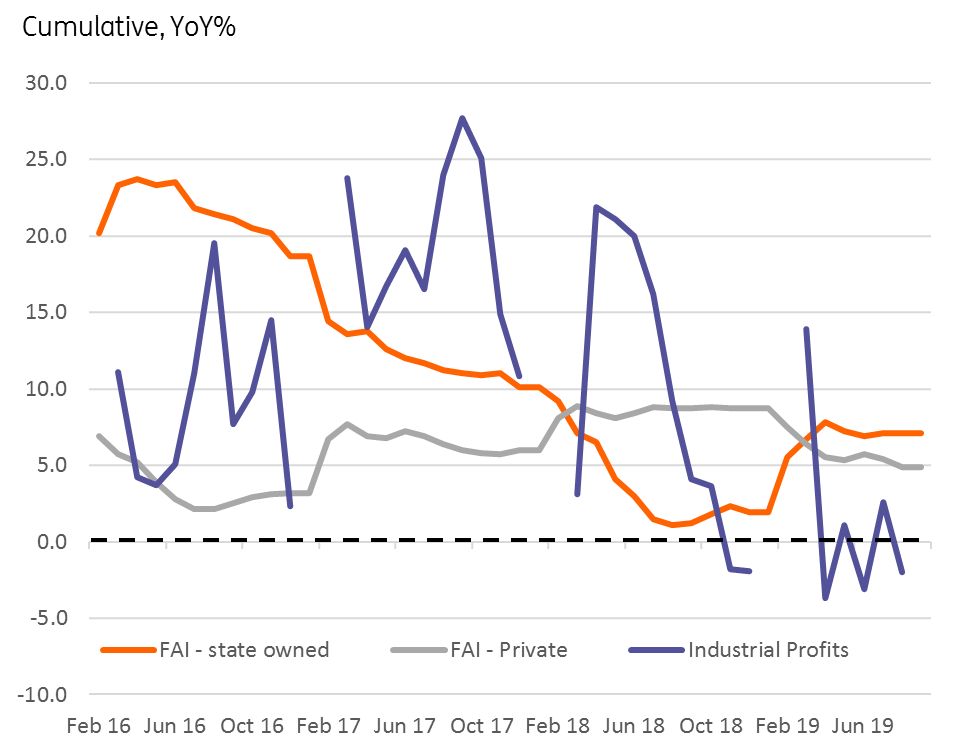

All this may help in time, though lags make it hard to judge the efficacy of measures already undertaken. In the meantime, the run of data has been mixed to poor. Hard data – fixed asset investment, industrial profits and industrial production have come in substantially weaker than expectations recently. Softer survey data, PMIs, and others have been more mixed with some recent upside surprises. The net conclusion, though, remains that the trade war is hurting China’s economy, and it is taking a substantial policy effort to keep things moving forward.

Hard data has been mainly bad

Further stimulus likely

Additional policy efforts look pretty much like a done deal. China’s strategic pork reserves have been utilised to try to keep food prices down. But further direct support measures for households will likely become necessary. Additional purchases of US pork will also likely be necessary, weakening the Chinese position in the trade war, though this can be presented as a favourable shift to foster trade dialogue, as it has been recently.

The yuan is now a policy lever in its own right

One additional policy lever that can be brought to bear is the yuan. For a long time, this was left out of the policy arsenal as being either too political or too prone to negative side effects such as capital outflows. The firming of China’s capital account restrictions has plugged the outflow problem, while ironically, the decision to label China a currency manipulator in early August and escalate tariffs, removed the disincentive for a more activist currency policy.

A weaker CNY doesn’t do much to shield China from tariffs, but it does serve as a clear snub to any US escalation, and we would anticipate this forming a part of any future retaliation. Recent movements of USD/CNY seem to have mirrored market sentiment about a possible trade deal, and recent CNY behaviour has appeared to be more market-driven than at any recent juncture.

Our forecast for USD/CNY for the end of 2020 is predicated on further trade trouble ahead and remains at 7.30.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 4 October 2019

- This bundle contains 5 Articles